Key takeaways

- While many of last year’s themes continue to dominant markets, there is one thing that is different: the energy sector.

- Year-to-date, the U.S. energy sector has posted a 10% gain, roughly in-line with the broader market.

- Russ believes there are several factors supporting the sector including elevated commodity prices and elevated inflation, as well as valuations and its role as a hedge.

Equities have recovered from their April slump and are once again posting new highs. While the rally has broadened, several of last year’s themes, including artificial intelligence (AI) and semiconductors, continue to lead. However, there is one change to note: Unlike last year, when it dramatically underperformed, the energy sector is holding its own so far this year. My own view is that the sector can continue to advance.

Several factors support further gains, including a surge in commodity prices, still elevated inflation, cheap valuations, and the sector’s role as a hedge against geopolitical uncertainty.

Sticky inflation, surging commodities

Energy stocks are benefiting from a resilient economy which has, in combination with select supply constraints, supported the broader commodity complex. Year-to-date, the S&P GSCI Commodity Index is up more than 10%. Depending on the universe, crude oil is up roughly 10%, with other parts of the energy complex, notably gasoline, posting solid double-digit returns.

This rally in commodities is occurring against a backdrop of still elevated inflation. While price gains have decelerated, both core and headline inflation remain comfortably above 3%. This is important as the sector’s performance tends to move with both expected and realized inflation.

During the past two years the S&P 500 energy sector has had a positive correlation with changes in short-term inflation expectations (~0.3), derived from the Treasury Inflation Protected Securities (TIPS) market. In contrast, the broader market has had a negligible relationship with changes in inflation expectations. Put differently, energy stocks may benefit from rising inflation expectations more than other parts of the stock market.

Recent patterns conform to longer-term trends. Historically, the relative performance of the energy sector has been positively correlated with the rate of inflation. Going back to 1995, whenever inflation has been below 3% year-over-year, the S&P 500 Energy sector has generally underperformed, trailing the market by an average of approximately 0.40%/month. However, in periods when inflation has been 3% or greater, energy stocks post positive average returns of around 0.90%/month.

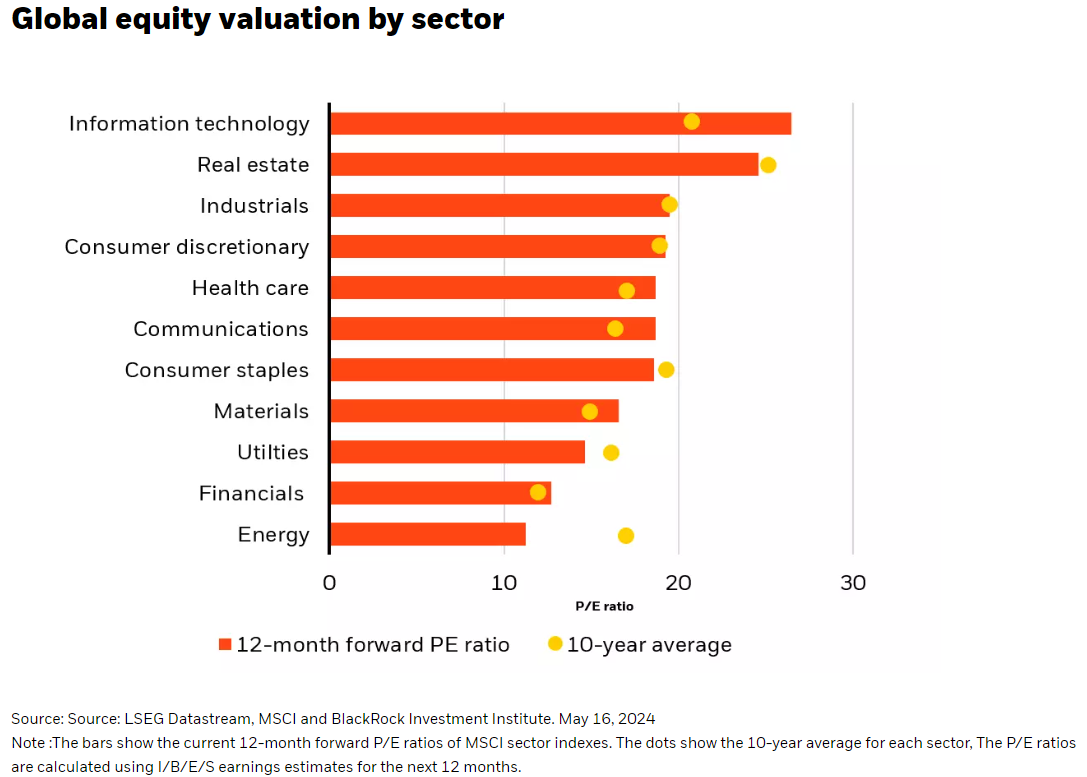

Still on sale

The third factor favoring energy stocks is valuation. Of the 11 GIC sectors energy is by far the cheapest. The current valuation, roughly 11x forward earnings, is also well below the sector’s long-term average (see Chart 1).

Energy stocks, depending on the catalyst, may provide one additional advantage: helping to hedge geopolitical risk. While the market has thus far looked past growing geopolitical instability, the conflicts in Ukraine and the Middle East are not abating. Despite it often proving profitable to ignore temporary eruptions in geopolitical risk, from an economic standpoint the events in Ukraine and the Middle East are distinguished by their potential impact on energy prices, whereas an increase in tensions could result in a spike in pricing. In addition to the other factors favoring energy, it is worth remembering the sector’s role not only as an inflation hedge, but as a geopolitical one as well.

**Investments that concentrate in specific industries, sectors, markets or asset classes may underperform or be more volatile than the general securities market and/or other industries, sectors, markets or asset classes.

To obtain more information on the fund(s) including the Morningstar time period ratings and standardized average annual total returns as of the most recent calendar quarter and current month-end, please click on the fund tile.

The Morningstar Rating for funds, or "star rating," is calculated for managed products (including mutual funds, variable annuity and variable life subaccounts, exchange-traded funds, closed-end funds, and separate accounts) with at least a three-year history. Exchange-traded funds and open-ended mutual funds are considered a single population for comparative purposes. It is calculated based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a managed product's monthly excess performance, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of products in each product category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars, and the bottom 10% receive 1 star. The Overall Morningstar Rating for a managed product is derived from a weighted average of the performance figures associated with its three-, five-, and 10-year (if applicable) Morningstar Rating metrics. The weights are: 100% three-year rating for 36-59 months of total returns, 60% five-year rating/40% three-year rating for 60-119 months of total returns, and 50% 10-year rating/30% five-year rating/20% three-year rating for 120 or more months of total returns. While the 10-year overall star rating formula seems to give the most weight to the 10-year period, the most recent three-year period actually has the greatest impact because it is included in all three rating periods.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© BlackRock

Read more commentaries by BlackRock