2024 Global Outlook: The Big Picture

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsOur outlook for 2024 is for a gradual U-shaped recovery composed of seemingly chaotic movements in economic data with turning points in policy rates and earnings growth.

Although we're accustomed to defining investment environments in calendar years, 2024 may not fit that approach very well. We expect that there may be a turning point in policy rates and earnings growth, but they may not be easy to identify in real time. Investors may have to step back a bit to see the bigger picture and look beyond the noise and volatility.

A scene in the movie Ferris Bueller's Day Off features Ferris' best friend Cameron focusing more and more closely at a child in one of Seurat's paintings, until he just sees dots and loses perspective. Director John Hughes said of Cameron and the painting, ''the closer he looks at the child, the less he sees,'' as the face disintegrates into a chaotic jumble of pointillist dots. Often the closer we get to something, the more complicated, noisy, and chaotic it seems. Focusing too closely or too near-term on specific developments in the economy, markets, or politics in 2024 can risk missing the bigger picture and broader trend.

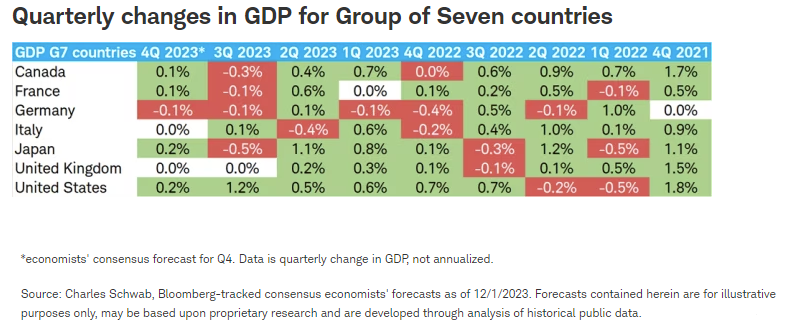

The big picture we see for 2024 is of a shallow U-shaped recovery in global economic and earnings growth, rather than the V-shape seen in the last two global recessions of 2008-09 and 2020. If in 2023 the global economy experienced a soft landing with growth for much of the Group of Seven countries (Canada, France, Germany, Italy, Japan, United States, and United Kingdom) stalling but not contracting much, then it's also likely that a soft recovery gets slowly underway during 2024, with growth rebounding only modestly (and unevenly) throughout the year. Global stocks may react with heightened volatility to the seemingly chaotic data points as parts of the global economy move in different directions, with a broader stabilization and recovery only visible over time. Patient investors in global stocks with an eye on the big picture may benefit despite an uneven path higher should markets discount better growth ahead supported by rate cuts among major central banks.

Cardboard box recovery

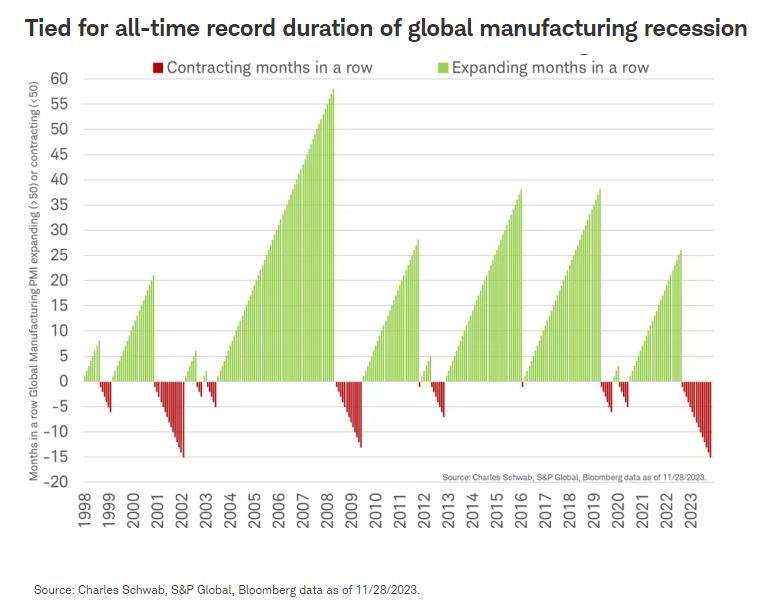

The 2023 global "cardboard box" recession, the downturn concentrated in manufacturing and trade (things that tend to go in a cardboard box), was evidenced in falling factory output, trade volumes and even demand for corrugated fiberboard (what most cardboard boxes are made out of). In particular, the November reading for the Global manufacturing purchasing managers' index (PMI) marked the 15th month in a row below the 50 level that divides growth from contraction. This is the longest such stretch in history, tied with the downturn that ended over two decades ago in 2002. While this downturn is nowhere near as deep as most of the past manufacturing downturns, its extended duration is unique, marking a recession in duration, if not in depth. Declining new orders indicate production weakness likely continues into the early months of 2024 before firming as inventories are drawn down and demand stabilizes.

Economies more exposed to manufacturing and trade have been among the weakest, such as the German economy, which has likely contracted in three of 2023's four quarters. Economies that are more services-focused, like France and the United States, have fared better.

A modest "cardboard box" recovery for 2024 may see a reversal in relative growth. Manufacturing economies may begin to improve while more service-based economies slow. The global services PMI edged down 0.3 points to 50.4 in October. While the latest reading still indicates modest growth, it's come down steadily from the peak of 55.3 in April and the share of economies where the services economy was expanding fell to 57%.

The 2024 forecasts from the OECD (Organization for Economic Cooperation and Development) published last week reflect these reversing trends. Germany's GDP is expected to accelerate out of recession in 2024 while growth in France and the U.S. is expected to slow. The different trajectories of the manufacturing and services sectors adds to the noise in the individual data points we might see in 2024, making the big picture a challenge for investors to discern.

The biggest economy outside of the G7, China, is also likely to struggle with growth in 2024. China has announced accelerated infrastructure spending and the fiscal deficit was raised to 3.8% from 3.0%, a rare intra-year move, likely indicating a sense of urgency and to provide a floor from which the stabilization can build. However, the recovery is likely to be uneven, and investors may need to get used to slower growth from China due to its weak property market, the past buildup of debt, and the size of its economy. More on our outlook for China can be found in our recent article: Is China Investable?

Weaker job market

The labor market may also contribute to the noise in the data points for 2024. While the weakest sector of the global economy, manufacturing, may show signs of improvement in 2024, the strength in the labor market is likely to weaken. Long and variable lags in how rate hikes impact the global economy mean difficult economic conditions may persist in some areas well into 2024, even if rate hikes ended in 2023. There is a clear and intuitive relationship between borrowing costs and job growth. The length of the lag between higher costs and weaker demand for workers is variable, and likely to be felt during 2024.

A weakening of the labor market in 2024 is implied by the chart of the manufacturing employment PMI, which leads job growth in Europe (see the chart below). Further evidence that the labor market is cooling can be seen in Germany's unemployment. It has risen for the 10th month in a row in November, pushing the German unemployment rate up to 5.9%, nearly a full percentage point above its post-pandemic low of 5.0%. We have observed at least one month of job losses in most of the G7 economies, including the U.K., Germany, Canada, Italy, and Japan. France reports employment quarterly and saw a 0.1% gain in employment in the third quarter but could be on the cusp of reporting weaker employment as well.

Relief from inflation

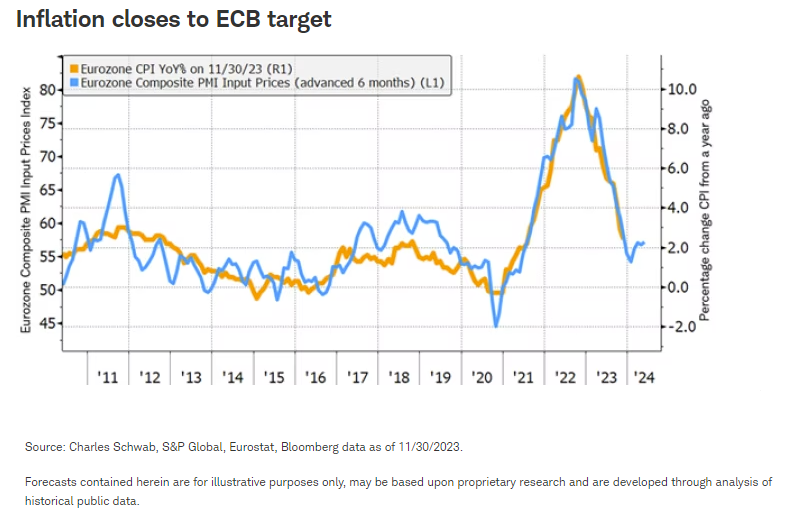

A sluggish European economy has helped inflation recede to 2.4% in November, down from 10% a year ago and very close to the European Central Bank's (ECB) target of 2%. The prior decline in input prices in manufacturing PMIs suggests the consumer price index (CPI) could stabilize around 2% in Europe over the next six months. The PMI input price index has provided a near perfect six-month leading indicator of the trend and level in inflation, which is the blue line you can see in the chart below leading inflation in orange by six months. This decline, coupled with a stagnant economy in Europe, likely opens the door for cuts in 2024.

Lagged impact

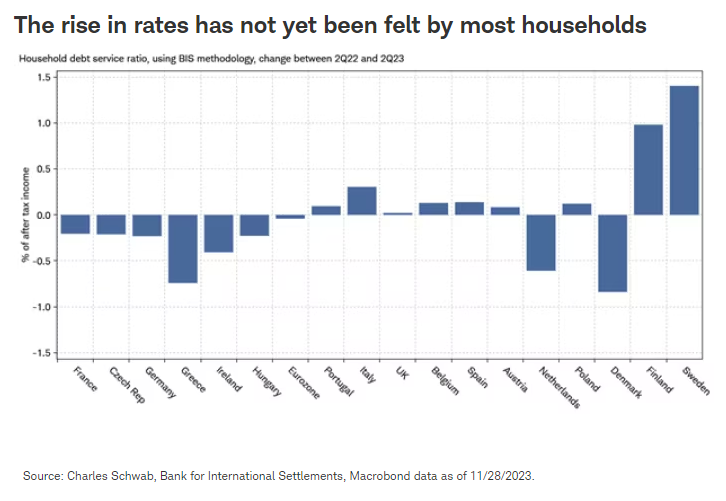

We believe that much of the impact of 2023's rate hikes has yet to be felt. The rise in interest rates in Europe, as the European Central Bank's hiking its policy rate 450 basis points from zero between July 2022 and September 2023 has not tightened European household budgets. The chart below shows the change in interest on debt as a share of income after taxes for households over the period just before rate hikes began at the end of the second quarter of 2022 through the end of the second quarter of 2023. The share of income going to interest payments has barely moved, falling for the eurozone overall, with exceptions in Finland and Sweden where 50% or more of mortgages are variable rate.

Europe's consumers have dodged being negatively impacted from the rise in interest rates in 2023 for three main reasons.

- First, borrowers extended much of their debt from short-term adjustable rates to long-term fixed rates. In Spain more than 90% of mortgages featured variable rates in 2015, but by 2020 the share of variable-rate mortgages dropped to less than 25%, replaced by fixed rate mortgages according to data from the Spanish National Statistics Institute and the Bank of Spain.

- Second, spurred by higher rates and solid income growth, consumers paid off some debt, lowering overall debt levels, according to data from the European Central Bank.

- Third, income rose just as fast as debt costs did. Official data from Eurostat through the first half of 2023 shows wages climbed 4.6% since the second quarter of 2022, slightly ahead of the rise in interest rates.

Looking ahead to 2024, wages probably won't continue to rise as fast, and both variable-rate debt and new debt will reflect higher rates. It's likely that household budgets will be tighter than in 2023, a lagged response to the rate increases. In contrast, the drop in the eurozone's inflation towards the ECB's 2% target is a sign that the ECB may begin to reverse rate hikes by mid-2024, easing some of the potential impact on households and helping to slowly improve or maintain economic momentum through the year.

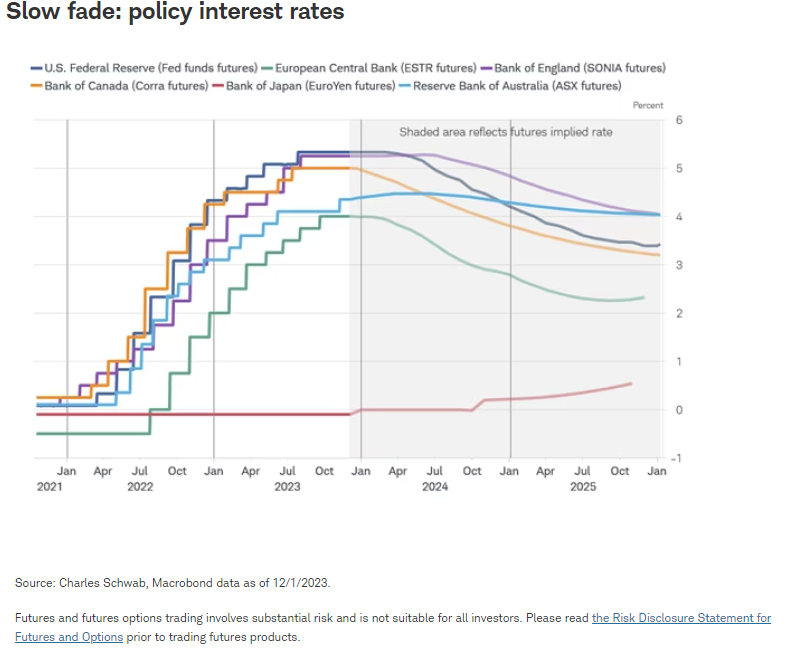

From hikes to cuts

It would be too easy to describe 2023 as a year of rate hikes and 2024 as a year of potential rate cuts since that overstates the change in conditions. While policy rates may be at a peak in most economies, we do not expect them to fall rapidly. The interest rate futures market tied to policy rates reflects a similar outlook in the chart below. The peak in rates is unlikely to look like an upside-down V-shape, instead rolling over only gradually. Quantitative tightening (the unwinding of the asset purchases by central banks during quantitative easing) may still continue and the lagged impact of the cumulative rate hikes may begin to weigh on global growth in the coming quarters, observed in climbing bankruptcies and weakening job markets.

An outlier in any shift to rate cuts next year could be the Bank of Japan. For over a decade, the Bank of Japan's (BOJ) policy has enabled Japan to be an important source of investment funding, with negative interest rates allowing investors to borrow cheaply in yen and then purchase investments in other countries offering a higher return. In 2023 Japan seemed to be pursuing contradicting goals: the BOJ bought bonds in an effort to contain bond yields, making the yen less attractive, while the Ministry of Finance at times bought yen to keep the currency from weakening too rapidly. These conflicting policies seem costly and unsustainable. We believe at some point next year the BOJ may need to allow higher bond yields and raise policy rates.

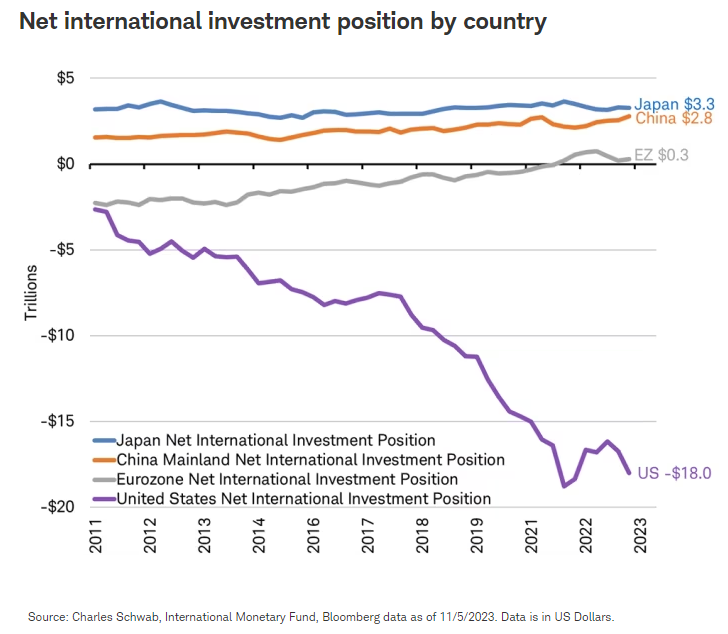

Moves by the BOJ could overshadow those by the Federal Reserve and other central banks if Japanese investors begin to sell foreign bonds, stocks, and currencies. Decades of current account surpluses have accumulated, giving Japan the world's largest net international investment position (even more than China) with $3.3 trillion of investments held abroad according to the International Monetary Fund (IMF). Although the U.S. has the largest economic influence in the world, Japan may have the largest influence in the asset markets due to these account surpluses. Should the BOJ begin to substantially tighten monetary policy next year, as signaled by the end of yield curve control at the BOJ's meeting in October, the potential for a reversal of decades of outward flow of capital may be felt by investors worldwide. With rates rising in Japan contrasting with rate cuts elsewhere, the yen could surge along with Japanese bond yields, prompting Japanese investors to bring their money home and invest in Japanese assets.

The whole picture

Geopolitics are likely to remain a source of market volatility. Despite their unimaginable human toll, these developments had only a marginal impact on most markets around the world in 2023, consistent with historical precedent. Geopolitical developments are difficult to forecast, but we anticipate they may again take a back seat to the economic outlook as the main driver of markets in 2024.

Global economic and earnings growth may ultimately be sluggish for much of next year. That could mean stock prices are more determined by moves in the price-to-earnings ratio than earnings as investors try to figure out what the right valuation multiple is in an environment of higher discount rates and uncertainty over the timing and pace of an earnings rebound. International stock valuations are already braced for a challenging 2024 with investor sentiment surveys in Europe not far from decade lows and the price-to-earnings ratio for the MSCI EAFE Index 15% below its 10-year average, and many Japanese stocks have price-to-book ratios below 1.0. Valuations could lift on clarity around rate cuts and as the economy firms later in the year.

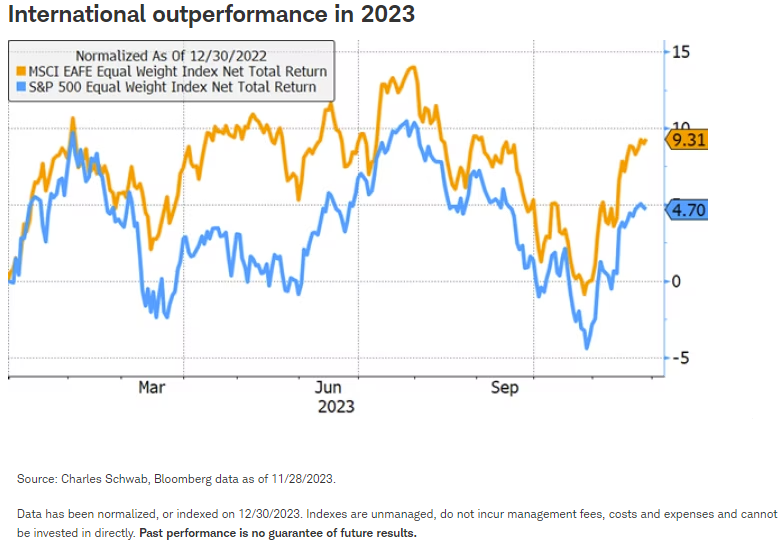

As with the economic picture, looking too closely at the performance of just a few U.S. stocks can keep investors from seeing the bigger picture of international outperformance. As the global economy transitions to a new cycle, markets are experiencing new leadership. In 2023, the average international stock outpaced the average U.S. stock through late November, as you can see in the chart below of the equal-weighted indexes (where each stock in the index gets an equal weighting). The MSCI EAFE Equal-Weighted Index has outperformed the S&P 500® Equal-Weighted Index by nearly 5% in 2023, adding to the 15 percentage points of outperformance since the bear market ended in October 2021.

The reason many investors haven't noticed the outperformance of international stocks is that the seven mega-cap stocks that make up about 30% of the S&P 500 capitalization-weighted index (where the largest stocks get the most weight) have pulled the rest of the stocks higher, preventing the S&P 500 index from underperformance in 2023. In general, the greater the number of stocks that are helping push the overall market higher, referred to as market breadth, the more support the market has. The average international stock continues to outpace the average U.S. stock, offering a broader base of support for developed international stocks. Should the U.S.'s mega-cap seven stocks lag, a possibility without aggressive Fed rates cuts in 2024 to sustain their momentum, the outperformance by the average international stock since the bear market ended in October 2021 may become more obvious.

Emerging market stocks' relative performance is likely to revolve around China and India, the top two countries represented and summing to over 40% of the value of stocks in the MSCI EM Index.

- Reasons prompting concern around investing in China may be improving, yet growth is unlikely to surprise on the upside given the property market overhang. Volatility is likely to remain characteristic of Chinese stocks in 2024. Read more here: Is China investable?

- India's growth momentum may carry it to the top three global economies in size before the end of the decade if it is able to capitalize on its transformative initiatives. India's stocks are expensive, perhaps already pricing in high expectations. Holding a broad mix of exposure to emerging markets includes meaningful exposure to India's growth, but also diversification to help insulate from its risks. Read more here: India: On the Rise

Artificial Intelligence (AI) holds the potential to transform employment, drive faster productivity growth, and drive gains for investors. Business investment is likely to climb in 2024 as the benefits of AI to their businesses become more evident, offering the potential for a productivity payoff in the second half of this decade. AI-related stocks may benefit from increasing capital investment and provide an opportunity for investors as firms look to improve their business processes. But portfolio diversification remains important given the heightened volatility that often accompanies new technologies and likely shifts in leadership as the technology and adoption evolves. Read more about Investing in Artificial Intelligence.

We do not expect a V-shaped economic recovery, nor do we expect an inverted V-shape to the path for interest rates, so we continue to favor "quality" companies with strong cash flow. Stocks with low price-to-cash flow ratios—more heavily represented in the MSCI EAFE Index—may continue to outperform in 2024. While these stocks can be found in all sectors, they are more concentrated in Financials and Energy.

For investors in 2024, what may seem like chaotic data points and volatile market performance on a day-to-day basis may resolve with some longer-term perspective into a clearer and bigger picture of a new multi-year cycle getting underway over the course of 2024.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Please note that this content was created as of the specific date indicated and reflects the author’s views as of that date. It will be kept solely for historical purposes, and the author’s opinions may change, without notice, in reaction to shifting economic, business, and other conditions.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including loss of principal.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets.

Investing in emerging markets may accentuate this risk.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income, small capitalization securities and commodities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

Commodity-related products, including futures, carry a high level of risk and are not suitable for all investors. Commodity-related products may be extremely volatile, illiquid and can be significantly affected by underlying commodity prices, world events, import controls, worldwide competition, government regulations, and economic conditions, regardless of the length of time shares are held. Investments in commodity-related products may subject the fund to significantly greater volatility than investments in traditional securities and involve substantial risks, including risk of loss of a significant portion of their principal value. Commodity-related products are also subject to unique tax implications such as additional tax forms and potentially higher tax rates on certain ETFs.

Currencies are speculative, very volatile and are not suitable for all investors.

The Global Manufacturing Purchasing Managers Index (PMI) is a survey-based indicator of the economic health of the global manufacturing sector. The PMI index includes the major indicators of: new orders, inventory levels, production, supplier deliveries and the employment environment.

The Employment component of the Eurozone Manufacturing Purchasing Managers Index (PMI) measures the conditions surrounding the cost of employment business expenses experienced by surveyed business leaders in the Eurozone.

The Input Prices component of the Eurozone Composite Purchasing Managers Index (PMI) measures the conditions surrounding the prices of raw materials and other business expenses experienced by surveyed business leaders in the Eurozone.

The MSCI EAFE Equal Weighted Index includes the same constituents as the MSCI EAFE Index (large and mid-cap securities from Developed Markets countries around the world excluding the US and Canada), with an alternative weighting scheme where at each quarterly rebalance date, all index constituents are weighted equally.

The S&P 500 Equal Weighted Index includes the same constituents as its parent index, the S&P 500, with each index constituent represented equally.

Market trends are shifting – is your investment strategy keeping pace? Join industry experts as they delve into the equity and bond markets, offering insights into the 2024 outlook. Register for our Market Outlook Symposium, on December 14th at 11 am ET. Click here.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All