Shedding Light on Private Credit

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIn the old days, there weren’t very many places you could get a loan. If a bank wasn’t willing to extend credit, you’d be thrust into the murky world of payday lenders and pawn shops. If you were really desperate, you get funds from a “shark,” who charged you 5%...per week.

Today, nonbank lending is much more respectable. Known as private credit, this sector of finance is growing very quickly. To its adherents, private credit is a channel that gets capital to borrowers more efficiently and one that offers attractive returns to investors. To its detractors, it is a potential source of systemic risk that needs to be better monitored and controlled.

Following is some background on how private credit came to its current standing, and where it might progress from here.

Bank lending has been losing its dominance for several decades. In the United States, very high interest rates in the 1970s led depositors to shift into investment products, limiting the ability of banks to make loans. Scores of bank failures in the 1980s prompted heightened regulation for traditional intermediaries, raising costs for borrowers. These developments created fertile ground for the growth of new credit channels.

Corporations began to raise capital more frequently in the financial markets. Short-term needs were met through the issuance of commercial paper, which was purchased by money market funds. Long-term needs were covered by bond issuance; according to the Securities Industry and Financial Markets Association (SIFMA), the American corporate bond market has expanded from a little over $1 trillion in 1990 to almost $11 trillion in the third quarter of 2023.

Household finance has also been transformed over the past 40 years. Mortgages once held by banks are bundled, guaranteed and sold as mortgage-backed securities. Consumer loans have also been “securitized.” Banks earn fees for originating these types of loans, but they have become waystations, not warehouses.

Amid this transformation, asset managers have become more and more central to the flow of capital. They create vehicles that sell shares to investors and invest the proceeds in a wide range of asset classes. The sector is not entirely unregulated, but it certainly does not face the same kind of capital and liquidity constraints that banks do. Asset returns are passed directly to investors; liabilities are uninsured.

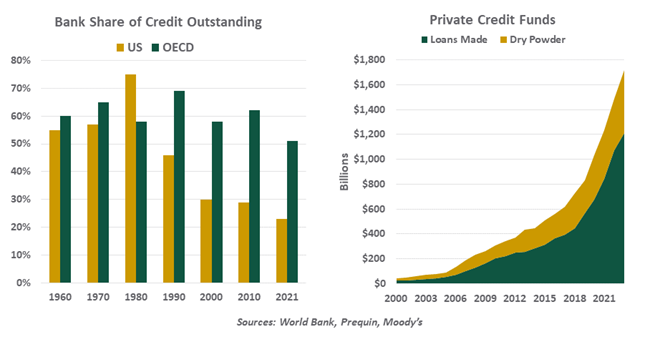

AS BANKS HAVE RETREATED, PRIVATE LENDING HAS ADVANCED.

Private credit is a natural extension of this trend. Mid-sized companies are typically not large enough to issue debt in the marketplace; many of them do not issue public financial statements. For these reasons, middle-market firms still rely on banks for the bulk of their financing

Increasingly, private equity (PE) firms are raising funds from investors, hiring credit underwriting teams (some of which are former bankers) and making loans to smaller businesses. PE firms have long been leaders in financing start-ups, so private credit is a natural graduation for them.

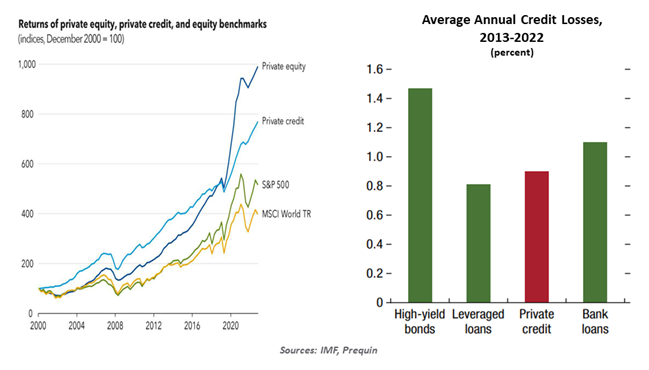

The attractions of private credit to borrowers include tailoring of terms and conditions, speed of execution and flexibility in working through defaults when they occur. The attraction to investors are returns which have exceeded listed equity indices over the past 15 years with lower levels of volatility. And losses on loans originated through private credit have been lower than those originated by banks.

It is important to note that while the growth of private credit has been more pronounced in the United States, other markets are following along. According to credit rating agency Moody’s, Europe’s private lending market has doubled over the past five years, to $448 billion. The practice in Asia is also growing quickly.

Observers and overseers of financial stability have significant concerns about private credit. For one thing, it is hard to gauge what is going on in this space.

Banks are heavily regulated by a range of overseers. As public companies, they are required to file financial statements. Banks file broad information on credit portfolios with regulators each quarter. By comparison, private credit funds are lightly regulated, have no public disclosure requirements and provide their investors with very little portfolio information. The opacity of this sector has prompted some owners (pension funds and insurance companies, for example) to consider holding larger buffers against prospective losses.

THERE IS CONCERN OVER HOW PRIVATE CREDIT WILL FARE UNDER STRESSFUL CONDITIONS.

There are several layers of leverage surrounding private credit that would have to be peeled back under adverse conditions. Sponsors of private credit products often have lines of credit from the banking system, both for contingencies and to enhance returns. Owners of private credit products may have leveraged their holdings to gain additional yield. Because shares in private credit funds are generally illiquid, owners may seek liquidity from banks should a correction occur. The channel has grown substantially since the last significant credit downturn, which leaves room for doubt over how it would fare under adversity.

Further, revelations of trouble in the private credit arena might trigger psychological contagion that would spread more broadly through financial markets. For all of these reasons, systemic supervisors and observers have expressed apprehension over the rapid growth in non-bank lending. Analyses published by the Federal Reserve, the Bank of England and the International Monetary Fund have highlighted the vulnerability that might be latent in this area.

The industry defends itself by noting that private capital can be a source of stability in bad environments. Distressed debt funds step in to acquire loans which are faltering, placing a floor under debt prices and providing price discovery amid illiquidity.

Private lenders are certainly not sharks preying on unsuspecting borrowers, but they could leave a trail of unsuspecting victims in a worst-case scenario. Better to know what’s going on beneath the water line before trouble surfaces.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All