I think that if I didn’t have bad luck, I would have no luck at all. Every time I travel internationally, the U.S. dollar depreciates against the currencies of the countries I will be visiting. At times, the cost of a light breakfast exceeds the daily meal allowance in our expense system.

I have an overseas trip coming up, but it looks like my fortunes may change. The U.S. dollar has been on quite a run this year, gaining ground against a broad range of its rivals. This development is easy to understand at one level, but surprising at another.

The American economy has been the best performer among major developed markets for well over a year. Growth continues to be fueled by consumers, who are enjoying sizeable real wage gains and appreciation of their investments. Government spending in the United States is escalating at a much faster pace than is the case in other nations, adding to aggregate demand.

Capital is also flowing into the U.S. Equity markets have gained, led by a technology sector which is leading innovation. And yields on Treasury securities remain very attractive, especially after increasing in the wake of revised expectations of Fed policy. Interest rate differentials between markets can be a catalyst for inbound investing, which requires trading into the U.S. dollar.

While beneficial to America (and its outbound business travelers), recent developments in the foreign exchange market have been problematic for a number of other countries. The prices of many essential commodities, including oil, are denominated in dollars; the strength of the dollar raises import costs abroad. Debt repayments on dollar-denominated borrowing have become more taxing for some emerging markets.

Preserving the strength of local currencies has led overseas central banks to keep rates higher than they would prefer, even though local inflation is benign. Economic performance in those areas is therefore at some risk. Countries with adequate reserves have been forced to intervene actively to keep their currencies from depreciating; China has been defending the yuan for some time now, and Japan likely intervened this week after the yen hit a 34-year low.

In these latter two cases, local authorities were probably anxious to dispel notions that they welcomed a weaker exchange rate. In recent decades, China and Japan have occasionally been accused of improving their terms of trade by steering their currencies lower; this risks retribution (often in the form of tariffs) from their export partners. In the present day, however, the realignment seems attributable to natural market forces and not intervention.

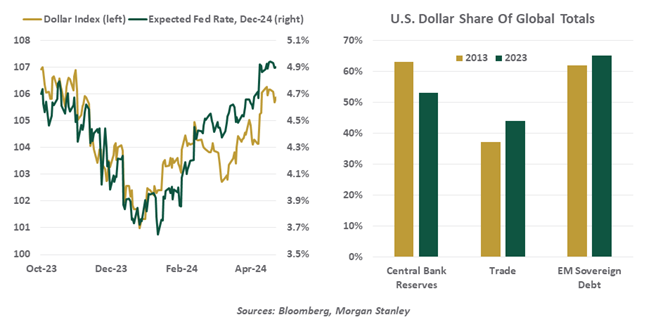

DESPITE A TROUBLING DEBT OUTLOOK, THE U.S. DOLLAR STILL REIGNS SUPREME.

While the dollar’s improvement is consistent with economic fundamentals, it is somewhat surprising when viewed in a broader context. The United States is dealing with a significant long-term debt problem and a disappointing lack of resolve in addressing it. The use of economic sanctions to punish bad actors has led some countries to dissociate themselves from the dollar and the financial systems centered around it. The development of digital currencies allows transacting without foreign exchange conversion, which also serves to take the edge off dollar dominance.

In spite of all this, the U.S. dollar remains the world leader by a wide margin. Its shares of central bank reserves, trade transactions and non-native debt issuance remain substantial, topping its nearest competitors by a wide margin. This may have more to do with weakness among alternatives, as opposed to the unquestioned strength of the dollar. For better or worse, currencies are graded on a curve, and the dollar is still the best relative brand.

The head of Northern Trust’s foreign exchange department visited me last year, and asked if I could keep him current on my travel schedule. Ever since, his group has enjoyed unusual success advising clients to take long positions in the currencies of the countries I visit. I’ve asked for a share of the fees, but so far, no luck.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Northern Trust

Read more commentaries by Northern Trust