The challenges in banks' portfolios will work out over time.

I am great with faces, but I am terrible with names. Once I see someone, I have near-total recall of past interactions: details about their firms and their families return quickly to mind. But the most critical field in my mental address book is often blank.

On one occasion last year, I referred to Mike, the leader of one of our offices, as “Joe” throughout a client meeting. There were confused looks around the table, which isn’t atypical when I am presenting. When the misnomer was pointed out afterwards, I was terribly embarrassed.

It is a blessing that our recollections of unpleasant experiences eventually fade. That is the point we had reached with the banking crisis of 2023, whose anniversary is approaching. But recent weeks have brought that episode forward in our consciousness. The names have changed, but some of the details are familiar.

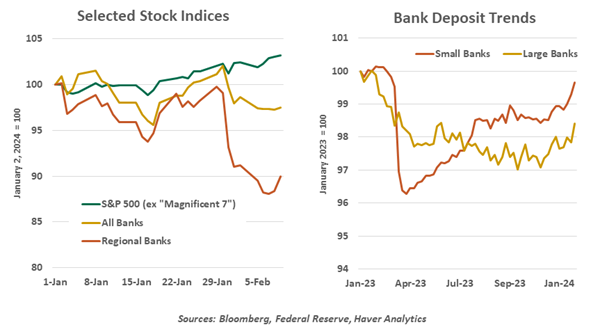

Late winter and early spring of last year were difficult times for the banking industry. The failure of Silicon Valley Bank (SVB) and two others sent shivers through markets. That unfortunate episode had receded into memory, until recent news surrounding New York Community Bank (NYCB) reinstated concerns about the financial sector.

For now, it does not appear that the situation is concerning depositors. In fact, funding at small and regional banks has been increasing of late, counter to the developments of a year ago. This is an encouraging sign that recent events are being placed into proper perspective.

There were two principal concerns at play during last year’s debacle. The first was the impact of higher interest rates on bank profitability. For some firms, tightening from the Fed caused the cost of funding to rise much more rapidly than the yields earned on assets. As those weaknesses became apparent, money fled the balance sheets of poorly-managed companies.

Some observers were convinced that other banks would succumb to the higher-for-longer interest rate environment. But SVB was an extreme case; its gamble that rates would remain low was immense. Most banks controlled their positions much more effectively, and regulators have been reinforcing the need for strong market risk management. Surprises are always possible, but it seems unlikely that we’ll see more failures tied to this root cause.

The second source of weakness for the banking industry is still active. Loans secured by office real estate properties are the subject of heightened concern and scrutiny. As we wrote last fall, we appear to have reached “peak return to office,” leaving acres of space vacant and rents under substantial downward pressure. The challenge of what to do with the unwanted square footage has been the subject of numerous recent examinations.

NYCB has served as a flash point on this issue. Its fourth quarter earnings release included additional provisions for real estate loan losses and a cut to its dividend. (Interestingly, the company had purchased a block of loans from the failed Signature Bank.) The company’s stock lost more than half of its value in just two days. A handful of other firms, some outside of the U.S., also announced charges related to commercial real estate (CRE) lending that led their shares to decline.

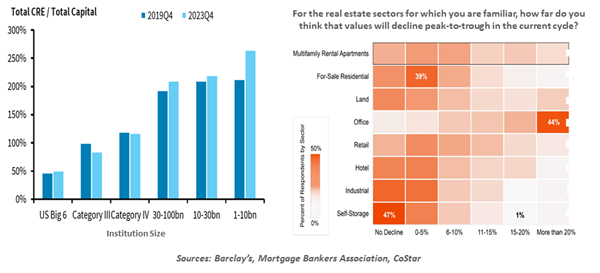

While there are unique aspects to the NYCB story, it has prompted a renewed focus on bank exposure to CRE loans. Financial institutions hold just under 40% of the credit extended to this sector; investors have the remainder. Within the banking industry, CRE loans are more highly concentrated in smaller, more regional firms, which makes them more vulnerable.

AS THE ANNIVERSARY OF SVB’S FAILURE APPROACHES, BANKS ARE FACING RENEWED SCRUTINY.

Some have suggested that systemic problems are imminent. We disagree, and here is why:

- Not all commercial real estate is created equal. Apart from office property, this category includes industrial space, apartment complexes and retail developments. These latter segments are performing relatively well; vacancy rates have been stable, and rents are growing.

- Not all office property is created equal. There is substantial diversion in performance between prime (class A) properties and those that are less modern. There is also substantial diversion between locations and property size; while our imaginations often go straight to towers in city centers, the median office building is only a few floors tall.

According to the real estate firm CBRE, nearly two-thirds of office properties are at least 90% leased. On the other side of things, about 7% are leased at 50% or less of capacity. It is those latter buildings, and those who lent against them, that are experiencing distress. This suggests that problems will be isolated and not industry-wide.

- Commercial real estate loans typically have five year terms, at which point they come up for renewal. That spreads the reckoning out over time, and affords both banks and landlords some opportunity to prepare.

- Banks maintain reserves for loan losses, which are based on quantitative and qualitative assessments. In general, CRE reserves are in line with estimates of changes in value; most firms have been adding to these reserves steadily over the past two years.

For all of these reasons, simple comparisons of commercial real estate loans to a bank’s capital base can be very misleading. While some firms will experience more stress than others, the industry should be well-positioned to deal with the office bust. As this situation is not new, regulators have been pressing firms to perform honest reckonings of their commercial real estate exposure. And if systemic stress resurfaces, the Federal Reserve can draw on the playbook it used last March to restore order.

These mitigating facts may, however, not be enough to head off negative sentiment. Once concern takes root, it is difficult to unearth. Fear of loss and confirmation bias in screening incoming information (among other behavioral tendencies) can make perceptions of the problem much more serious than the problem itself. As was the case last year, it may take time for calm to be restored.

I was hoping to get some help for this article from one of our crack banking analysts. Unfortunately, I couldn’t remember his name to drop him a note. He has three children, though…

EXPOSURE TO COMMERCIAL REAL ESTATE LOANS DOES NOT REPRESENT A BROAD THREAT TO THE BANKING INDUSTRY.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Northern Trust

More Active Management Topics >