One of the longest nonstop commercial flights in the world is the trip between Los Angeles and Singapore, at just under 18 hours. I found myself on the route three weeks ago; to pass time, I took two long naps, watched three movies, ate two meals, and cleared about 2,000 e-mails.

The journey was tiring, but my energy was restored during two weeks of interesting meetings in Malaysia, Singapore, China, and Hong Kong. Following are my main take-aways from the trip.

China is struggling to find the right formula for economic stimulus.

Official measures of real growth are still aligned with the country’s 5% target, but consumer confidence and spending are soft, export growth has slowed, and business investment has slumped. China is experiencing its largest capital outflows in 15 years, and its equity markets are significantly underperforming.

With an outlook that calls for stimulus, monetary policy in China has become more restrictive. Inflation has fallen, and real interest rates have risen. The money supply is growing more slowly than it has at any time in the last 20 years. With a deleveraging trend in place, lowering interest rates will have limited benefit and could place further pressure on the Chinese currency.

China has announced a program intended to deal with the overhang of apartment inventory. 300 billion yuan (around $40 billion) will be allocated to state-owned enterprises controlled by local governments, which will use the money to purchase unoccupied units and convert them to affordable housing. The program aims to establish a floor on property values and bring supply into better alignment with demand.

But the effort raises a host of questions. It isn’t clear how prices will be set; current owners will almost certainly realize a substantial loss. The amount allocated represents less than 5% of China’s aggregate residential property value, likely not enough to stabilize values. And many local governments are in severe financial distress, and may not be in the best position to execute the plan.

I RETURNED HOME WITH MORE CONCERNS ABOUT CHINA.

There was concern about Chinese deflation among many I spoke with in the region. The policy response to date has been piecemeal. The situation seems to call for broad fiscal stimulus, but high levels of public debt have Chinese officials hesitant.

I returned home with a somewhat higher level of concern over China’s economic outlook. The implication of underperformance for the region and the world could be significant.

Those of us who live in large countries often don’t appreciate how hard it is for developing countries to make economic progress.

One of the more poignant moments of the trip was an address from Malaysia’s economic minister at an event we hosted. He spoke articulately about his country’s challenges and opportunities, highlighting the need to complement traditional industries with newer ones. He also noted the importance of attracting foreign capital, using the phrase “China plus one” as an invitation for firms to use his country as complement to operations in China.

But internal and global politics can present obstacles. Electorates have limited patience, and managing alignments between East and West is terribly difficult for emerging markets. The minister struck the right balance between realism and idealism, a posture that I would recommend as we consider prospects for emerging markets.

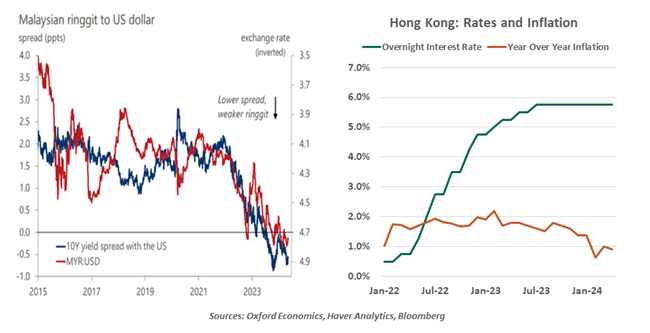

Asian central banks are in a difficult position.

Higher-for-longer interest rates in the United States are causing a great deal of discomfort in the region. Hong Kong provides a case in point: real gross domestic product (GDP) in Hong Kong is still below its 2019 level, and asset values are under pressure. Inflation is less than 1% over the past year, and falling.

But because the Hong Kong dollar is pegged to the U.S. dollar, the Hong Kong Monetary Authority cannot ease until the Fed does. Few countries have this kind of official peg for their currencies, but many have to maintain an informal link to keep capital from leaving the country.

I was asked frequently if the Federal Reserve recognizes the impact its policy has overseas. The Fed is certainly conscious of its global influence, but its Congressional mandate focuses on domestic inflation and employment. Unless stress overseas threatens growth or financial stability in the U.S., the Fed is unlikely to relent.

U.S. POLICY HAS A HUGE INFLUENCE ON ASIA’S ECONOMIES.

The U.S. election is being closely watched in Asia.

Many I spoke with expressed frustration that neither of America’s political parties seems interested in normalizing economic relations with the region. I was also asked often how U.S. markets and the U.S. dollar can perform so well amid so much political dysfunction. (To be honest, I did not have a great answer to that question.) Our deep budget deficits and the mosh pit that Washington has become diminish the desire of Asian countries to follow the American model.

The food culture in Asia is always amazing.

This year’s fare included white pepper crab, Sichuan-style crawfish, and Beijing-style hot pot with lamb. Morning coffee is often strong, over ice, and flavored with just a hint of sweetened condensed milk. That gets the day started right.

Memorably, a group of us escaped the office for lunch one day and went to the Tiong Bahru hawker center in Singapore. We gorged on slow roasted pork belly, freshly made wontons with chili, noodles with roasted duck and kueh with pandan (sweet rice flour cakes). Unfortunately, I was dressed in a suit, which wasn’t suitable for the humidity or the occasional chopstick malfunction.

45 hours in the air over two weeks is no one’s idea of a good time. But the reward for all of that flying came in the form of memorable meals and conversations. I hope it won’t be long before I return.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.