In this week’s edition of “Three on Thursday,” we take a deeper look at the employment landscape in the United States. Every month, usually on the first Friday, the Bureau of Labor Statistics reports jobs data. This data comes from two surveys of establishments and households. Using a representative sample of 122,000 entities (private and public), the Establishment survey is best known for providing the monthly change in nonfarm payroll employment. Beyond this, it also captures data on earnings and hours worked. Alternatively, the Household survey samples roughly 60,000 eligible U.S. households. It is best known for measuring the national unemployment rate, but also looks at the labor force, and employment with demographic detail. Much can be gleaned from both reports, and over time the employment components tend to track each other closely. The employment sector has undergone a tumultuous journey over the past four years, and recently the trajectory of job gains has experienced a gradual deceleration over the past year, prompting speculation about the future. To offer deeper insights, we’ve included three informative charts below.

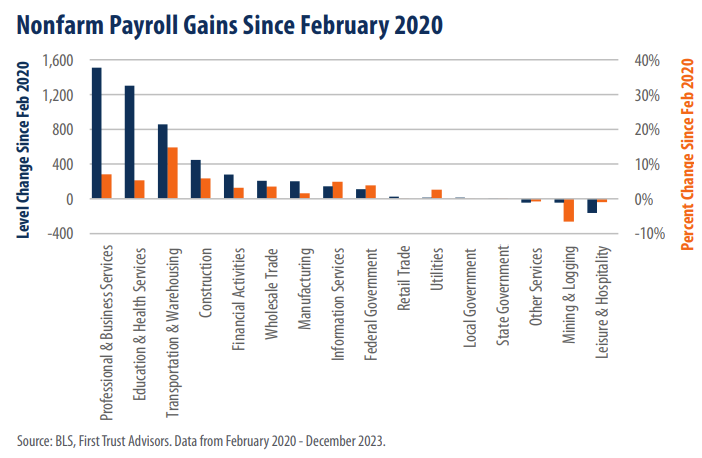

During the COVID-19 shutdowns in March and April 2020, the Establishment survey showed a loss of 21.9 million jobs. Since the bottom in April of 2020, payrolls have rebounded by 26.8 million, resulting in a net increase of 4.9 million jobs since February 2020. While the overall job market has shown improvement, three sectors—Other Services, Mining & Logging, and Leisure & Hospitality—have yet to fully recover. During this period, Professional & Business Services, as well as Education & Health Services, have emerged as standout performers, accounting for 2.8 million of the 4.9 million net job gains. On the surface these look like big numbers, but monthly gains have averaged just 106,000 since February 2020.

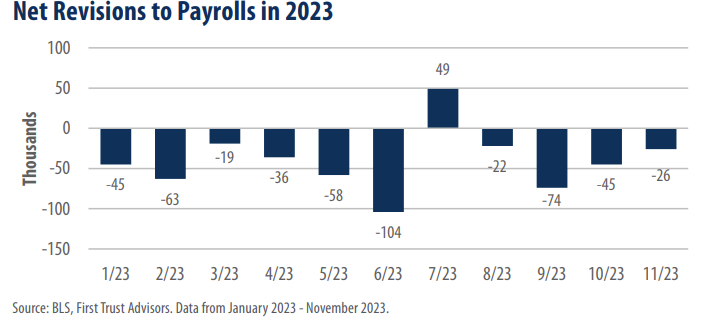

Within the Employment Situation report every month, the Establishment survey provides a current estimate of the monthly change in nonfarm payrolls, along with revisions to prior months. So far in 2023, from January to November (the latest month with a revision), downward revisions have occurred 10 out of the 11 months—a trend observed only a few times in history, notably in 2008 and 2009. Nonfarm payrolls experienced downward revisions totaling 427,000 jobs. We view this as a sign that the labor market is weakening, however it may not persist.