Economists are different from normal people. We think that families use supply and demand curves to decide on whether to have children. We forget the names of our neighbors, but we can identify all of the members of the Federal Reserve Board. We don’t think it’s funny when someone says that we were created to make weather forecasters look more accurate.

Economists also believe that people make decisions using cold calculus instead of gut instinct. But voters often employ a visceral perspective when considering pocketbook issues. And this could have a significant bearing on the U.S. election outcome.

The American economy and American markets have performed very well over the past two years. Yet surveys reflect a degree of disappointment. Measures of consumer sentiment are still at a significant deficit to their pre-pandemic levels. A Gallup poll covering the President’s handling of the economy is at its lowest reading since 2001.

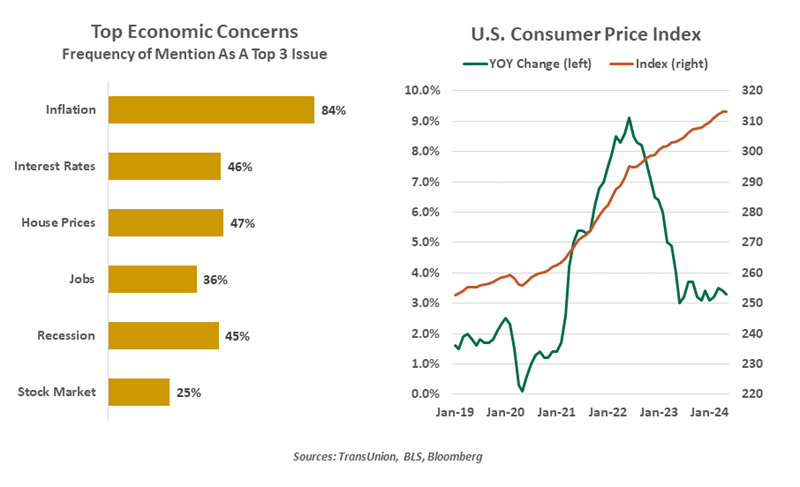

One reason for the disaffection is inflation, which is a leading concern for Americans. This surprises some economists, who point to significant improvement on this front over the past two years. The most recent reading of the Consumer Price Index showed a yearly increase of 3.3%, down from the peak of more than 9% in 2022. Most analysts expect continued moderation in the months ahead.

Further, wages are rising faster than prices. Average hourly earnings are more than 4% higher over the past twelve months, creating gains in real purchasing power for most workers. That should make people happy, but it has not.

A typical person does not follow the inflation data at close range. Instead, impressions of inflation are formed through the experience of shopping for goods and services. And whether it is strictly rational or not, many think that things have gotten inordinately expensive.

Normal people do not confine themselves to the twelve-month window employed by economists to gauge inflation. In many cases, perceptions are still anchored to pre-pandemic conditions. In aggregate, prices paid by American consumers are more than 20% higher than they were four years ago.

It is also puzzling to laypeople why food and energy prices are set aside when agents like the Federal Reserve assess “core” inflation. These two categories account for a significant portion of monthly spending for many households, and a source of considerable anxiety. A gallon of regular gasoline has averaged $3.41 so far this year, as compared to $2.61 in 2019. Grocery shopping involves regular bouts of disbelief. A dozen eggs costs twice what they did in 2020. Chicken has gone from $1.40 per pound back then to over $2 now. And the list goes on.

To some, only a decline in prices would signal to them that inflation was under control. While we have seen deflation in spots, prices typically don’t retreat. The fact that earnings are rising more quickly than inflation over the past year is of little comfort. Households view this as making up for declines in real income that lasted for more than two years.

INFLATION IS STILL VIEWED AS A SERIOUS PROBLEM BY MOST AMERICANS.

Presidents tend to take the blame for economic discontent, even though they often have little influence over outcomes. Post-pandemic inflation was primarily the product of two supply shocks, to the availability of goods imported from the Far East and to the availability of labor. Neither was within the control of the Oval Office.

The Federal Reserve is chartered with keeping inflation under control, but was late to recognize the scale of the problem. The elevated interest rates required to restore order have impaired housing affordability and stretched those carrying credit card debt. The Fed strives to remain apolitical, but its performance since the last election may have a big influence on the next one.

And so while economists cheer the decline in inflation as they see it, households are not feeling cheery. The difference of perspective may make a difference in November.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

© Northern Trust

Read more commentaries by Northern Trust