The Survey of Consumer Finances wasn’t the only significant report released by the Federal Reserve last week. The semiannual Financial Stability Report (FSR) was also noteworthy.

The last FSR was issued in May, amid the banking turmoil that marred the spring. Interestingly, we rarely talk about that episode much anymore, as threatening as it seemed at the time. Deposit levels at banks have stabilized, and we have seen no further distress.

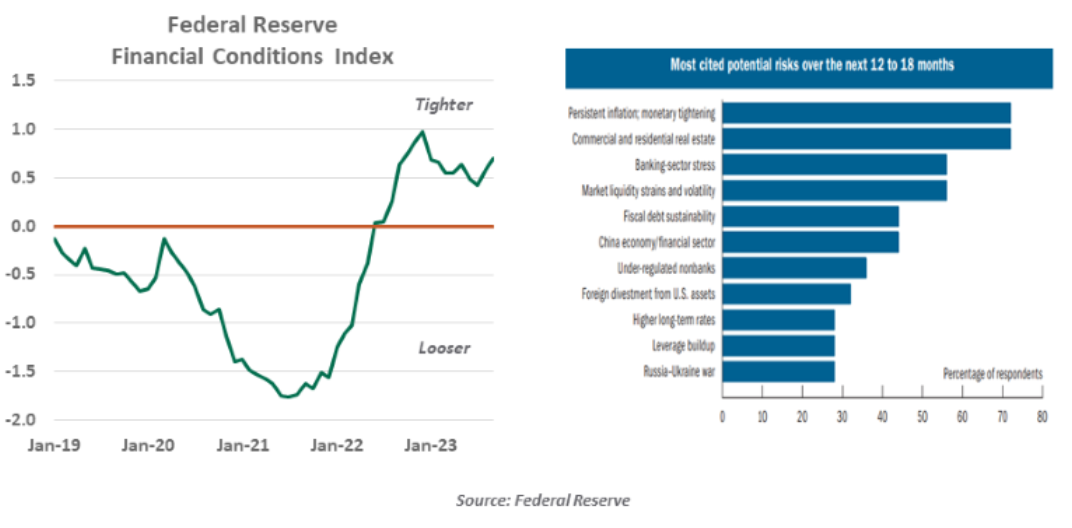

But the bank failures of last spring led to a tightening of credit. The Fed’s own gauge of financial conditions, which places heavy weights on bank lending standards and long-term interest rates, has swung from easy to restrictive in a very short space of time. Further, the regulatory environment surrounding banks has become more limiting. As these changes take deeper root, it will produce economic headwinds and stress some portfolios.

The latest FSR attempts to anticipate where this stress might surface. The report focused attention on the following candidates:

- There is not a lot of public information about alternative asset classes, so we know little about their sensitivity to interest rates or other market movements. By design, there is a lot of equity in these vehicles that can absorb losses, but most funds also have credit lines that can serve as a channel of financial contagion if trouble arises.

- Higher interest rates and hybrid work have hindered commercial real estate values. There are concentrations of exposure to this sector in small banks and certain investment products.

- Tight monetary policy in Western countries has limited demand for exports. As the world’s leading exporter, China has borne the brunt of this development.

As the world’s second largest economy, China is well represented in many investment portfolios. That has been beneficial to returns in most years, but China’s recent financial challenges could be a source of underperformance and systemic risk.

While not related to interest rates, the FSR also expresses justifiable concern over the potential for international unrest to shock markets and produce instability.

Thankfully, most of the concerns raised in financial stability reports never come to fruition. But that doesn’t diminish the value of the surveillance. Let’s hope for the best, but prepare for the worst.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Northern Trust

Read more commentaries by Northern Trust