The Dollar Remains King

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey Takeaways

- The U.S. dollar has remained dominant as the king of currencies for the past 50 years, despite predictions of its impending downfall.

- The most important precondition for the U.S. dollar to lose its dominance would be the existence of a viable alternative currency, which currently does not exist.

- The threat of sanctions is a significant driver of the angst and rhetoric against the U.S. dollar’s dominance, as many countries lack access to the dollar and face consequences if they do not comply with sanctions.

And there is no apparent successor. For the better part of 50 years, there has been one prediction that has been persistently in the headlines and persistently wrong—the impending implosion of the U.S. dollar. The sheer dominance of the dollar makes it a clear target. Eventually, the U.S. dollar must share its crown as the king of currencies. Right?

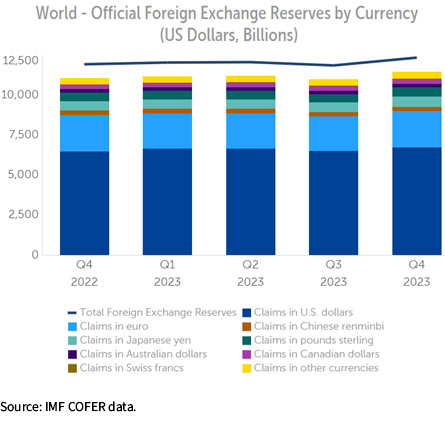

Maybe. But there are a few preconditions that are far from being met. The most important would be a viable alternative to the dollar. The Chinese yuan is frequently cited. It should not be. China has a closed capital account meaning there is a limited ability to transact in the currency. That precludes it from being a viable alternative to the dollar. In fact, China’s Belt and Road lent around $1 trillion in dollars not yuan. That is more signal than noise in the supposed “de-dollarization” narrative. There is a reason the dollar share of reserves has remained stable despite the threat of sanctions (more on that in a bit).

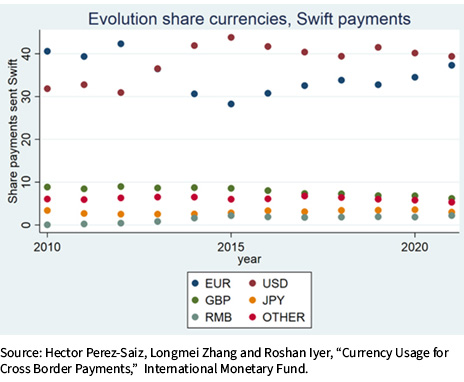

There is an important, often overlooked distinction between “transaction” and “reserve.” The dollar and euro compete for the crown as the transactional currency king. Everyone else competes for a distant third-place trophy.

But the headlines are incessantly calling for the impending downfall of the dollar system. Frequently, these talk about threats from Russia, Iran, North Korea, Venezuela and similar actors. The question that should be asked is, “So what”? Many of the countries saber rattling against dominance are doing so because they lack access to the dollar. Sanctions—and the threat of sanctions—are the primary driver of the angst and rhetoric.

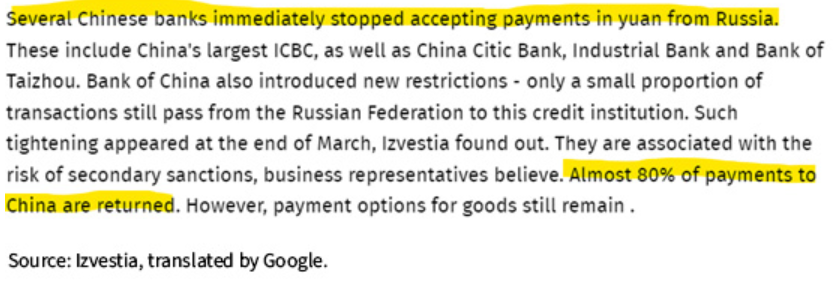

Sanctions are often underestimated. The above quote is a stark reminder of how powerful the threat of sanctions can be in the global financial system. Some of China’s larger banks are unwilling to accept payments in China’s own currency from Russia, because there is the real, tangible threat of being cut off from the broader financial system. Yes, there are ways to evade sanctions. Yes, Russia is pursuing those channels. No, it is not cheap or simple. It takes middlemen and haircuts to avoid sanctions, which raises prices and risks to both parties.

King Dollar is not at risk of losing its crown any time soon. There are always competing economic blocs. That will never change. Sometimes they matter more than others. But—for now—there is simply no other alternative to the dollar. Occasionally, hyperbolic headlines matter. This is not one of those times.

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.

This article originally appeared on WisdomTree's website and is reprinted on VettaFi | Advisor Perspectives with permission from the author. For more information, please visit WisdomTree.com

A message from Advisor Perspectives and VettaFi: Join us on June 27 for the Midyear Market Outlook Symposium, where advisors will gain insights into macroeconomic trends, active ETFs, investing abroad, and more to navigate 2024's challenges.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All