Election Years Create Their Own Patterns

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIn this article, Russ Koesterich discusses how momentum and election cycles may shift the impact and timing of seasonal trends.

Key takeaways

- YTD stock returns have been driven by earnings growth, supported by a resilient economy. That said, traditional seasonal factors would indicate caution in the near-term.

- Historically, May through September tends to be the weakest period for stocks. During election years, summer weakness often shifts to the fall.

- Strong market momentum and a resilient economy may keep stocks in positive territory, or at least until the fall when the election gains more focus.

Stocks have recently struggled with higher rates, but year-to-date, 2024 has gotten off to a decent start. While several parts of the market, notably small caps, have been left behind, as of mid-April the S&P 500 is up roughly 6%.

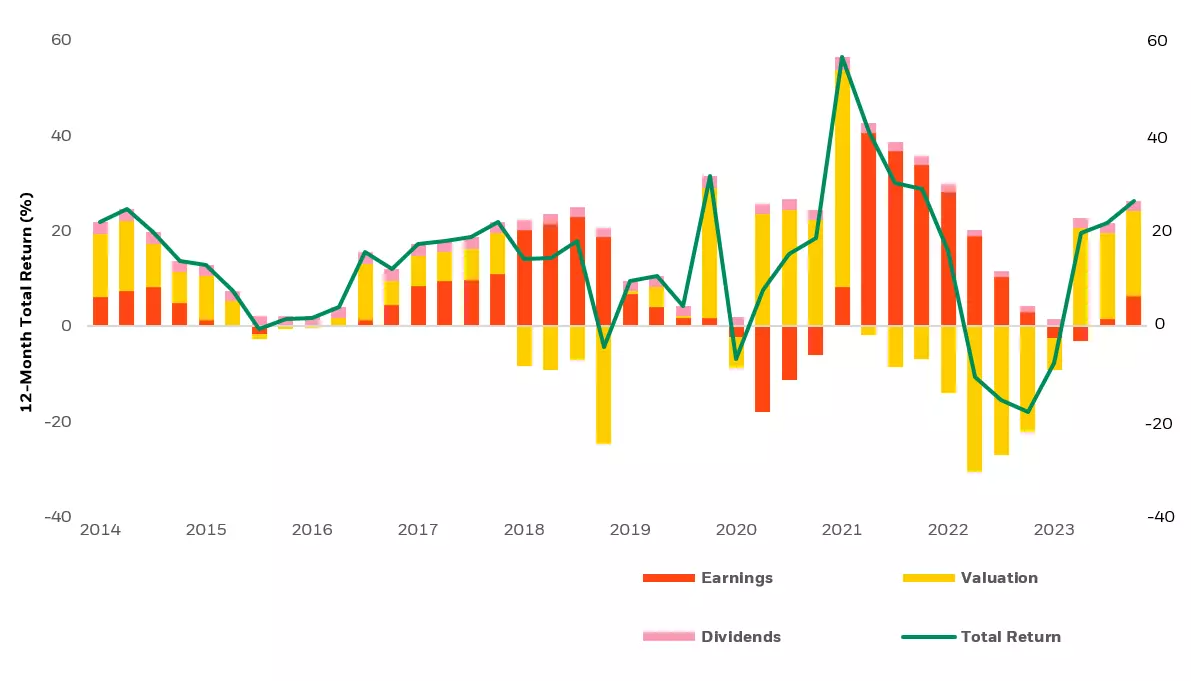

While stocks continue to rise, the driver of returns has shifted. Last year’s gains were powered by higher valuations. This year a solid economy is allowing for stronger earnings, which are increasingly driving returns for US stocks (see Chart 1).

S&P 500 sources of total return

Source: LSEG Datastream, S&P 500 and BlackRock Investment Institute Apr 18, 2024

Notes: The bars show the breakdown of the S&P 500 12-month return into dividends, earnings growth and

Valuation (multiple). Earnings growth is based on the 12-month change in 12-month forward I/B/E/S earnings

Estimates. Returns are based on the S&P 500 index.

That said, particularly in the near-term sentiment matters. Investors are understandably nervous given rising rates, a change in the Federal Reserve narrative and elevated geopolitical risk. While not rising to the same level of importance, investors may also be worried about the calendar.

As discussed in previous blogs, while the seasonal impact on stocks can be exaggerated, in the past returns have often followed seasonal patterns. Since 1960, the May through September period tends to be the weakest. Average monthly price returns during those months are approximately 0.10%, versus roughly 1% for all other months. In short, the old maxim, ‘Sell in May and Go Away’ has some validity.

Momentum and the election

While seasonal factors can matter, and certainly did in 2023, other forces can shift the impact and timing of seasonal trends. As we move into spring, two other factors are worth watching: momentum and the election. Starting with momentum, seasonal weakness tends to be more muted in month’s when the market has risen strongly in the preceding 12 months. Since 1960 average monthly returns are approximately twice as high in the spring and summer months when 12-month momentum is 10% or more. As of mid-April, S&P 500 12-month returns were still north of 20%, suggesting good momentum going into the late spring and summer.

The other potential mitigating factor may be the election cycle, which has its own internal logic. With the caveat that results should be treated cautiously given fewer observations, in past election cycles summer weakness often shifts to the fall. Said otherwise, historical election year’s have witnessed solid returns in June, July, and August before returns turned negative in September and October.

Intuitively, this makes some sense. While political junkies may be fixated on every primary machination, most people, including most investors, pay far less attention until the party conventions begin and the fall campaign starts. It is at this point polls become more significant, and investors start to pay more attention to the implications of the potential outcomes.

Near-term investment implications

If historical patterns hold near-term, seasonal market weakness may not necessarily be a prelude to a bigger summer correction. Instead, market momentum and a strong economy may keep stocks in positive territory, or at least until the full significance of the election starts to become apparent in the fall.

To obtain more information on the fund(s) including the Morningstar time period ratings and standardized average annual total returns as of the most recent calendar quarter and current month-end, please click on the fund tile.

The Morningstar Rating for funds, or "star rating," is calculated for managed products (including mutual funds, variable annuity and variable life subaccounts, exchange-traded funds, closed-end funds, and separate accounts) with at least a three-year history. Exchange-traded funds and open-ended mutual funds are considered a single population for comparative purposes. It is calculated based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a managed product's monthly excess performance, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of products in each product category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars, and the bottom 10% receive 1 star. The Overall Morningstar Rating for a managed product is derived from a weighted average of the performance figures associated with its three-, five-, and 10-year (if applicable) Morningstar Rating metrics. The weights are: 100% three-year rating for 36-59 months of total returns, 60% five-year rating/40% three-year rating for 60-119 months of total returns, and 50% 10-year rating/30% five-year rating/20% three-year rating for 120 or more months of total returns. While the 10-year overall star rating formula seems to give the most weight to the 10-year period, the most recent three-year period actually has the greatest impact because it is included in all three rating periods.

About the Author

Russ Koesterich, CFA, JD

Russ Koesterich, CFA, JD, Managing Director and portfolio manager, is a member of the Global Allocation team.

Mr. Koesterich's service with the firm dates back to 2005, including his years with Barclays Global Investors (BGI), which merged with BlackRock in 2009. He joined the BlackRock Global Allocation team in 2016 as Head of Asset Allocation and was named a portfolio manager of the Fund in 2017. Previously, he was BlackRock's Global Chief Investment Strategist and Chairman of the Investment Committee for the Model Portfolio Solutions business, and formerly served as the Global Head of Investment Strategy for scientific active equities and as senior portfolio manager in the U.S. Market Neutral Group. Prior to joining BGI, Mr. Koesterich was the Chief North American Strategist at State Street Bank and Trust. He began his investment career at Instinet Research Partners where he occupied several positions in research, including Director of Investment Strategy for both U.S. and European research, and Equity Analyst. He is a frequent contributor to financials news media and the author of two books, including his most recent "The Ten Trillion Dollar Gamble."

Mr. Koesterich earned a BA in history from Brandeis University, a JD from Boston College and an MBA from Columbia University. He is a CFA Charterholder.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All