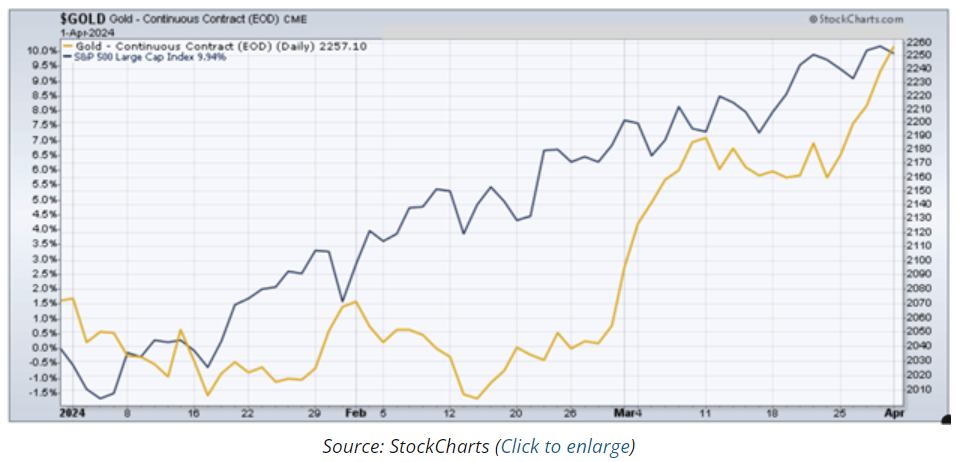

Gold started this week at an all-time high. It’s up about 10% since the start of the year. That’s roughly on par with the S&P 500. All of this while inflation is trending down (with some bumps).

Demand for gold is not coming from individuals, but from central banks. Money flows from ETFs that hold gold have been negative since 2020, while central banks are adding record amounts of gold. The Central Bank of China, in particular, has been a big buyer. Why is that?

Gold is widely accepted as a store of value. Banks can hold gold without political or credit risk. There’s nothing particularly new or revealing about that. But what if gold’s latest popularity is signaling its return to being used as an actual currency—a means of exchange among nations looking to settle trade outside of the US dollar?

Settling trade in gold is one way to thwart US sanctions and avoid the global SWIFT payment system. Iran selling oil for gold is a standout example.

China has a big incentive to derisk from the US dollar. The OEC reports that in 2022, China exported $3.73 trillion worth of goods, while importing only $2.16 trillion. That imbalance results in a massive surplus of foreign currency—mostly dollars, which have to go somewhere. Some of China’s other trading partners, particularly Russia and Iran, don’t find dollars very useful.

There are nations who need to secure grains, uranium, potash, and oil from Russia, one of the world’s largest producers of these and other crucial commodities. But trading with Russia is not easy. It is under US sanctions, and US dollars aren’t very helpful or desirable for Russia at the moment.

To facilitate trade, Russia has to accept a certain level of foreign currencies, or convince trading partners to deal in rubles. Russia’s central bank cannot get overweight any single currency. Indian rupees, Brazilian reals, and Iranian rials only go so far on the global market.

Gold, however, is accepted everywhere. And it doesn’t leave a paper trail.

I once toured a Brinks vault, where I saw pallets of 400 troy ounce gold bars stacked 20 feet high, held kilogram bars (2.2-pound slabs the size of a small iPhone), and even saw a massive gold Euro coin roughly 12 inches in diameter and too heavy for one man to easily lift.

I have to admit, gold is intoxicating. As an investment, it can also be incredibly frustrating (just ask Jared). A lot of smart investors have waited a long time for gold to work. That long, painful, and frustrating period may finally be over.

Gold as a store of wealth, as a hedge against currency debasement, and a return to its centuries-old role as a tradable currency… these are all powerful reasons for its price to continue climbing higher. Not to mention the massive government deficits in Washington, DC.

I personally hold very little gold. I gave up years ago. I do own gold miners, though, and have for some time. They take investor frustration to new levels.

If you missed the first leg of this gold rally, you are in luck. Shares of gold miners remain cheap. I’ve been adding to my positions and will likely continue doing so. Mining stocks usually lag a big move in gold’s price. Energy is a large cost of mining, and energy prices are also on the move. Still, gold miners could be a great trade at current prices.

Unless you have real expertise in this field, don’t make this more complicated than it needs to be. Buy a big, well-managed, major gold miner. Then wait. I own Barrick, but it could also be Newmont or Franco-Nevada. A more diversified option is an ETF of gold miners, such as the VanEck Gold Miners ETF (GDX).

Grant Williams is one of the world’s most eloquent speakers on all things gold. He’ll be interviewing the great Felix Zulauf at our Strategic Investment Conference, and I suspect gold will be discussed.

Our conference, by the way, is once again virtual. You can join no matter where in the world you are, watch live, and get immediate access to session recordings. If you haven’t yet registered, I hope you’ll do so now. You can see all our speakers and learn more about our featured sessions here. I’ll be your co-host, along with “El Jefe” John Mauldin.

In addition to being what I humbly claim to be the best annual financial conference, the SIC is also one of the most financially important events of our year. It pays for much of the writing, research, and ideas you find in your inbox every week from myself, John Mauldin, and the other team members here at Mauldin Economics. We appreciate your support and hope to see you (virtually) at the 20th annual Strategic Investment Conference.

Please join us!

Ed D’Agostino

Publisher & COO

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Mauldin Economics

Read more commentaries by Mauldin Economics