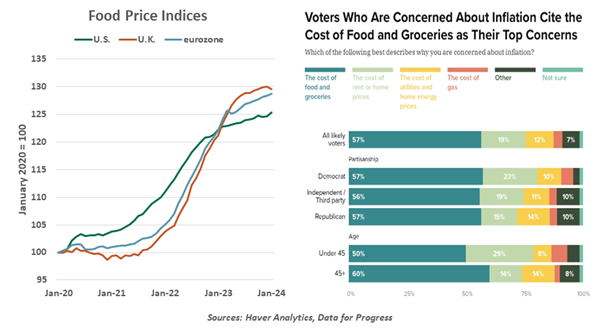

Food prices are dragging down feelings about the economy.

“What goes up, must come down.” That elegant summary of Newton’s second law applies in the physical world, but it does not apply to economics. And that is currently a source of consumer discontent.

In most major economies, inflation is much lower than it was a year ago. The target of 2% is within sight, which should allow interest rates to moderate. Unemployment has not risen much, creating the makings of a soft landing. Asset prices have also been very strong. This combination of outcomes would have been assigned a very low probability a year ago.

Nonetheless, households aren’t at all happy with economic circumstances. Consumer confidence is at low levels in major markets, despite better-than-expected results. Some of the poor sentiment is political, as views about the outlook vary with party affiliation. But some of it is based on markets: supermarkets, not stock markets.

The pandemic affected food prices more than almost any other category. Quarantine forced a shift in distribution from restaurants to grocery stores; illness disrupted processing and distribution. Concerns over food security led to a decline in exports and scant supplies for some commodities.

Other supply shocks piled on. The war in Ukraine hindered shipments of fertilizer used by farmers around the world. An outbreak of avian flu in the United States affected the poultry industry. Across developed markets, grocery prices are about 30% higher than they were at the beginning of 2020. “Shrinkflation,” where product quantities are reduced while prices remain stable, and “skimpflation,” where product quality is reduced, add insult to injury.

Food is a substantial portion of the average family’s budget, and it therefore plays a significant role in perceptions of inflation. (Most people know the prices of milk and eggs, but not the prices of medical care.) Further, while economists focus on changes in prices (inflation), the average person is more attuned to the level of food prices. To many, therefore, inflation hasn’t improved much.

With food supply chains largely back to normal, why haven’t food prices descended toward pre-pandemic levels? A combination of factors are at play:

- Overall demand remains strong. High prices can be a cure for high prices in the grocery aisle, as shoppers trade down to house brands or cheaper ingredients. But rising income levels and asset markets have dulled price consciousness for some households.

- Prices of some food commodities have moderated only slightly from the peaks seen in early 2022. Wholesale prices of most grains are back to price ranges seen prior to the pandemic, but proteins remain expensive. Herds and flocks are smaller than they were four years ago, as the costs of raising them have increased.

- Processing, packaging and transporting products make up about 85% of food costs. Those elements all rely on labor; wages in the industry have escalated faster than the pace of wage gains in the overall labor market. These industries have high levels of turnover and are more likely to rely on immigration than other sectors. Ironically, the high cost of food has led workers in the field to demand higher wages to keep pace.

FOOD COSTS HAVE A HEAVY INFLUENCE ON PERCEPTIONS OF INFLATION.

- A significant fraction of food spending is devoted to eating out. Inflation at those venues is higher than for meals eaten at home, as another layer of labor and distribution costs is involved.

- Some have suggested that increasing concentration in the retail grocery industry has supported “greedflation,” but evidence supporting this is not conclusive. In fact, supermarkets traditionally have very low profit margins, and have been investing heavily in technology to maintain them. Applications range from self-checkout kiosks to AI-driven inventory management systems.

The cost and availability of food has contributed to political change frequently throughout history. There are a lot of elections on the calendar this year; if the price of Newton’s apple doesn’t come down to earth, incumbents may find themselves shopping for new jobs.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Northern Trust

More Large Cap Growth Topics >