In this article, Russ Koesterich discusses why bonds are still not a reliable hedge for equities in an environment where inflation remains elevated and volatile.

Key takeaways

- For nearly two decades long duration Treasuries were an efficient hedge in multi-asset portfolios.

- This dynamic began to change in 2022 with the rapid surge in prices, causing stocks and bonds to more positively related.

- In this environment, investors may consider other hedging strategies such as an overweight to the U.S. dollar and exposure to equity options.

Like a young child stuck on a long car trip, many investors keep asking the same question: Are we back to a world in which bonds act as a reliable hedge? From my perspective, the answer is still no. Instead, investors should consider a variety of strategies, including the use of options, rather than rely too much on bonds as a risk mitigator.

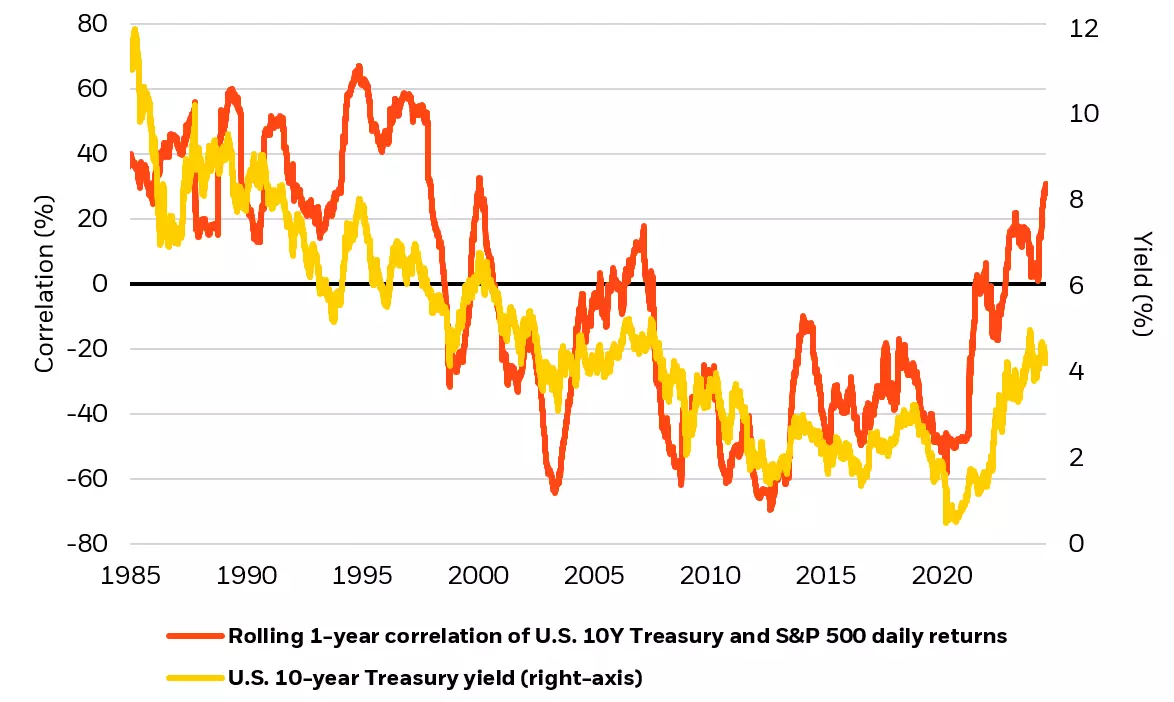

As discussed in previous blogs, for nearly two decades long duration Treasuries were an efficient hedge in multi-asset portfolios. The reason: stock/bond correlations were consistently negative in the 20 years leading up to the pandemic. That began to change in 2022. After decades of low and stable inflation, investors were suddenly faced with the fastest surge in prices since the 1980’s.

As I discussed back in March, while inflation has come down the world still looks very different than was the case in recent decades. The Federal Reserve’s mission to return the economy to a state of low and stable inflation remains incomplete.

To be sure, in recent months there have been signs of progress. The core consumer price index (CPI), which excludes food and energy prices, has decelerated from 6.6% to 3.4%. That said, inflation remains both elevated and more volatile. Given this dynamic, stock/bond correlations are unlikely to revert to their pre-pandemic norm anytime soon (see Chart 1).

Correlation of U.S. bond and equity returns (1-year)

To see why it’s useful to compare today’s inflation levels to those prior to the pandemic. At around 3.5%, core inflation is still nearly twice the 2000-2020 average of around 2%.

Not only is inflation higher, but it is also less stable. The 3-year volatility of inflation, measured by the standard deviation of monthly changes, is down significantly from the 2023 peak but remains double the average of the previous decade. Put differently, while inflation volatility is moderating, it is still far from moderate.

A tool kit, not an asset class

If bonds remain an unreliable hedge, what is the alternative? Unfortunately, there is no single asset class that offers the same liquidity, convexity, and reliability. Previously I discussed the benefits of maintaining an overweight to the dollar, particularly against the euro. I still think a long dollar strategy can help manage risk, particularly if the catalyst for a market sell-off is an aggressive Fed.

Apart from currency positioning, another strategy to help mitigate downside risk: Take advantage of cheap equity market volatility by using options. With index level volatility, evidenced by the VIX Index, still well below the long-term average, investors can hold a portion of their equity exposure in call option form without having to pay above average premiums. Call options provide the opportunity to buy the underlying equity index if the price hits a set level within a certain period of time. This strategy maintains upside potential, should the market keep grinding higher, while limiting the downside. So far 2024 has been mostly about upside gains for equity markets. Investors may want to focus more on ways to mitigate downside exposure as we enter the uncertainty of the fall election season.

Investing involves risks: Options involve risk and are not suitable for all investors. Prior to buying or selling an option, a person must receive a copy of "Characteristics and Risks of Standardized Options." Copies of this document may be obtained from your broker, from any exchange on which options are traded or by contacting The Options Clearing Corporation, (1-888-678-4667).

To obtain more information on the fund(s) including the Morningstar time period ratings and standardized average annual total returns as of the most recent calendar quarter and current month-end, please click on the fund tile.

The Morningstar Rating for funds, or "star rating," is calculated for managed products (including mutual funds, variable annuity and variable life subaccounts, exchange-traded funds, closed-end funds, and separate accounts) with at least a three-year history. Exchange-traded funds and open-ended mutual funds are considered a single population for comparative purposes. It is calculated based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a managed product's monthly excess performance, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of products in each product category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars, and the bottom 10% receive 1 star. The Overall Morningstar Rating for a managed product is derived from a weighted average of the performance figures associated with its three-, five-, and 10-year (if applicable) Morningstar Rating metrics. The weights are: 100% three-year rating for 36-59 months of total returns, 60% five-year rating/40% three-year rating for 60-119 months of total returns, and 50% 10-year rating/30% five-year rating/20% three-year rating for 120 or more months of total returns. While the 10-year overall star rating formula seems to give the most weight to the 10-year period, the most recent three-year period actually has the greatest impact because it is included in all three rating periods.

About the Author

Russ Koesterich, CFA, JD, Managing Director and portfolio manager, is a member of the Global Allocation team as well as the lead portfolio manager on the GA Selects model portfolio strategies.

Mr. Koesterich's service with the firm dates back to 2005, including his years with Barclays Global Investors (BGI), which merged with BlackRock in 2009. He joined the BlackRock Global Allocation team in 2016 as Head of Asset Allocation and was named a portfolio manager of the Fund in 2017. Previously, he was BlackRock's Global Chief Investment Strategist and Chairman of the Investment Committee for the Model Portfolio Solutions business, and formerly served as the Global Head of Investment Strategy for scientific active equities and as senior portfolio manager in the U.S. Market Neutral Group. Prior to joining BGI, Mr. Koesterich was the Chief North American Strategist at State Street Bank and Trust. He began his investment career at Instinet Research Partners where he occupied several positions in research, including Director of Investment Strategy for both U.S. and European research, and Equity Analyst. He is a frequent contributor to financials news media and the author of two books, including his most recent "The Ten Trillion Dollar Gamble."

Mr. Koesterich earned a BA in history from Brandeis University, a JD from Boston College and an MBA from Columbia University. He is a CFA Charterholder.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent market outlooks.

© BlackRock

Read more commentaries by BlackRock