Summary

- In a sea of income investment options, MLPs could be easily overlooked despite generous yields and tailwinds from free cash flow generation.

- Stable cash flows and special tax treatment have allowed MLPs to historically pay generous distributions (dividends).

- Significant changes to capital allocation over the years, free cash flow generation, and a greater focus on sustainable distribution growth can add to investors’ confidence in MLP payouts going forward.

Income investors have an overwhelming number of investment options today. The menu ranges from traditional fixed income to equity investments like REITs to innovative covered call ETFs to more exotic vehicles. Master limited partnerships (MLPs) are known for their potential to provide tax-advantaged income. But they have also generated attractive total returns in recent years. Despite positive fundamentals driven by solid free cash flow generation, MLPs may be overlooked by investors given so many income investment options. This note explains why MLPs are able to provide generous yields and why investors can be confident in MLP payouts going forward.

Understanding MLP Yields

MLPs enjoy special tax treatment by nature of their involvement with natural resources. Though there are other kinds of MLPs, investment products tend to focus on energy infrastructure (or midstream) MLPs. These companies generally transport, store, and process hydrocarbons for fees. While midstream is a subsector of energy, it is unique within energy due to its fee-based business models. Midstream companies generate stable, predictable cash flows, and as such, most companies provide annual EBITDA guidance that is largely independent of commodity prices.

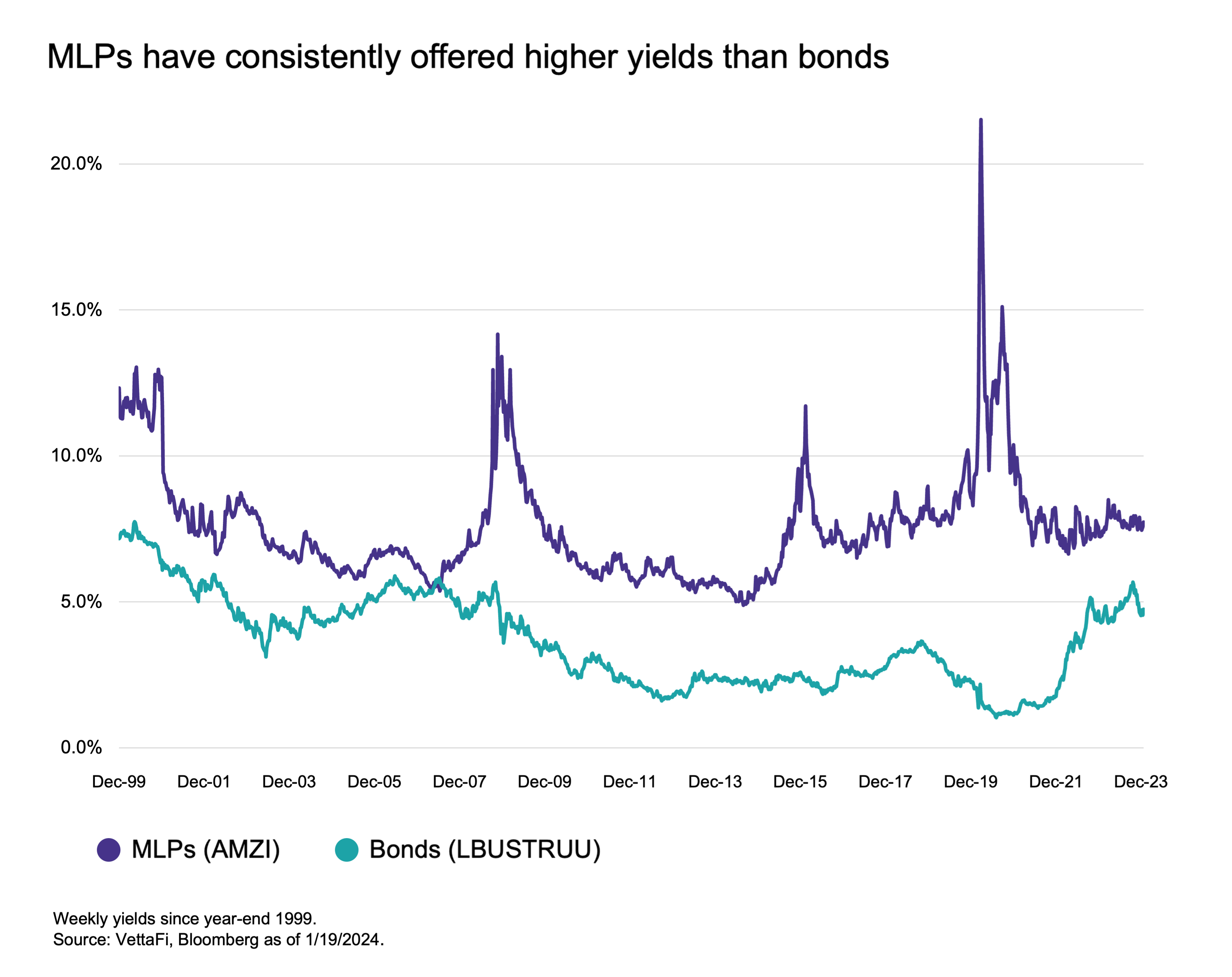

Stable cash flows and special tax treatment have allowed MLPs to historically pay generous distributions. These distributions are often tax-deferred, adding to the appeal of MLPs (read more). The chart below compares the yield for the Alerian MLP Infrastructure Index (AMZI) and the Bloomberg US Aggregate Bond Index (LBUSTRUU). To be clear, MLPs are not a bond substitute. And as equities within the energy sector, MLPs have a different risk profile than corporate bonds. Rather, the corporate bond benchmark is used as a comparison for its familiarity. The chart also highlights the contrasting nature of MLP yields and bond yields, which fluctuate with interest rate levels.

The period since 2000 covers a variety of economic conditions and commodity price environments. The AMZI yield noticeably spiked during the Great Financial Crisis, when oil prices were plummeting in 2015-16 as Saudi Arabia battled U.S. shale for market share, and during the pandemic. These periods coincided with weakness in MLP performance. Admittedly, there were distribution cuts from select MLPs both in 2015-16 and in 2020, with smaller companies generally more likely to experience cuts. The average AMZI yield since 2000 was 7.6%. That is in line with the current index yield of 7.5% as of January 26, 2024.

The lowest yield for AMZI since 2000 was 4.9% in August 2014. That coincided with an all-time high in AMZI. Even with a three-year annualized total return of 31.6% as of January 26, 2024, the AMZI is still 52% below the all-time high from 2014. This isn’t a space that has become expensive (read more). MLP yields remain generous compared to many other income investments. They also provide the potential for tax-deferred income.

How Can Investors Be Confident in MLP Payouts?

A long-term yield chart can be helpful context, but for new investors, the outlook for MLP distributions is arguably more important. There are several reasons investors can feel confident in MLP payouts going forward. These include significant shifts in capital allocation, as well as a broader focus on sustainable distribution growth from lessons learned in the past.

First, companies have largely lowered their leverage ratios and are generating free cash flow. MLPs have stronger balance sheets and more financial flexibility today. Distribution cuts in the past were often a function of hefty growth spending combined with an overreliance on capital markets for financing. Growth spending has moderated significantly from prepandemic levels. And companies are much less dependent on debt and equity markets for funding than they once were.

Additionally, MLPs have a stronger distribution track record today. Approximately 80% of AMZI by weighting has grown its distribution over the last year. Importantly, the last distribution cut from an AMZI constituent was in July 2021. Companies learned their lessons from painful distribution cuts in the past. They are more focused on sustainable distribution growth. A reestablished track record for payouts can add to investor confidence going forward.

Finally, many MLPs have buyback authorizations in place, particularly larger names in the space. By weighting, 70% of AMZI had a buyback authorization in place at the end of 2023. If companies have excess cash flow to pursue opportunistic buybacks, that is a good indication they can afford to maintain or grow their distributions.

Bottom Line:

MLPs provide generous yields while benefiting from the tailwinds afforded by solid free cash flow generation. With a constructive outlook for future payouts, MLPs can help enhance the yield of income portfolios.

For more on using energy infrastructure in income portfolios, including other portfolio benefits like diversification, please join our 30-minute LiveCast on Tuesday, February 6, at 12:30 p.m. ET (register here).

Related Research:

Is Your Income Stream Too Dependent on the Fed?

MLPs and MLP ETFs: Not Just Income, but Tax-Deferred Income

Midstream/MLPs: Free Cash Flow Powerhouse

Midstream/MLPs Raising the Bar with Lower Leverage

Midstream Sees Strong Free Cash Flow Generation in 2023

3Q23 Midstream Dividend Recap: MLPs Bring the Growth

Understanding the Tax Benefits of MLPs

Raymond James Analyst Shares Top Picks, Midstream Investment Opportunities

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB).

Vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMLP and MLPB for which it receives an index licensing fee. However, AMLP and MLPB are not issued, sponsored, endorsed, or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of AMLP and MLPB.

Originally published on ETFTrends.com on January 30, 2024.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Read more commentaries by VettaFi