Many investors limit their mandates to credits rated BBB or higher. But they could tap high-quality high yield—without adding to overall risk.

A traditional investment-grade multi-sector bond portfolio offers clear attractions: low default risk combined with a modest yield pick-up over Treasuries in a readily understood package. Even so, this approach comes with an opportunity cost. An investment-grade-only portfolio misses out on the benefit of wider diversification, which creates the opportunity to manage risk more efficiently and potentially achieve higher income and better risk-adjusted returns.

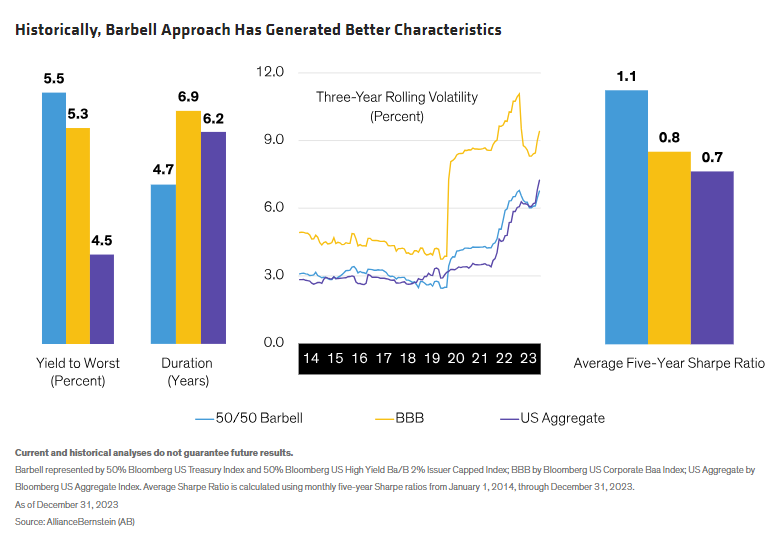

For example, a simple 50/50 passive “barbell” combination of US Treasuries with high-quality (rated BB or B) US high-yield bonds has historically produced better outcomes than both BBB-rated US corporate bonds and the broader US Aggregate Index across a range of metrics. These include higher income, lower volatility, less interest-rate risk (duration), and higher risk-adjusted returns (Display)—features that have characterized the barbell approach over time.

Combining Negatively Correlated Assets

A credit barbell combines interest-rate-sensitive bonds with higher-yielding credit assets because their returns are usually negatively correlated. When riskier, growth-oriented credit assets such as high-yield bonds fall in value, government bonds and other interest-rate-sensitive assets usually rise, and vice versa. Because negatively correlated assets tend to take turns outperforming each other, investors can sell the outperformers on one side (for instance, high-quality high yield) and buy the cheaper bonds on the other (for example, Treasuries). That approach has historically tended to increase returns over time.

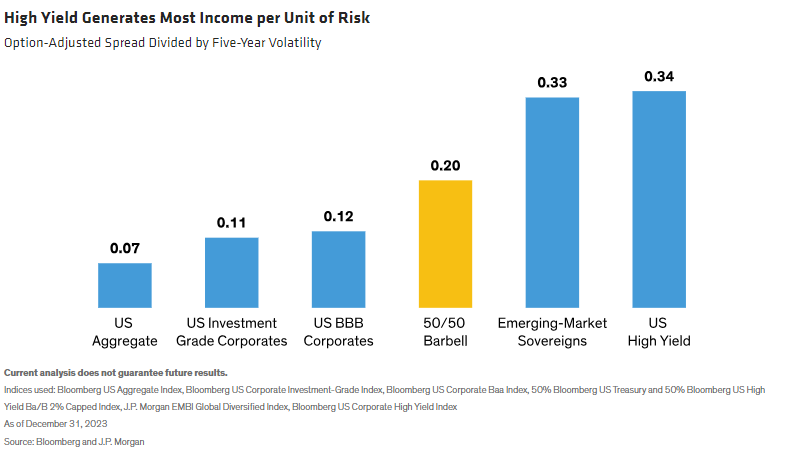

In our 50/50 barbell example, we used US Treasuries to represent interest-rate risk and US high yield as a proxy for credit risk. The investment-grade portfolio underperformed this barbell because it lacked enough exposure to credit risk to generate higher income and returns. Credit risk is typically well compensated with income. Using option-adjusted spread divided by volatility as a measure of income per unit of risk, we can see that US high yield is a very efficient income generator (Display).

The income contribution from high yield is critical. Historically, the biggest component of bond returns has come from income payouts to bondholders rather than capital appreciation. In fact, over the last 20 years, US high-yield bonds’ annual return due to income has slightly exceeded annual total return. Hence, a strategy that is underexposed to income per unit of risk will likely struggle to generate attractive returns for risk-conscious investors.

Getting the Balance Right

What’s the right mix of assets? That depends on each investor’s needs and comfort level. A simple 50/50 split could be right for an investor with high income requirements and a high risk tolerance, because credit assets are at least twice as volatile as high-quality government debt. So when it comes to risk exposure, an even split between the two asset classes effectively tilts toward credit.

An investor who wants a more balanced exposure would likely incline toward a 65% Treasuries / 35% high-yield allocation, giving up a small amount of return in exchange for lower risk. In practice, investors seeking an optimal mix would also likely allocate to a wide variety of higher-yielding fixed-income sectors, including not only high-yield bonds but also corporate and hard-currency emerging-market debt, inflation-linked bonds and securitized assets.

Most important, we believe keeping the right balance involves an active, dynamic approach that explicitly manages the interplay of rate and credit risks. To that end, credit barbells offer an advantage: combining diversifying assets in a single portfolio makes it easier to manage risk and tilt toward duration or credit according to market conditions.

High-Yield Credit Has Structural Advantages

Although spreads have tightened recently, high-yield credit is still attractive, in our view. And it has several structural advantages over investment-grade credit too, beyond its bigger exposure to credit risk.

The high-yield market is relatively small and has tended to benefit as bond issues are promoted to and demoted from investment grade. Rising stars have typically outperformed by approximately 60 basis points in the months before they leave the high-yield index, as the market anticipates their promotion. And once rising stars enter the investment-grade market, high-yield-focused investors have tended to sell and redeploy the proceeds across similar high-yield credits, boosting their price.

Fallen angels also enjoy supportive conditions. Fallen angels tend to be large relative to the average high-yield name and to trade with tighter spreads than the broader index. Investors who benchmark to the high-yield index often need to buy these new and sizeable index constituents to remain aligned with their benchmark.

At the same time, fewer of the investment-grade investors that held these bonds before they fell below investment grade are forced sellers than in the past, when guidelines compelled them to sell upon downgrade; many of these investors now have the flexibility to wait for a recovery in the issuers’ rating.

The high-yield market’s small size has other advantages. Downgraded high-yield bonds can attract strong support from investors that specialize in distressed names, owing to limited supply.

Whereas investment-grade corporate bonds are generally not callable, high-yield issuers can call their bonds—and sometimes do so above the call price stated in the prospectus, generating windfall profits for bondholders. That’s a potentially valuable feature when, as today, bonds are trading at a discount.

Stay High Quality to Mitigate Risk

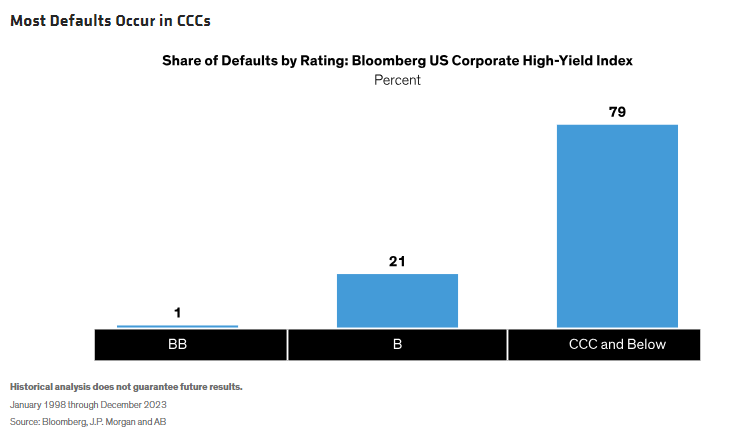

To reduce some credit risk, an investor might cut out low-quality, CCC-rated bonds, the riskiest slice of the high-yield universe. These securities are at the highest risk of default (Display), and steering clear might make sense during the late stages of a credit cycle when economic conditions are tough for corporates. This approach would concede a small amount of return in exchange for significantly lower default risk.

Active Management Can Add Value

There’s no one way to build a well-diversified portfolio. But it’s important to vet potential managers carefully to learn about their investment process and approach to balancing interest-rate and credit risks. Knowing which way to lean—and when—requires a deep understanding of the interest-rate and credit cycles around the world and how they interact.

We think a portfolio that dynamically balances high-quality and high-income bonds has the potential to weather most markets and represents a more efficient approach than a stand-alone investment-grade multi-sector mandate. Investing, like most things in life, is better with balance.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© AllianceBernstein

More Volatility/Downside Protection Topics >