Private credit has in a little more than a decade evolved from a niche asset class to a key component of a diversified investment portfolio. We think it will be even more important in 2024 as banks’ reluctance to lend widens the opportunity set for investors.

A potential slowdown in economic growth may put pressure on some borrowers this year, making manager skill in proactively managing and navigating credit risk across a portfolio a key focus. At the same time, with US inflation likely at or near the peak and prices in the eurozone heading back toward target, we expect to see increases in capital-market activity and private transaction volume.

In short, the year ahead has the potential to be a rewarding one for those invested in private credit. Opportunities span the risk-return spectrum across private credit asset classes, including corporate lending, commercial real estate, energy transition and consumer finance. And investor allocations are increasing. According to Preqin, a data provider, total assets have nearly doubled since 2020 to $1.6 trillion and are expected to swell to $2.3 trillion by 2027.

The question investors are likely to be asking in 2024 isn’t whether to increase exposure to private credit. It’s how.

Banks on the Backfoot

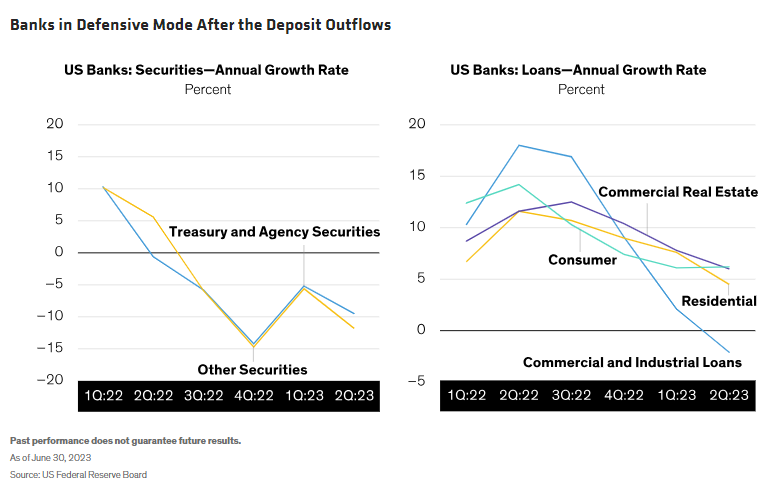

The way we see it, investors will have multiple trails to tread. Banks sharply reduced lending last year as they shed deposits and took mark-to-market losses on assets as interest rates soared (Display). More than $1 trillion of household deposits have left the US banking system since interest rates started their rapid rise in 2022, adding momentum to the trend of bank retrenchment that began after the global financial crisis.

Banks will soon have to comply with updated global Basel III regulations, which come into effect in 2025 and will include a rewrite of the risk-weighted asset framework. We expect this to force many to reduce lending further and shed some of the loans—residential, commercial and corporate—already on their balance sheets.

Put another way: some banks today want to be in the moving business, not the storage business. That will create opportunities for private lenders to partner with banks across market areas and geographies in 2024 and beyond.

For example, private lenders may benefit from the sourcing of attractive investment opportunities, such as purchasing pools of loans from banks at a discount or entering into risk-sharing agreements to acquire newly originated ones that meet pre-determined credit requirements.

Banks, meanwhile, would benefit from maintaining loan origination and the associated fees without incurring the high regulatory capital charges that would come with keeping these loans on their books.

A Rockier Road

The macro backdrop next year may create some challenges. Key central bank interest rates are likely to remain high compared to the past 15 years. But signs of slower growth in the US and Europe suggest markets could see rate cuts before year end. We expect a soft landing—but a landing, nonetheless.

That’s important, because even a gentle turn in the credit cycle can increase stress for some borrowers. This is likely to shine a spotlight on managers’ ability to underwrite, structure and price credit risk effectively, and it will favor those with a track record of operating across asset classes and economic cycles.

On the other hand, it’s important to remember that private credit transactions are directly originated, negotiated and structured (including borrower convents). These transactions also involve regular communication among lenders, borrowers and, in the case of direct lending, private equity sponsors. This makes it easier to proactively engage with borrowers and work around potential problems.

Filling the Gap

So where should investors set their sights as the new year gets underway? We think there are several areas that deserve attention. But 2024 may turn out to be the year in which asset-backed lending strategies—also known as “specialty finance”—start to take up more space in private asset allocations.

Specialty finance encompasses niche strategies that involve non-bank lending against pools of cash-flowing assets or receivables—often consumer- or small-business-related—such as auto and equipment loans or esoteric assets such as the revenue streams generated by royalty payments.

We think these types of strategies have the potential to generate strong return potential while diversifying portfolios and vastly broadening the private investment universe, much the way direct lending did in the years after the global financial crisis.

Don’t Neglect Direct Lending

Direct lending fueled the growth of private credit after the global financial crisis and will remain the bedrock of private asset allocations. As 2024 gets underway, direct lending represents the largest share of the US private corporate credit market and offers attractive incremental yield over public corporate credit.

What’s more, direct lending can play an important role in bull and bear markets. We think a focus on companies with strong revenue profiles and diversified customer bases has the potential to deliver attractive risk-adjusted returns in any market environment. Deals today typically come with important structural protections, including large equity cushions. In the new year, we think investors may benefit from investing alongside disciplined managers with experience investing in a variety of market conditions.

Turning a Corner?

Activity in the commercial real estate market was restrained in 2023. But signs that interest rates in the US and Europe may have peaked suggest that could change. We expect greater rate stability to result in higher transaction volumes and increased price discovery across property types.

A wave of maturing loans held by banks who may be reluctant to extend them could create opportunities for private lenders who have remained patient and well-capitalized. As always, the risk-reward calculus varies by property type.

The Global Energy Transition

We expect private lenders to continue to drive financing for renewable energy projects in the year ahead, and we see a number of attractive opportunities as 2024 gets underway. Many stem from the repricing of long-dated public and private infrastructure assets—the result of sharp rate spikes in the third quarter of 2023.

For investors who can take a highly opportunistic approach, the current market backdrop looks appealing. Developer demand for capital remains robust and stress in the banking sector means negotiating leverage has shifted to private capital providers, who can demand credit enhancements and other protective provisions. We see opportunities across the US and European markets.

Putting Capital to Work

Even if the pace of economic growth slows, yields are likely to remain above pre-pandemic-era lows. And we expect deal terms across asset classes to remain favorable, with low loan-to-value ratios and attractive asset values that were reset over the last 18 months as rates rose. In our view, 2024 will be a good time to put capital to work.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein