This week’s edition of “Three on Thursday” digs a little deeper into the S&P 500 Index. Widely regarded as a barometer for the overall stock market, the S&P 500 Index tracks the performance of 500 of the largest companies listed on U.S. stock exchanges. The S&P 500 Index adopts a market-cap weighting approach, allocating a higher percentage of the index to companies with larger market capitalizations, adjusting for the number of shares available to trade publicly. Year-to-Date (YTD) through December 5, 2023, the S&P 500 Index has delivered a total return of 20.8%. Serving as a benchmark for the broader stock market, many investors find themselves disappointed as their portfolios have not experienced comparable growth this year, falling short of the 20% mark. To unravel the reason behind this disparity, along with other valuation metrics, we present three informative charts below.

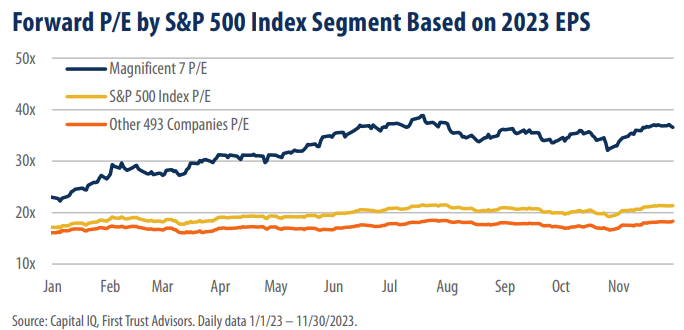

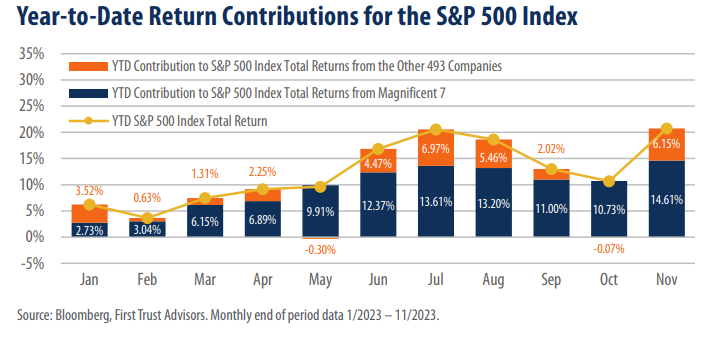

If you’ve adhered to the advice of financial experts (and we believe you should) and built a highly diversified portfolio, this year may have seen your performance lagging behind the S&P 500 Index. The reason lies in the dominance of the so-called “Magnificent 7” companies—Apple, Nvidia, Microsoft, Amazon, Tesla, Alphabet, and Meta. Astonishingly, these seven giants – which currently boast a combined 28.6% weighting in the S&P 500 Index – have contributed to most of the returns in the market this year. As of the end of October, the S&P 500 Index showed a 10.66% increase for the year, with the Magnificent 7 accounting for more than 100% of this total return. This implies that the collective performance of the remaining 493 companies was negative for the year. Then in November, the S&P 500 Index surged 9.1%. Even though the Magnificent 7 rose in November, gains were much more widespread. Consequently, the Magnificent 7 contribution YTD through November to the overall S&P 500 Index has dropped to 70.4% from over 100% in October.

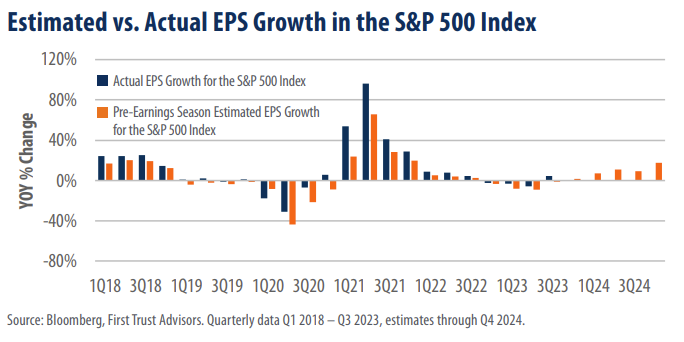

The third quarter earnings season is concluding, with 491 out of 500 companies in the S&P 500 Index having reported for Q3, representing 98.6% of the total market capitalization. Impressively, 81.5% of these companies exceeded expectations, surprising to the upside. Notably, earnings per share (EPS) in Q3 are up 4.5% versus a year ago. Pre-earnings season expectations estimated a 1.2% year-over-year (YOY) decline. Significantly, this quarter marks a noteworthy reversal, representing the first positive quarter after three consecutive down quarters. Earnings are still down for the year, but the consensus outlook sees this as behind us and expects earnings to rise in 2024.