March US consumer prices rose faster than expected. The reacceleration in supercore inflation suggests the strong inflation readings at the start of the year may not have been mere blips. Franklin Templeton Fixed Income Economist Nikhil Mohan expects the Federal Reserve will likely begin rate cuts in September, but inflation trends may affect the timing of the cuts.

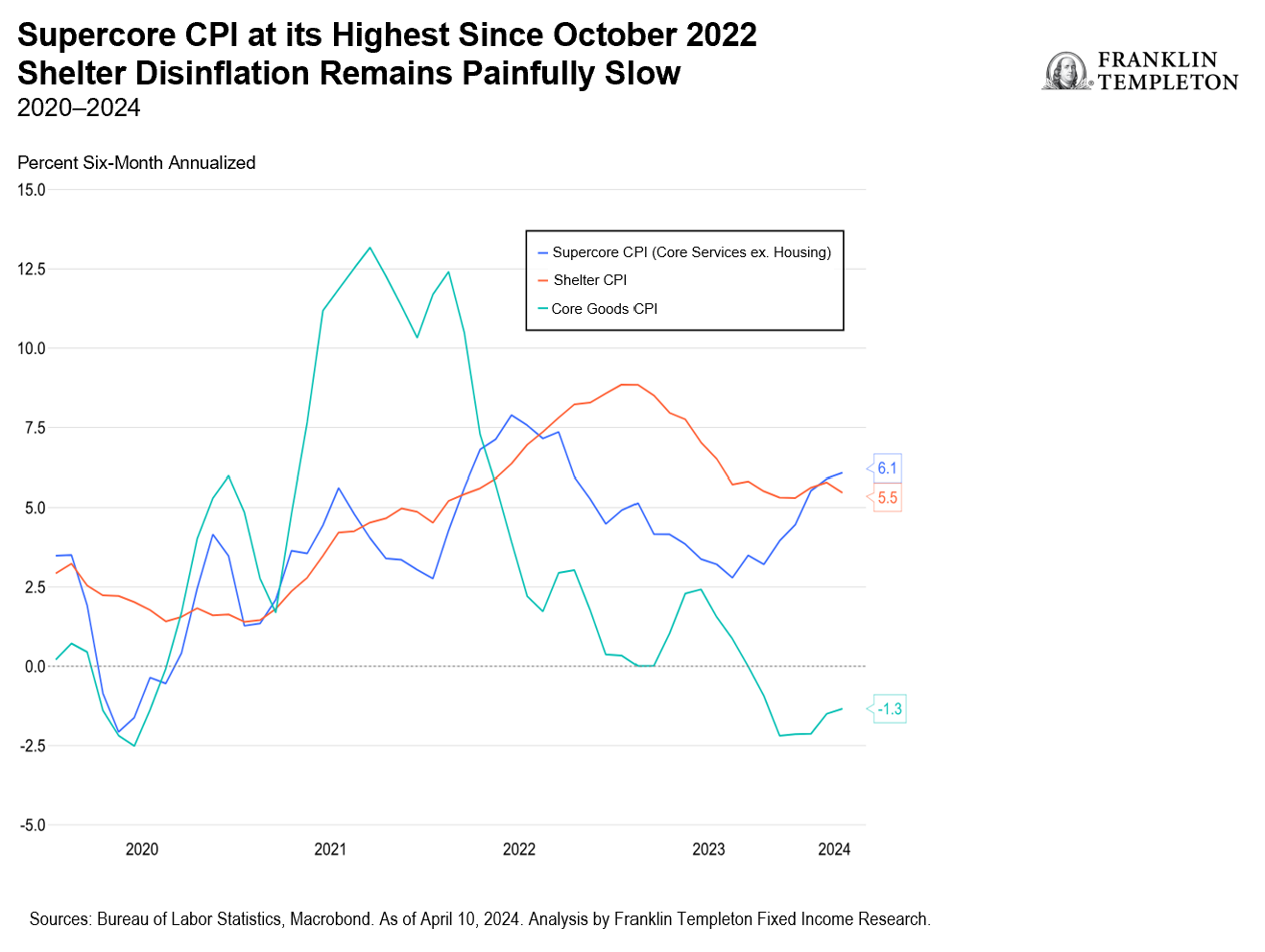

On a monthly basis, US headline and core Consumer Price Index (CPI) topped expectations—both rising 0.4%. The core measure has now risen at that pace for three successive months. While the pace of increase remained unchanged at 0.5% for core services (which is still more than double the 2012–2019 average), the pace of increase for the supercore measure (core services excluding housing) accelerated to 0.7%. Transportation, medical and other personal services largely drove the rise. On a six-month annualized basis, core CPI is now near 4%, while supercore CPI inched above 6% (the highest since October 2022) and has been on an uptrend for the past five months.

Although shelter inflation ticked marginally lower, the pace of disinflation remains painfully slow. Owner-occupied rents saw another 0.4% month-over-month (m/m) increase. For rents on primary residences, there was a slight downshift in the pace of increase. However, the six-month annualized measures are still running well above 5% and closer to 6% on a year-over-year (y/y) basis.

Core goods CPI turned negative once again (-0.2% m/m). This was primarily due to declines in prices for new and used vehicles, auto parts, recreational, and information technology goods. The one silver lining is that, on a y/y basis, core goods inflation has turned increasingly deflationary—running well below its 2012–2019 average.

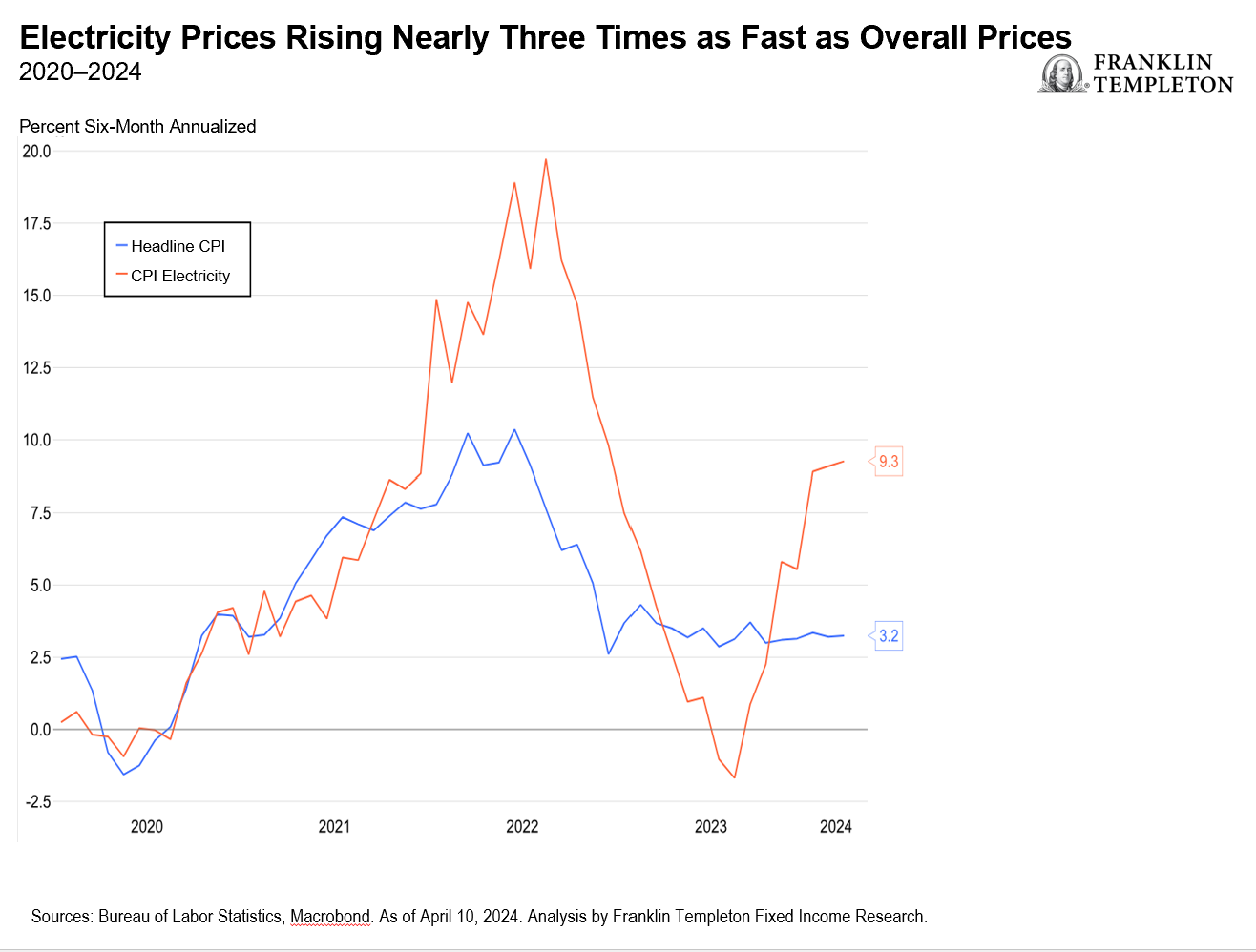

While energy services has slowed since the beginning of the year, the 0.7% m/m increase is still particularly elevated. The six-month annualized and yearly pace rose to 9.7% and 3.1%, respectively. What’s concerning to us is that there has been increasing anecdotal evidence suggesting that households are having to shell out more for electricity. Utility companies have been aggressively upgrading/expanding the existing grid network and decarbonizing. This cost of expansion and upgradation is ultimately falling on end-users.

As for Federal Reserve policy rate expectations, our base case has increasingly turned toward a September cut and 50 basis points (bps) of cuts in total this year. The March inflation print further reinforces that view. Over the past few months, markets too have inched closer to our view—June and July rate-cut expectations have been trimmed significantly after the latest CPI release, and just about 50 bps of rate cuts have been priced in for the year.1 However, if inflation were to continue reaccelerating and/or stall at its current pace, we wouldn’t rule out a further delay in rate cuts (beyond September).

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Fixed income securities involve interest rate, credit, inflation and reinvestment risks, and possible loss of principal. As interest rates rise, the value of fixed income securities falls. Low-rated, high-yield bonds are subject to greater price volatility, illiquidity and possibility of default.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S.: Franklin Resources, Inc. and its subsidiaries offer investment management services through multiple investment advisers registered with the SEC. Franklin Distributors, LLC and Putnam Retail Management LP, members FINRA/SIPC, are Franklin Templeton broker/dealers, which provide registered representative services. Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com.

__________

1. Source: CME Group fed funds futures market, as of April 10, 2024. There is no assurance any estimate, forecast, or projection will be realized.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Franklin Templeton

Read more commentaries by Franklin Templeton