Energy and Security

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsEuropean nations still have a long energy transition ahead.

It seems to me that people often choose partners who have a completely different sense of temperature. One is usually too warm; the other, too cold. Wrestling over the thermostat is known to cause challenges for even the best relationships.

Europe has been wrestling with a thermostat challenge ever since the invasion of Ukraine two years ago. It hasn’t been easy, but Europe has managed through two winters without Russian natural gas. The approach of spring should bring seasonal relief, but Europe is still seeking energy and security.

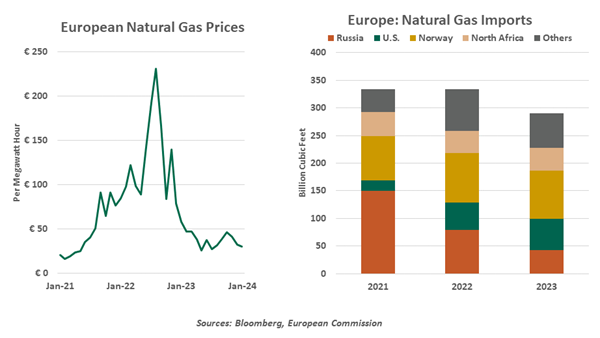

When Western countries sanctioned Russia for its aggression, Russia retaliated by restricting the supply of natural gas to other European countries. At first, key pipelines were taken down for “maintenance;” shortly thereafter, they were closed. In September of 2022, the NordStream pipeline was destroyed in an explosion. This sequence of events initiated a jump in energy prices and a scramble to be ready for winter 2022-23.

EUROPE’S FORCED ENERGY TRANSITION HAS COME AT A SUBSTANTIAL COST.

Matters could have been worse. In the decade prior to the hostilities, Europe had increased the fraction of its electricity derived from renewable sources from 18% to 32%. (This compares to about 25% in the United States.) Nonetheless, Europe generates about 20% of its power from natural gas-fired power plants, and about 30% of its homes are heated with that fuel. Securing replacement supply became an imperative.

Thankfully, Europe succeeded in getting enough natural gas into storage to be ready for seasonal demand. Purchases of liquified natural gas (LNG) from the United States, among others, helped considerably. Conservation measures reduced electricity usage by 10%, and a relatively mild winter limited heating needs. Coal-fired and nuclear power plants were used more heavily. The continent came through last winter with plenty in reserve.

The experience was an expensive one, though. Energy costs in the eurozone’s consumer price index escalated by more than 40% during the first year of the war. Real income of households declined, hampering consumption. A number of countries enacted measures to buffer the blow felt by residents. While welcomed by the recipients, they weren’t entirely popular with economists, who felt that support would dull incentives to conserve and diversify. The programs also added to public debt, the cost of which will be borne by businesses and households in the years ahead.

Rising input costs contributed to the struggles of Europe’s industrial sector. Further, inflation in the euro area peaked at over 10%, prompting a series of interest rate increases from the European Central Bank. This combination of headwinds brought the region’s economy to a standstill; prospects for this year are modest, at best.

The pipeline closures have proven costly to Russia, as well. Oil not sold to Western Europe has been diverted to India, China and other countries. But there are no customers who can fully replace European purchases of Russian natural gas. Exports have fallen by 40%, depriving Russia of a substantial source of revenue. Unfortunately, this deficit has yet to bring either side to the bargaining table.

There is a debate to be had about whether economic sanctions have been worthwhile. The costs to both sides have been significant, especially when lost trade between the two is factored in. Sanctions have a moral component that should not be underestimated, but the costs of weaponizing commerce may not produce sufficient geopolitical returns.

The most recent winter offered a repeat of the preceding one. Europe entered the season with plenty of gas in storage, and winter temperatures were the second highest in the last ten years. The slowing regional economy reduced demand for power, taking further pressure off prices. Homes remained warm, and European energy costs are now deflating.

EUROPE HAS SURVIVED TWO WINTERS WITHOUT RUSSIAN GAS, BUT THERE ARE MANY WINTERS AHEAD.

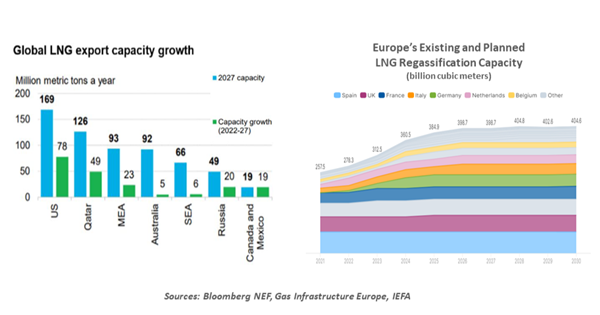

Favorable supply and demand conditions have provided Europe some time to adapt more permanently to life without Russian fuel. European leaders are anxious to sustain progress towards their environmental goals; to that end, investments in alternative energy sources have accelerated. The continent is busily constructing new terminals to receive LNG, and exporters have moved to increase output. Production of LNG is expected to increase by 40% over the balance of this decade.

In January, however, President Biden announced a pause on pending LNG projects. Analysts saw two motivations for the move: one was that supporting dependence on natural gas might slow the transition to fuels that are more environmentally friendly. The second was economic: rising exports have increased natural gas prices in the United States and made them more volatile. The U.S. Energy Information Agency projects a 10% increase in domestic energy costs if LNG exports follow the planned path.

For decades, domestic supplies of natural gas afforded the United States a substantial advantage. The fuel does not travel easily; pipelines must be carefully constructed, and transport by road, rail or sea requires liquification or compression. Investments made to facilitate a more global market have improved energy supply and security for Europe, at the expense of American users.

The current situation illustrates what economists have called the energy “trilemma,” a state in which there are three goals but where only two can be achieved. The world wants cheap energy; it wants clean energy; and it wants to procure energy from reliable sources. Western countries have been seeking to balance these elements since the first Arab oil shocks sixty years ago. Some progress has been made, but much more is needed.

Europe’s energy resilience over the past two years has been impressive, but the future remains uncertain. Downward pressure on thermostat settings and upward pressure on trade relations may not subside for a while.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All