It is said that if someone had only a limited time to live, they should spend it with an economist; the experience would seem like an eternity. We are not known as the most vivacious people.

It will therefore come as no surprise that economists are anxious for holiday celebrations to end. The American Economic Association (AEA) holds its annual meeting right after new year’s, and the event draws thousands. Many of the sessions are of somewhat academic interest, but a handful are more mainstream.

Such was the case last week, when Lorie Logan, the President of the Federal Reserve Bank of Dallas, offered her thoughts on monetary policy at the AEA meeting in San Antonio. There has been a lot said and written about how central banks might manage interest rates in 2024, but relatively little has been offered on how they might steer their balance sheets. Logan ventured into the latter territory, offering a potential roadmap for the year ahead.

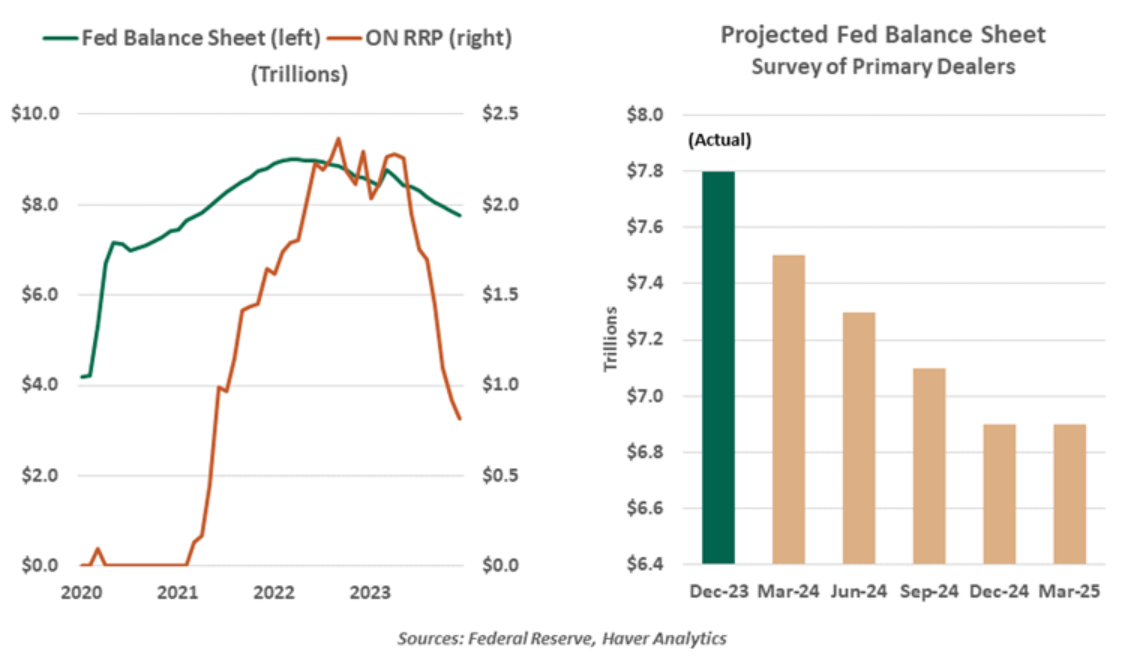

As background, the Fed (among other central banks) built its investment portfolio amid the crises of 2008 and 2020. The process, known as quantitative easing (QE), was designed to continue providing stimulus when overnight interest rates were at zero. The Fed’s balance sheet went from about $900 billion in early 2008 to $4.5 trillion in 2015 and nearly $9 trillion in early 2022.

The Fed has been reducing its portfolio for nearly two years now, to tighten financial conditions. (Hence the term “quantitative tightening,” or QT.) Holdings have fallen by more than $1 trillion. Excess liquidity invested in the Fed’s overnight reverse repurchase program (ON RRP) has dropped from well over $2 trillion to less than $700 billion.

There is no set level or formula for how large a central bank’s balance sheet should be. The size of its underlying economy, the demand for reserves from the banking system and the depth of its local markets are all important considerations. And while we have decades of history to study how interest rates affect economic activity, the Fed’s QE program is only fifteen years old. (And several of those fifteen years were consumed by crisis.) So central banks have little to guide strategy on this front.

As we discussed last year, the Fed’s first attempt at QT in 2019 ended prematurely. Reserves in the financial system became thin, challenging the liquidity of certain markets. The program concluded far earlier than anticipated and created a minor dent in the Fed’s credibility. One take away from that experience was the need to provide early guidance on when balance sheet management efforts were near an end.

Fed officials are discussing when and how to stabilize their balance sheet.

Logan, who managed the Fed’s investments before moving to Dallas, is especially well placed to begin providing that perspective. In her remarks to the AEA meeting, Logan hinted that QT may be in its final stages, saying “(W)e should slow the pace of runoff as ON RRP balances approach a low level.”

Exactly what a “low level” of balances is will be the subject of considerable discussion. John Williams, the President of the Federal Reserve Bank of New York, said later last week that “we don’t seem close to that point.” Nonetheless, the fact that the topic is being discussed by Fed officials publicly and privately suggests that the Fed’s balance sheet could stabilize within the next twelve months.

The Treasury markets will be watching developments closely, as the tapering of the Fed’s holdings requires other investors to step forward. Having a sense of what the Fed’s long-term demand looks like may help reduce volatility in fixed income markets.

To the layperson, this somewhat wonky discussion may not seem overly exciting. But to economists, it really got the new year off to roaring start.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Northern Trust

Read more commentaries by Northern Trust