Last week, the U.S. Congress completed work on the country’s budget for fiscal year 2024. Good thing: the government’s fiscal year is almost halfway over.

After all the hand-wringing (and near-shut downs) over increasing deficits, the outline calls for nearly $6.5 trillion in spending this year. That represents more than 23% of the country’s gross domestic product (GDP). The Congressional Budget Office projects a shortfall of $1.5 trillion (5.6% of GDP) for this fiscal year. Both of these levels are very high by historical standards.

This outcome might give one the impression that legislators have no limits when it comes to budgeting and borrowing. That may be overly harsh, but the way Congress views major programs may be in need of an overhaul.

When initiatives are proposed, they are subject to “scoring,” which estimates their impact on the budget. At a basic level, measures are judged by the direct effect they have on revenue or spending. Under this “static” approach, a tax cut or spending increase would be viewed as increasing annual deficits.

But those who support these proposals contend that they would generate increased levels of economic growth, broadening the tax base and producing additional revenue. In an attempt to capture these effects, “dynamic” scoring can be used. The dynamic part refers to after-effects that might make the analysis more comprehensive, such as the favorable impact of lower tax rates on economic growth. The case for a more interactive approach can be found here.

While theoretically meritorious, performing dynamic scoring is extraordinarily difficult. For example, if taxes are cut, the heightened level of activity could threaten to become inflationary. In that event, the central bank might tighten monetary policy to cool things down, which would restrain the economy and tax collections. Slower growth might prompt higher unemployment, which might prompt the central bank to ease, and so on. The circular relationship between economic variables makes analyzing policy changes challenging.

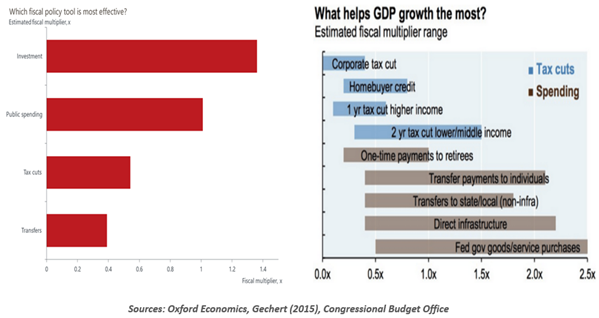

Even with a full inventory of causes and effects, calculating their magnitudes is very difficult. The science (if it can be called that) focuses on “fiscal multipliers,” which relate the cost of a policy to the amount of economic activity it generates. A fiscal multiplier of more than one signifies the program generates incremental output that exceeds its cost. (It should be noted that this is not the same as saying that the program “pays for itself,” since incremental tax revenue is far less than incremental national income.)

Models that estimate fiscal multipliers have a large margin of error, and different models may come up with vastly different conclusions. Political leanings may steer the assumptions used to evaluate policies dynamically.

The range of uncertainty surrounding the process allows sponsors to claim that almost any initiative will be budget friendly. That was the case with the Tax Cuts and Jobs Act (TCJA) of 2017, and it was the case for the major spending programs passed by the Congress in 2022.

CLAIMS THAT TAX AND SPENDING PROGRAMS WILL PAY FOR THEMSELVES HAVE PROVEN INACCURATE.

Verifying these claims is almost impossible. Retrospective studies have to hold a range of other economic influences constant to focus solely on the impact of a specific program. That is exceptionally hard to do. Further, outcomes have to be judged against what would have occurred in the absence of the legislation, which is not directly observable.

To some, the ultimate scoring is the national debt, which is in an uncomfortable place. It seems clear that some or all of the analysis surrounding recent tax and spending legislation was overly optimistic. We will be paying for those mis-projections for a long time. With major fiscal decisions on the horizon (including next year’s consideration of whether to extend some aspects of the TCJA), a much more conservative approach to projecting outcomes would be sensible.

In the years ahead, we might want to familiarize ourselves with mathematical functions other than multiplication. Some addition and subtraction may be needed to put us on a more sustainable fiscal path.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

© Northern Trust

Read more commentaries by Northern Trust