I’ve just concluded two weeks of client briefings in Florida. We covered nine cities, spread across more than 700 miles. It was a challenging itinerary, but it was a treat to visit with so many clients and partners.

I did get a respite during a weekend in Key West, which features a buoy marking the southernmost point of the continental United States. I thought of that icon as I reflected on the fortnight of conversations. The most frequently asked question (by far) was how much further south the finances of the United States might drift in the years ahead.

We’ve covered some of the issues related to America’s fiscal crisis in recent months. (Two entries in that catalogue can be found here and here.) Clients raised some additional questions about the national debt, answers to which I thought it would be useful to share formally.

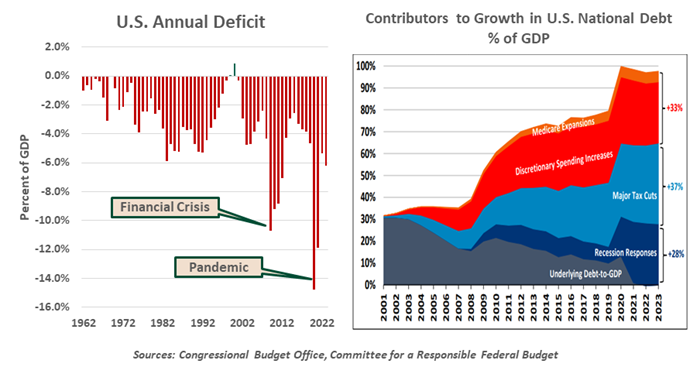

How did we get into so much debt? It is hard to recall, but the United States had a budget surplus in the year 2000. But rather than use the excess to retire debt or shore up Social Security, Congress chose to rebate the amount (and then some) to taxpayers and initiate new programs. That re-started the red ink, which has flowed freely ever since.

PROGRESS ON THE NATIONAL DEBT WILL REQUIRE COMPROMISES ON BOTH TAXES AND SPENDING.

The Committee for a Responsible Federal Budget estimates that tax cuts and spending increases have added debt equal to 70% of gross domestic product (GDP) during this century. Had those measures not been taken, the national debt might have been retired by now.

The magnitude of the debt is even more frightening when viewed in the context of very strong economic and market performance during the past two decades. We may not be able to count on that kind of performance persisting into the future.

Whose fault is it? It is certainly tempting to lay blame for deepening deficits at the feet of one party or another, and plenty of people do. But leaders of both parties have contributed to the situation. The four presidents who have served during the 21st century are responsible for about 70% of our national debt. Two of them have been Republicans, and two have been Democrats. During the past 23 years, the Senate has been in Republican hands for 12 years, and the House has been led by the GOP for 15 years. The bottom line: neither party can claim a high road when it comes to fiscal discipline.

The early polls suggest that divided government is the most likely outcome of this year’s U.S. election. Further, recent history suggests that neither party is likely to have full control over the government for very long. What this illustrates clearly (at least to me) is that a durable solution can only come through collaboration between the parties. The two sides are going to have to compromise if lasting progress is to be mde.

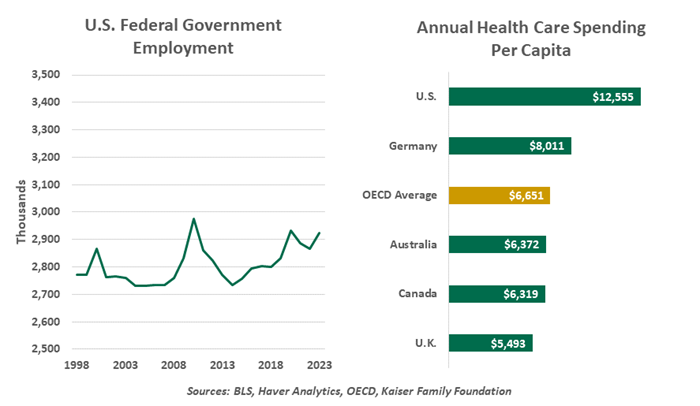

Why is it so hard to shrink the size of government? Some people gauge the size of government by the number of federal employees. By that metric, government hasn’t grown much at all in the last 35 years. It is the scale of government programs that has mushroomed.

SHRINKING GOVERNMENT WILL REQUIRE TACKLING ENTITLEMENT PROGRAMS.

Discretionary spending that is not related to defense accounts for 15% of federal outlays. A review of this segment is certainly warranted, but meaningful spending discipline cannot be achieved without tackling the other 85%: defense, Social Security, Medicare/Medicaid, and interest. Defense is a poor candidate for cuts amid geopolitical uncertainty, and interest on the debt can’t be reduced by fiat. That leaves the two big entitlement programs.

Social Security has required significant restructuring on three occasions since 1977. Each time, some combination of changes to eligibility, retirement ages, payroll taxes and benefit levels was employed to return the system to long-term solvency. Means-testing benefits has some appeal, as Social Security is an insurance program, not an entitlement program. (People do not have individual Social Security accounts, despite popular perception; the system relies on working age people paying retirees.)

The good news is that longevity in the United States has improved, and the new class of GLP-1 drugs (like Ozempic and Mounjaro) are likely to extend life spans. But the average American now spends almost 20 years as a retired person, as opposed to about 13 years when Social Security was initiated.

Medicine is considerably more complicated. The United States spends almost twice as much per capita per year than the average developed country on health care, but outcomes (life expectancy, infant mortality, the incidence of chronic disease) are often worse. Stakeholders in the system agree on one thing: we are not getting our money’s worth.

A message from Advisor Perspectives and VettaFi: As fixed income dynamics shift, how will you guide your clients through 2024? Discover strategies at the Fixed Income Symposium on April 18. Click here to register.

© Northern Trust

Read more commentaries by Northern Trust