Private lenders are increasingly meeting borrowers' needs.

Financial flows have shifted this year. In the credit arena, bank lending has been moribund throughout the year, as standards tightened and interest rates rose. But borrowers still need capital, and private lenders are increasingly meeting their needs.

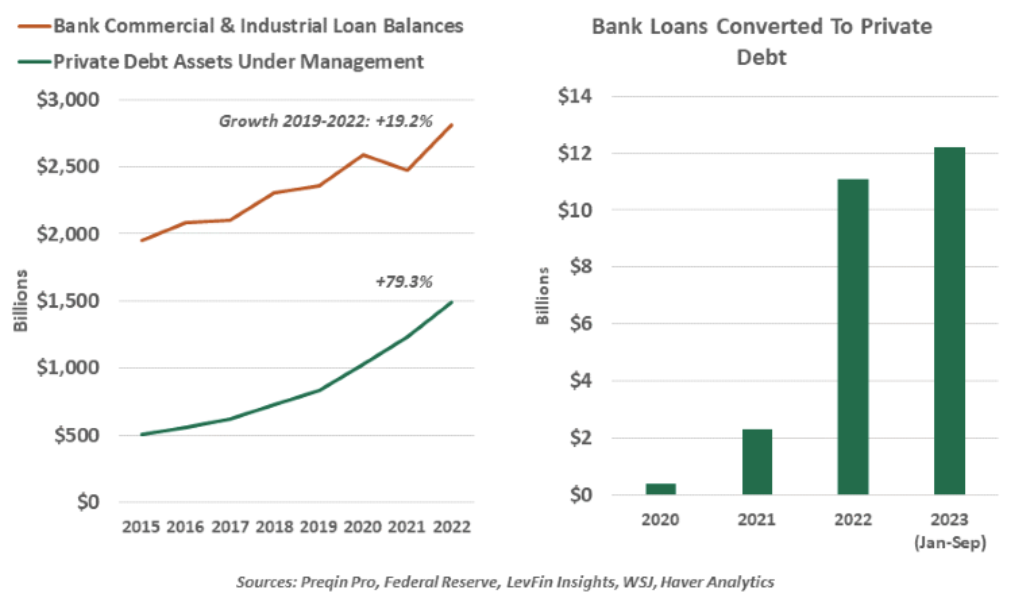

Private debt assets under management nearly doubled during the course of the pandemic. From a starting point of $831 million in December 2019, assets surged to nearly $1.5 trillion at the end of 2022. This is more than half the size of bank commercial and industrial lending. 2023 has almost certainly seen further growth of private lending.

The asset class is not new; private lenders have typically served smaller, more complex or less profitable borrowers who may have struggled to qualify for conventional financing. More recently, the category has grown as more borrowers seek the flexible underwriting and repayment plans that private lenders can offer.

Unlike an actively traded bond, private debt is not marked to market, avoiding the stress of volatile valuations and unrealized losses. If a loan underperforms, the parties can negotiate to extend the loan, restructure the debt or arrange a workout plan, with a greater range of options than the borrower could expect from a publicly-traded vehicle. The lender and borrower are in a closer relationship than an arm’s-length market transaction, creating more openness to alternative arrangements. Indeed, some of this market’s growth has been fueled by refinancing bank loans.

That optionality comes at a cost: private loans are reputed to be more costly than public debt, though the specifics are kept confidential. The private market is opaque and lightly regulated. Private credit funds do not need to disclose their investors, their borrowers, nor any terms of their funding or deals. These arrangements make it difficult to compare the performance and returns of private debt against other markets. And importantly, we cannot know the extent of investments in the sector to gauge whether any losses could be the beginnings of a systemic shock.

Funding for private credit comes exclusively from large, accredited investors. Many private equity funds are shifting their focus away from equity and into debt. These market participants should be in the best position to understand the risks of the market and gauge their own risk appetite. However, as more investors seek opportunities in this market, its risk as a vector of contagion grows. The yields offered by private debt may have tempted a wider swath of investors, who could face a shock if deals turn sour. Many private lending funds have credit lines from traditional intermediaries which could be drawn upon under duress, causing stress to spread through traditional bank channels.

Some of the new growth in private credit has come from an older channel: business development companies (BDCs). BDCs are a tax-advantaged corporate structure dating to the 1980s. They are closed-end investment funds that must invest in small and midsized U.S. businesses and must pass over 90% of their profits to shareholders. BDCs’ total assets have more than doubled since 2021, and they now represent a quarter of assets under management in private credit. Even in a well-established vehicle, this sort of growth raises suspicion of excess.

The forces fueling the current rise of private debt are similar to past drivers of growth in alternative asset classes. Regulated intermediaries, facing pressure on capital and liquidity, pull back; non-traditional providers step forward. Private debt has helped to sustain economic growth in this cycle, but it is lightly regulated. A downturn would certainly test the resilience of this sector, and potentially the whole of the financial system.

In an efficient market, capital will flow to where it expects to earn the highest return. At the moment, private credit is providing that outlet to many investors, with some productive outcomes. But as with all elevated flows, we will continue to monitor this channel as a source of risk.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Northern Trust

Read more commentaries by Northern Trust