Quality Is Now a Momentum Trade

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIn this article, Russ Koesterich discusses why the current momentum trade, despite stretched valuations, could continue.

Key takeaways

- Year to date, technology related companies have been the market leaders, with an increased focus on the ability to generate cash-flow. From a style factor lens, momentum has been the winner.

- Historically, this style has often been associated with more speculative, lower-quality parts of the market. Today, momentum names are increasingly high-quality businesses with consistent profitability – something investors are willing to pay a premium for.

Markets have been on a tear, driven by solid earnings and a benign economic backdrop. And while a chorus of commentators is increasingly pointing to a replay of the late 1990’s technology bubble, there is one important difference: cash flow generation. Today’s technology related market leaders are incredibly powerful businesses levered to long-term secular trends. While this does not guarantee perpetual dominance, and valuations do ultimately matter, we believe it can support the trend to continue in the near-term.

I last discussed the technology (tech) sector in November of last year. At the time the market was still trying to recover from last fall’s backup in U.S. long-term interest rates. My view at the time was that tech might provide a measure of safety in a volatile market.

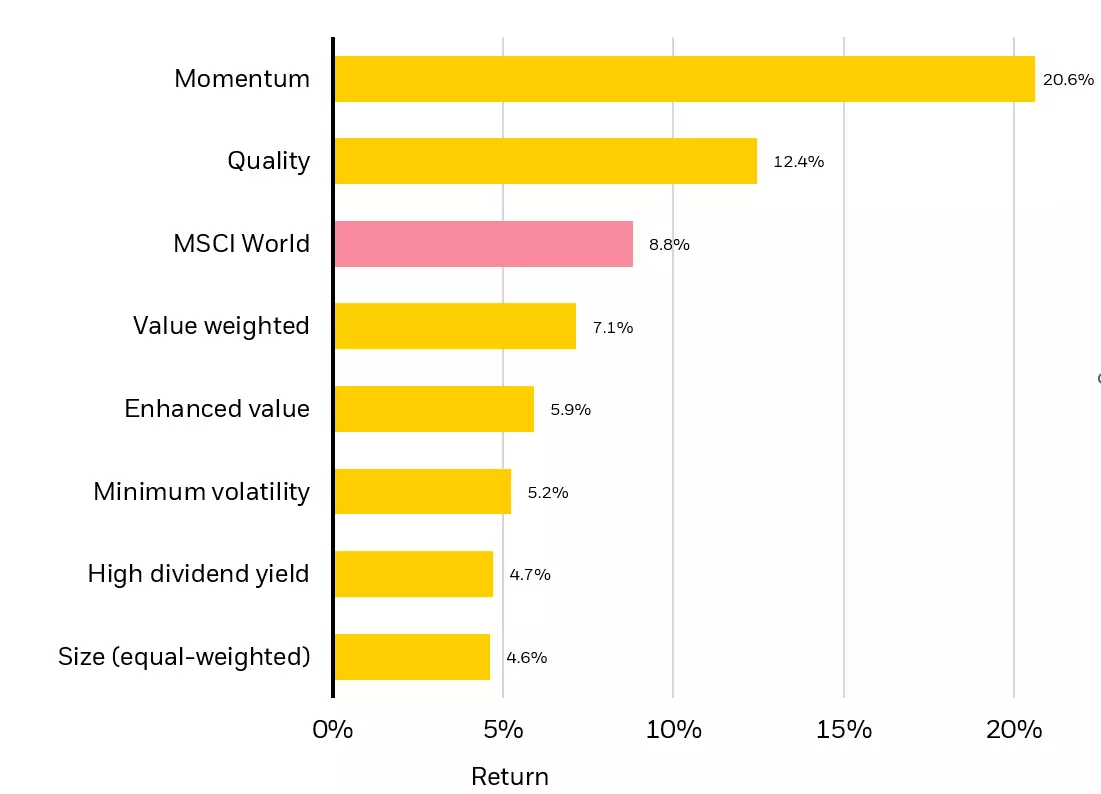

While markets have rallied sharply since then, the same logic holds. Tech and tech-related names are still benefiting from the generation of high-quality cash-flow, something most investors prioritize in the current environment. Adding to this subset buying, year-to-date a new group of investors have been chasing this trend: momentum players (see Chart 1).

Momentum investors typically focus on stocks that are rising the fastest, often using a one-year time frame to measure. Last year the momentum factor struggled relative to other investment styles. Chasing trends was difficult when the economic and market narrative kept shifting every few months.

More recently, as recession fears fade and a soft-landing seems to be taking hold, momentum has enjoyed a resurgence. The investment style has also been supported by an increasing fixation on long-term structural themes, notably artificial intelligence. As a result, year-to-date, momentum has significantly outperformed other investment styles, such as value investing (see Chart 1).

MSCI World factor index performance - year to date

Source: LSEG Datastream, chart by BlackRock Investment Institute, Mar 19, 2024

What is interesting about the current rally is the composition of the companies included in the momentum trade. In the past, momentum has often been associated with more speculative, lower-quality parts of the market. Today, momentum names are increasingly high-quality companies, i.e., firms defined by high profitability, consistent earnings, and relatively low debt. This dynamic is evident in the increasing representation of highly profitable companies, as measured by return-on-equity, ROE, in momentum strategies measure of a company's net income divided by its shareholders' equity ).

We see a similar pattern using more granular systematic signals. Based on research by the Global Allocation systematic research team, the top performing signals in Q1’24 have mostly been tied to cash-flow momentum and earnings. Based on this research, some of the best performing systematic signals are cash-flow momentum, analyst revisions, margin consistency and stable revenue growth. Put differently, investors are investing in companies generating strong cash-flow and consistent earnings.

Momentum may have further to go.

The rally in mega-cap growth has been going on for some time. For many of these names, valuations appear stretched, if not outright expensive. That said, company fundamentals underpinning the rally are still very much in place. To the extent many of these businesses are levered to long-term trends such as artificial intelligence, semiconductors (a key component in AI enablement), internet commerce, and innovations in pharmaceuticals, the momentum trade may continue a bit longer.

To obtain more information on the fund(s) including the Morningstar time period ratings and standardized average annual total returns as of the most recent calendar quarter and current month-end, please click on the fund tile.

The Morningstar Rating for funds, or "star rating," is calculated for managed products (including mutual funds, variable annuity and variable life subaccounts, exchange-traded funds, closed-end funds, and separate accounts) with at least a three-year history. Exchange-traded funds and open-ended mutual funds are considered a single population for comparative purposes. It is calculated based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a managed product's monthly excess performance, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of products in each product category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars, and the bottom 10% receive 1 star. The Overall Morningstar Rating for a managed product is derived from a weighted average of the performance figures associated with its three-, five-, and 10-year (if applicable) Morningstar Rating metrics. The weights are: 100% three-year rating for 36-59 months of total returns, 60% five-year rating/40% three-year rating for 60-119 months of total returns, and 50% 10-year rating/30% five-year rating/20% three-year rating for 120 or more months of total returns. While the 10-year overall star rating formula seems to give the most weight to the 10-year period, the most recent three-year period actually has the greatest impact because it is included in all three rating periods.

About the Author

Russ Koesterich, CFA, JD, Managing Director and portfolio manager, is a member of the Global Allocation team.

Mr. Koesterich's service with the firm dates back to 2005, including his years with Barclays Global Investors (BGI), which merged with BlackRock in 2009. He joined the BlackRock Global Allocation team in 2016 as Head of Asset Allocation and was named a portfolio manager of the Fund in 2017. Previously, he was BlackRock's Global Chief Investment Strategist and Chairman of the Investment Committee for the Model Portfolio Solutions business, and formerly served as the Global Head of Investment Strategy for scientific active equities and as senior portfolio manager in the U.S. Market Neutral Group. Prior to joining BGI, Mr. Koesterich was the Chief North American Strategist at State Street Bank and Trust. He began his investment career at Instinet Research Partners where he occupied several positions in research, including Director of Investment Strategy for both U.S. and European research, and Equity Analyst. He is a frequent contributor to financials news media and the author of two books, including his most recent "The Ten Trillion Dollar Gamble."

Mr. Koesterich earned a BA in history from Brandeis University, a JD from Boston College and an MBA from Columbia University. He is a CFA Charterholder.

Carefully consider the Funds' investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Funds' prospectuses or, if available, the summary prospectuses, which may be obtained by visiting the iShares Fund and BlackRock Fund prospectus pages. Read the prospectus carefully before investing.

Investing involves risk, including possible loss of principal.

Principal Risks: The fund is actively managed and its characteristics will vary. Stock and bond values fluctuate in price so the value of your investment can go down depending on market conditions. International investing involves special risks including, but not limited to currency fluctuations, illiquidity and volatility. These risks may be heightened for investments in emerging markets. Fixed income risks include interest rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments. Non-investment grade debt securities (high yield/junk bonds) may be subject to greater market fluctuations, risk of default or loss of income and principal than higher-rated securities. Asset allocation strategies do not assure profit and do not protect against loss. Short selling entails special risks. If the fund makes short sales in securities that increase in value, the fund will lose value. Any loss on short positions may or may not be offset by investing short sale proceeds in other investments. The fund may use derivatives to hedge its investments or to seek to enhance returns. Derivatives entail risks relating to liquidity, leverage and credit that may reduce returns and increase volatility.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of April 2024 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader.

Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. You cannot invest directly in an index.

The BlackRock Model Portfolios are provided for illustrative and educational purposes only, do not constitute research, investment advice or a fiduciary investment recommendation from BlackRock to any client of a third party financial advisor (each, a "Financial Advisor"), and are intended for use only by such Financial Advisor as a resource to help build a portfolio or as an input in the development of investment advice from such Financial Advisor to its own clients and shall not be the sole or primary basis for such Financial Advisor’s recommendation and/or decision. Such Financial Advisors are responsible for making their own independent fiduciary judgment as to how to use the BlackRock Model Portfolios and/or whether to implement any trades for their clients. BlackRock does not have investment discretion over, or place trade orders for, any portfolios or accounts derived from the BlackRock Model Portfolios. BlackRock is not responsible for determining the appropriateness or suitability of the BlackRock Model Portfolios or any of the securities included therein for any client of a Financial Advisor. Information and other marketing materials provided by BlackRock concerning the BlackRock Model Portfolios –including holdings, performance, and other characteristics –may vary materially from any portfolios or accounts derived from the BlackRock Model Portfolios. Any performance shown for the BlackRock Model Portfolios does not include brokerage fees, commissions, or any overlay fee for portfolio management, which would further reduce returns. There is no guarantee that any investment strategy will be successful or achieve any particular level of results. The BlackRock Model Portfolios themselves are not funds. The BlackRock Model Portfolios, allocations, and data are subject to change.

For financial professionals: BlackRock’s role is limited to providing you or your firm (collectively, the “Advisor”) with non-discretionary investment advice in the form of model portfolios in connection with its management of its clients’ accounts. The implementation of, or reliance on, a Managed Portfolio Strategy is left to the discretion of the Advisor. BlackRock is not responsible for determining the securities to be purchased, held and sold for a client’s account(s), nor is BlackRock responsible for determining the suitability or appropriateness of a Managed Portfolio Strategy or any securities included therein for any of the Advisor’s clients. BlackRock does not place trade orders for any of the Advisor’s clients’ account(s). Information and other marketing materials provided to you by BlackRock concerning a Managed Portfolio Strategy—including holdings, performance and other characteristics–may not be indicative of a client’s actual experience from an account managed in accordance with the strategy.

For investors: BlackRock’s role is limited to providing your Advisor with non-discretionary investment advice in the form of model portfolios in connection with its management of its clients’ accounts. The implementation of, or reliance on, a Managed Portfolio Strategy is left to the discretion of your Advisor. BlackRock is not responsible for determining the securities to be purchased, held and sold for your account(s), nor is BlackRock responsible for determining the suitability or appropriateness of a Managed Portfolio Strategy or any securities included therein. BlackRock does not place trade orders for any Managed Portfolio Strategy account. Information and other marketing materials provided to you by BlackRock concerning a Managed Portfolio Strategy—including holdings, performance and other characteristics—may not be indicative of a client’s actual experience from an account managed in accordance with the strategy. This material is subject to change.

Prepared by BlackRock Investments, Inc. LLC. Member FINRA

©2024 BlackRock, Inc or its affiliates. All rights reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

USRRMH0424U/S-3491438

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All