State revenue trends in focus: While headlines may turn negative, municipal credit conditions remain strong

In recent months, state and local government tax collections have fallen from the exceptionally high and unsustainable levels in fiscal years 2021 and 2022. Total state and local revenue declined 7% in the third quarter from the same quarter last year; however, the overall backdrop remains healthy when put in context.Footnote1 State governments’ fiscal year 2024 budgeted personal income tax collections remain approximately 25% above pre-pandemic levels,Footnote2 sales tax revenues remain relatively stable, property tax trends remain positive, and state and local governments remain flush with accumulated reserves.Footnote3 We expect to see an increase in negative headlines over the coming months as state governments report softer collections relative to prior years – potentially with some falling short of 2024 budget assumptions – but this is likely indicative of a return to a more healthy and sustainable trajectory as opposed to a harbinger of growing credit weakness.

Recent data from California highlights the headline-grabbing revenue declines: California’s October general fund tax receipts missed budget expectations by -31%, with personal income tax (PIT) receipts down -$20 billion relative to budget estimates.Footnote4 This shortfall likely reflects both the shifting revenue environment and the last-minute, one-month extension of the income tax filing deadline. If the October cash report is an early indicator of economic headwinds and a sizeable upcoming budget deficit, we feel California is well-positioned to manage the downturn. Unlike during the global financial crisis, the state is not dealing with a liquidity crisis or governance constraints. Rather, this is a budgetary challenge for which the state has been preparing: California maintains solid reserves and liquidity, and is already operating under a scaled back fiscal year 2024 budget. We would expect the state to respond to an upcoming deficit with austerity measures and use of reserves.

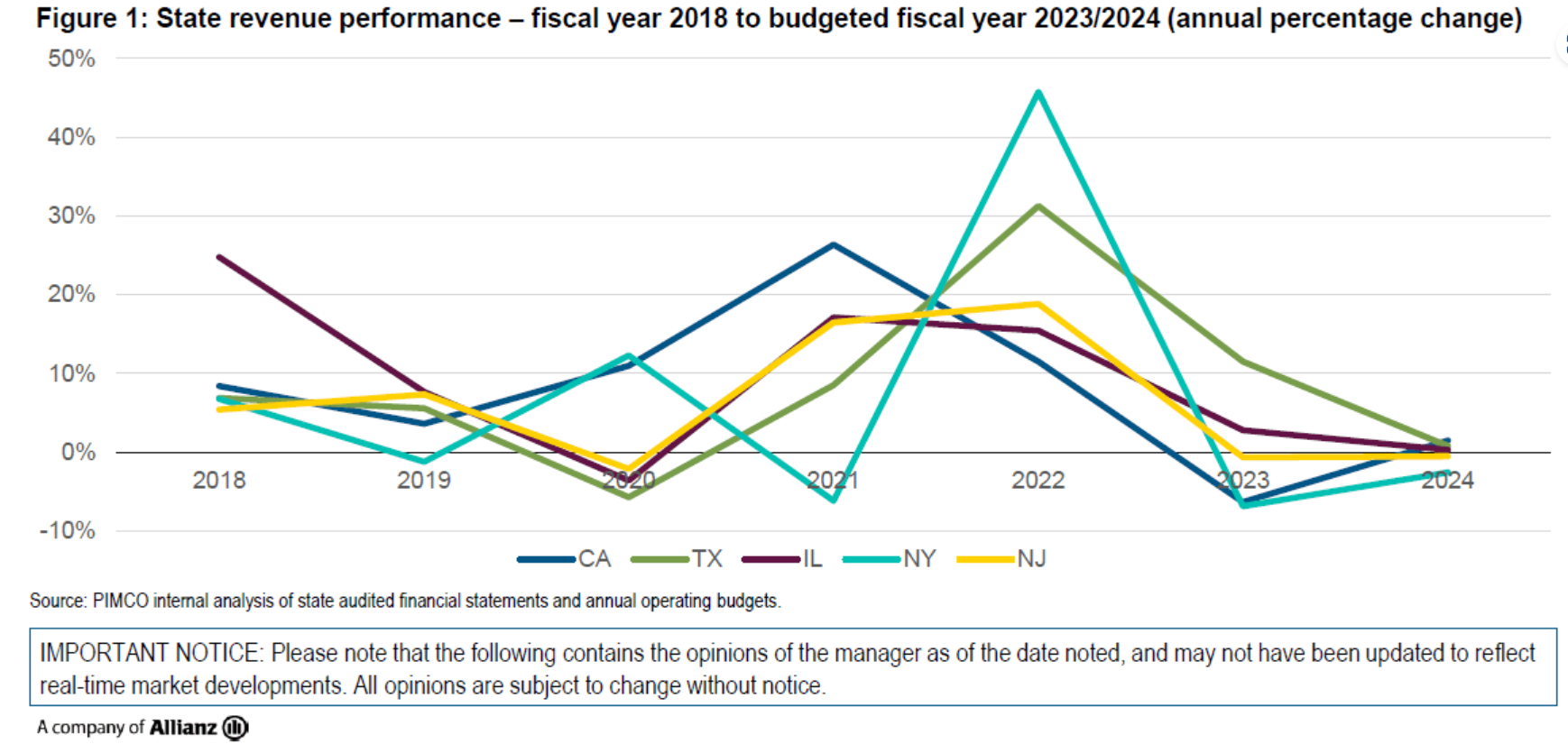

While California was early to make fairly sweeping spending cuts in its 2024 budget, we would note that most large states have dialed back revenue growth estimates considerably for fiscal years 2023 and 2024. Figure 1 illustrates this, specifically showing how a number of states (e.g., Connecticut, New York, and New Jersey) passed budgets that assumed revenue declines and expectations of relatively flat growth in 2024. This is a major positive, as states did not create spending plans for the current fiscal year under the expectation of ongoing robust revenue growth; rather, they were already approaching coming budget cycles with caution. We expect this will make any coming adjustments due to revenue underperformance far easier than if budgets had assumed ongoing revenue growth.

On a broad level, we believe municipal credit conditions remain exceptionally strong. Notably, the median state rainy day fund currently sits at 12% of expenditures versus a median of 4% from 2000 to 2018.Footnote5 Likewise, many local governments are sitting on historically high levels of reserves augmented by remaining federal aid funds that will be spent down through 2026. As negative headlines roll in, it is important to view data in a historical context. We will continue to provide our investors with updates on the municipal credit landscape as it unfolds.

November month in review

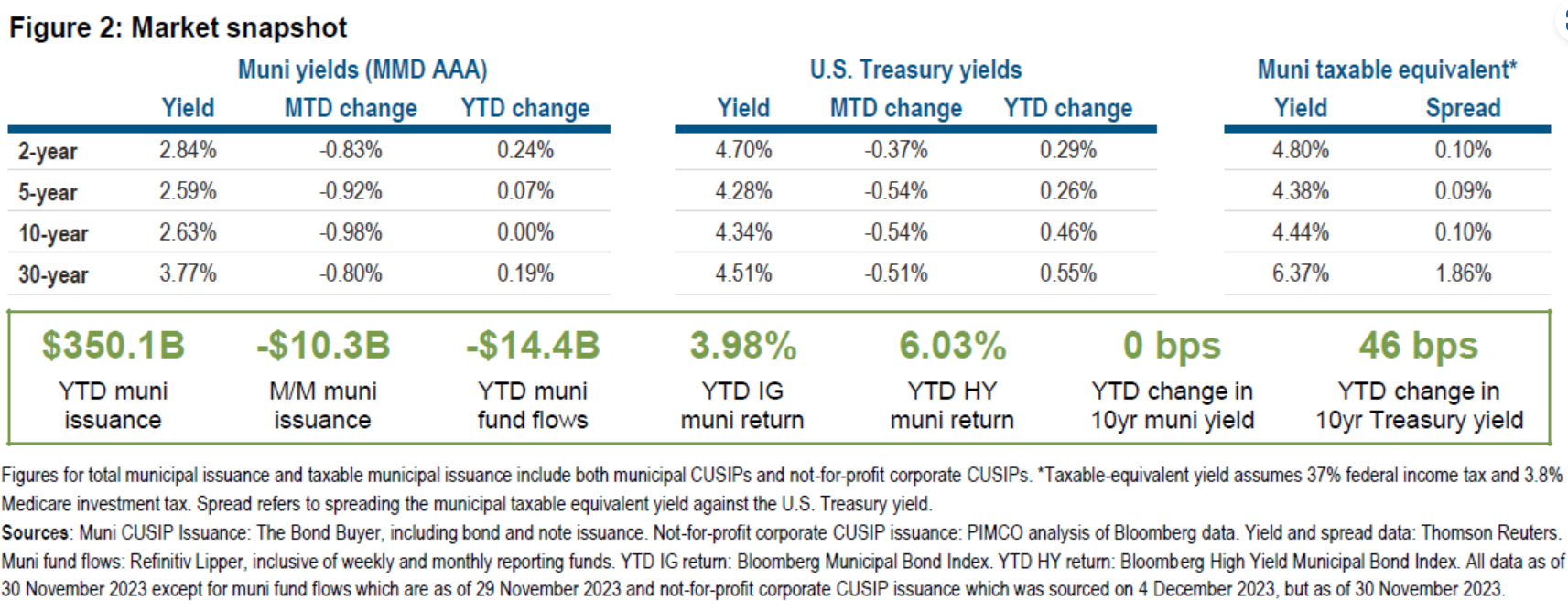

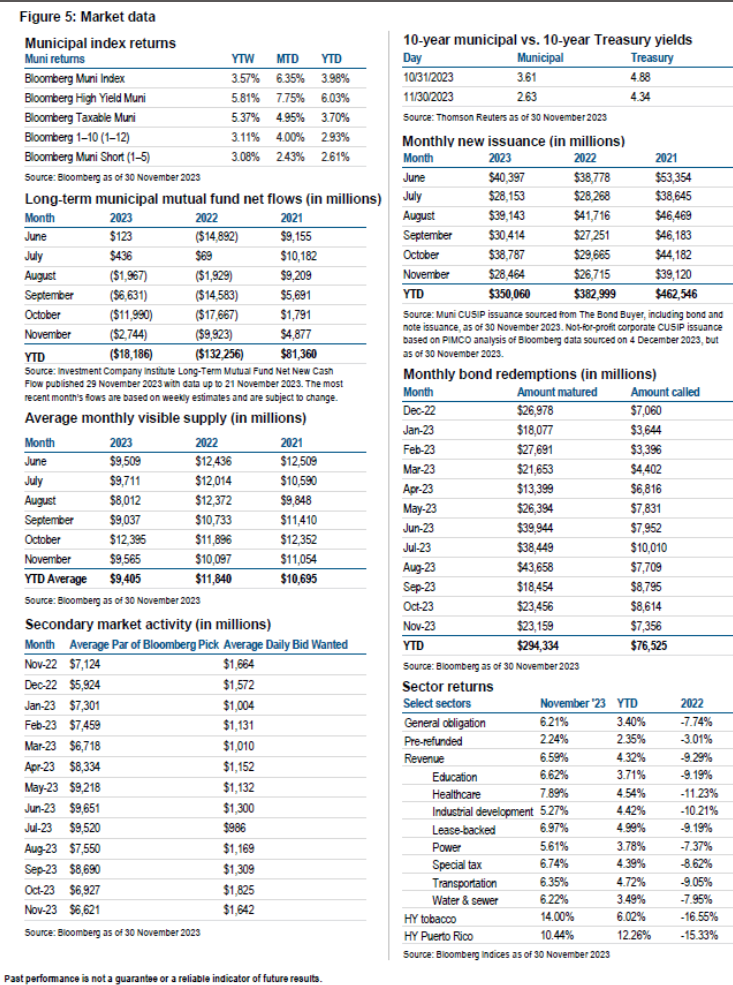

Municipal bond performance in November was the strongest of the year to date. The Bloomberg Municipal Bond Index gained 6.35% (3.98% YTD), while the Bloomberg High Yield Municipal Bond Index increased by 7.75% (6.03% YTD), and the Bloomberg Taxable Municipal Index returned 4.95% (3.70% YTD).Footnote6 The most significant gains came at the long end of the curve. Notably, state and local government debt gained more than 5%, the highest figure since January 1986.Footnote7This robust performance in November turned year-to-date returns in the municipal market positive, highlighting a strong rebound from three consecutive months of negative returns.

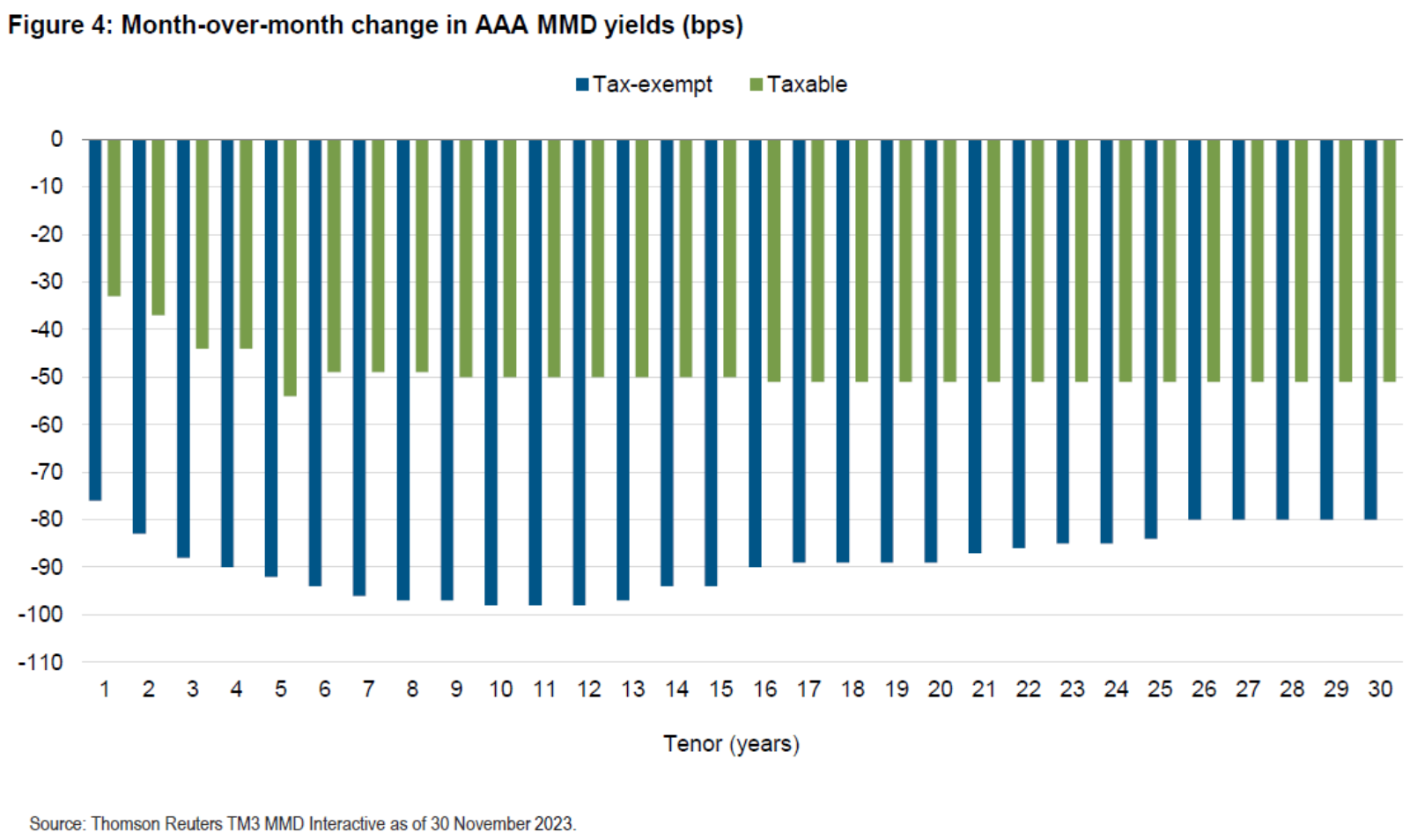

As municipals rallied in November, yields dropped across the curve. The 1-, 5-, 10-, and 30-year tenors of the AAA Municipal Market Data (MMD) curve closed the month at 3.00% (-76 bps), 2.59% (-92 bps), 2.63% (-98 bps), and 3.77% (-80 bps), respectively.Footnote8 U.S. Treasury yields similarly fell in November, but at a more modest rate. Yields dropped at all tenors of the Treasury curve, with the 1-, 5-, 10-, and 30-year tenors ending the month at 5.14% (-32 bps), 4.28% (-54 bps), 4.34% (-54 bps), and 4.51% (-51bps), respectively.Footnote9 Performance wise, the Bloomberg U.S. Treasury Index gained 3.47% (0.67% YTD).

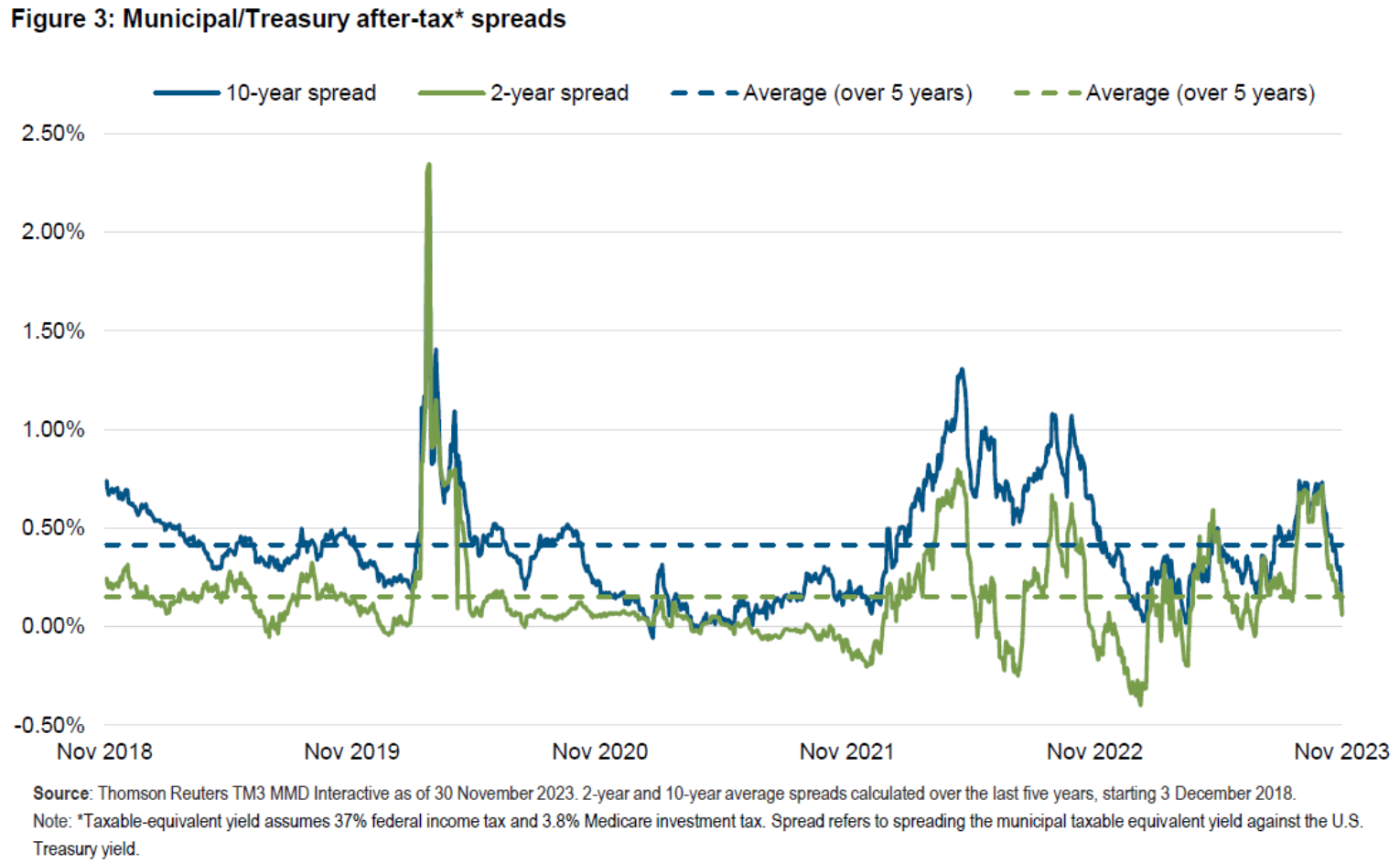

As a result of rate movements, municipal/Treasury ratios richened significantly in November. At month-end, ratios at the 1-, 5-, 10-, and 30-year tenors of the curves were 58%, 61%, 61%, and 84%, respectively, compared to October’s month-end figures of 69%, 73%, 74%, and 91%.Footnote10

Over the first 11 months of 2023, states and localities sold $329.9 billion of long-term municipal bonds, a slight decrease of 2.8% compared to the same time frame of 2022.Footnote11 The small decline was encouraging considering the significant slowdown in overall issuance this year. Notably, the market has seen 28 deals this year exceeding $1 billion, surpassing last year's total of 24 and the previous record of 26 set in 2020.Footnote12 November concluded with total new issuance of $28 billion, down $10 billion from October’s figure but exceeding November 2022’s figure of $26 billion.Footnote13

November also saw municipal bond trading reach an all-time high of 1.5 million trades, as reported by MSRB, driven by a surge in demand from individual investors. Despite the historically high trading activity, outflows from municipal bond funds continued, bringing the year-to-date total to $18.2 billion.Footnote14 Regardless of fund outflows, we expect ETFs to continue to grow. As experienced last year, tax loss harvesting could drive significant ETF inflows in December.

1 US Census Bureau, 2023 Quarterly Summary of State & Local Tax Revenue TablesReturn to content↩

2 NASBO, Fiscal Survey of States, Spring 2023Return to content↩

3 US Census Bureau, 2023 Quarterly Summary of State & Local Tax Revenue TablesReturn to content↩

4 California Office of the Controller, October 2023 Statement of General Fund Cash Receipts and DisbursementsReturn to content↩

5 NASBO, Fiscal Survey of States, Spring 2023Return to content↩

6 Bloomberg, 30 Nov 2023Return to content↩

7 Bloomberg, “Municipal Market Brief: Story Bonds Are Back; Rally Rolls,” 30 Nov 2023Return to content↩

8 Thomson Reuters TM3 MMD Interactive Data, 30 Nov 2023Return to content↩

9 Ibid Return to content↩

10 Ibid Return to content↩

11 Bloomberg, “Municipal Market Brief: Political Fodder; Fed Proceeds Carefully,” 22 Nov 2023Return to content↩

12 Bloomberg, “Municipal Market Brief: Deals by the Billion; Charter Bundle,” 29 Nov 2023Return to content↩

13 The Bond Buyer: Primary Market Statistics – A Decade of Bond Finance, 30 Nov 2023; Bloomberg Corporate Issued Municipals Data, 30 Nov 2023Return to content↩

14 Refinitiv Lipper US Flow, J.P. Morgan, 4 Dec 2023. Note: combined weekly and monthly flowsReturn to content↩

DISCLOSURES

Past performance is not a guarantee or a reliable indicator of future results.

Investing in municipal bonds involves the risks of investing in debt securities generally and certain other risks. Investors will, at times, incur a tax liability. Income from municipal bonds is exempt from federal income tax and may be subject to state and local taxes and at times the alternative minimum tax. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increases this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed.

The credit quality of a particular security or group of securities does not ensure the stability or safety of an overall portfolio. The quality ratings of individual issues/issuers are provided to indicate the credit-worthiness of such issues/issuer and generally range from AAA, Aaa, or AAA (highest) to D, C, or D (lowest) for S&P, Moody’s, and Fitch respectively.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

PIMCO does not provide legal or tax advice. Please consult your tax and/or legal counsel for specific tax or legal questions and concerns.

Charts are provided for illustrative purposes and are not indicative of the past or future performance of any PIMCO product.

Bloomberg Municipal Bond Index consists of a broad selection of investment-grade general obligation and revenue bonds of maturities ranging from one year to 30 years. It is an unmanaged index representative of the tax-exempt bond market. The index is made up of all investment grade municipal bonds issued after 12/31/90 having a remaining maturity of at least one year. The Bloomberg High Yield Municipal Bond Index measures the non-investment grade and non-rated U.S. tax-exempt bond market. It is an unmanaged index made up of dollar-denominated, fixed-rate municipal securities that are rated Ba1/BB+/BB+ or below or non-rated and that meet specified maturity, liquidity, and quality requirements. The Bloomberg Taxable Municipal Index represents a rules-based, market-value weighted index engineered for the long-term taxable bond market. For inclusion in the Index, bonds must be rated investment grade quality or better, have at least one year to maturity, have a coupon that is fixed rate, have an outstanding par value of at least $7 million, and be issued as part of a transaction of at least $75 million. The Intermediate Municipal subsector groups together securities with an average maturity between one to 10 years. The Bloomberg 1-10 Year Municipal Bond Index is an unmanaged index considered to be generally representative of investment-grade municipal issues having remaining maturities from 1-10 years and a national scope. The Bloomberg Muni Short (1-5) Index is the Muni Short (1-5) component of the Bloomberg Municipal Bond Index. The Bloomberg U.S. Treasury Index is a measure of the public obligations of the U.S. Treasury. Bloomberg U.S. Aggregate Index represents securities that are SEC-registered, taxable, and dollar denominated. The index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities. These major sectors are subdivided into more specific indices that are calculated and reported on a regular basis. It is not possible to invest directly in an unmanaged index.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world. ©2023, PIMCO.

CMR2023-1211-3275607

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© PIMCO

More Exchange-Traded Products Topics >