A Deep Dive Into U.S. Debt

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe longer the U.S. debt is left to grow, the harder it will be to correct.

The most popular economic article I have ever written was a cautionary tale about the national debt of the United States. I warned that it was on a troubling trajectory, and implored policy makers to take corrective action before it was too late.

I thought the content was well-constructed, but that wasn’t the reason that the piece was so popular. The essay was phrased as an open letter to my baby daughter about the financial future she, and others of her generation, might face. The inclusion of a cute picture of her crawling around our family room floor was a blatant attempt to boost ratings, and it worked.

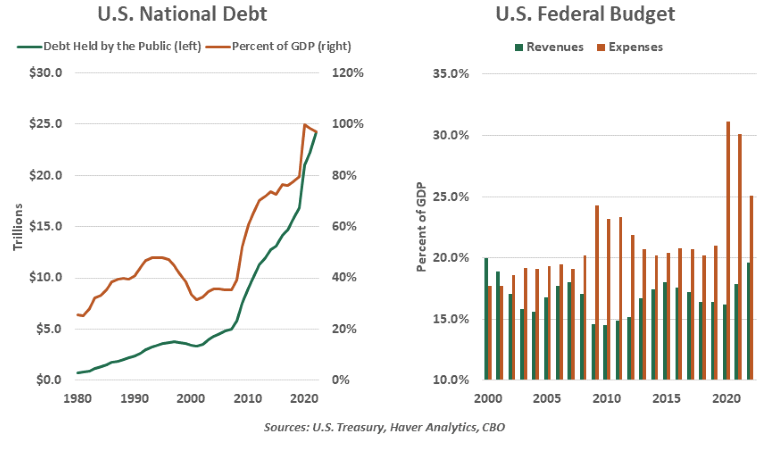

Nostalgia sets in when I remember that piece. Both the baby and America’s fiscal position were relative innocents back then: my daughter was 10 months old, and the Federal debt was about $5.5 trillion. The former is now in her mid-twenties, and the total national debt stands at more than $33 trillion.

The level of concern about the size and sustainability of U.S. debt has increased substantially this year. The deficit for fiscal year 2023 is projected to be around $2 trillion, an unusually large amount during a period of strong economic growth. Rising interest rates make the cost of carrying the debt much more significant. And political dysfunction in Washington raises serious questions about the soundness of fiscal policy.

In response to a rising number of client questions, we’re devoting our entire issue this week to an analysis of the American fiscal picture. We’ll attempt to diagnose how we got here, anticipate where we are going, and offer some potential remedies. We will also tackle the question of whether the United States is close to a breaking point at which the debt becomes too great for the market or the country to bear.

Our main conclusions:

- The U.S. national debt is on a dangerous trajectory, one that will test the market’s willingness to accept unlimited amounts of our credit.

- Bending the deficit curve will almost certainly require a combination of sizeable revenue enhancements and spending curbs.

- Containing spending will require review of entitlement programs, which legislators have been reluctant to do.

- The United States has the means to manage its debts, but not the political will to do so.

Background on these points, and others, follows.

Red Tide

“How did you go bankrupt?"

Two ways. Gradually, then suddenly.”

― Ernest Hemingway, The Sun Also Rises

The route to the current U.S. fiscal problem has both gradual and sudden elements.

The sudden component is the result of the two substantial economic shocks that we have experienced in the last 15 years. As is apparent from the charts, debt and deficits increased sharply after the Global Financial Crisis (GFC) in 2008 and the COVID-19 pandemic. Fiscal policy took a leading role in the recovery from each challenge, stepping in to offset steep declines in private demand.

The U.S. government spent about 7% of gross domestic product (GDP) on relief programs after the GFC. The economic recovery that unfolded in subsequent years was sluggish; employment took five years to return to the levels of early 2008.

That experience likely informed the government’s response to COVID-19. The nature of the pandemic was different from the GFC, but there was a strong sense among policy makers that they needed to do much more than they had before. In all, fiscal support in the wake of COVID-19 amounted to about $5 trillion, almost 25% of GDP.

That total does not include three large-scale bills passed in the wake of the pandemic, which have more to do with industrial policy. In the short term, these bills have founded a construction boom, but only time will tell whether the increments of economic activity produced by the legislation will be budget neutral.

The gradual elements can be found on each side of the ledger. The U.S. Congress passed major tax reductions in 2001, 2003 and 2017. Some features of these measures were set to expire after a few years, but fears of a “fiscal cliff” that would damage the economy led many of them to be extended. Major provisions of the 2017 Tax Cuts and Jobs Act are scheduled to sunset in 2025, but many think that at least some of them will be extended.

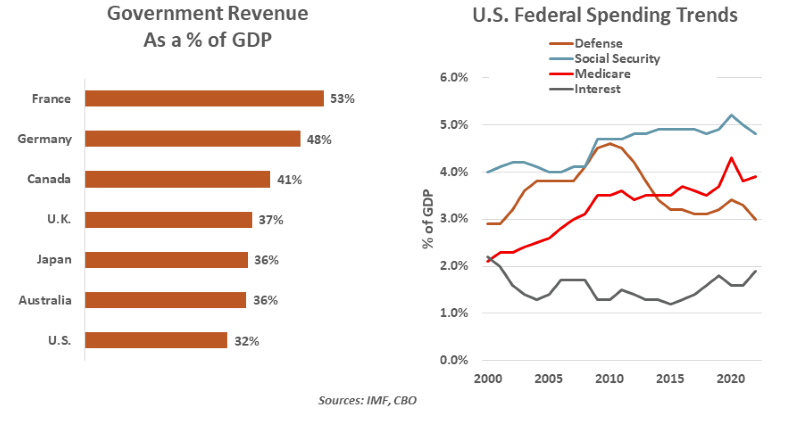

U.S. tax revenues as a percent of GDP are among the lowest of any developed country. There are those who note that low tax rates can be supportive of economic activity: reductions in taxes over the past two decades have been justified on the grounds that incremental growth would leave the federal budget relatively unaffected. We have called this fuzzy math, because it does not appear that tax cuts have come anywhere close to paying for themselves.

On the spending side, the country’s aging demographics have been a driver of cost increases in the two largest entitlement programs, Social Security and Medicare. These categories contribute most to projected increases in the U.S. national debt held by the public, which is forecast to grow from 98% of GDP at present to a whopping 180% of GDP in thirty years.

About 85% of what the U.S. federal government spends goes to three categories: interest, defense, and mandatory programs headlined by Social Security and Medicare/Medicaid. Interest will fluctuate with market rates, but cannot be actively managed without reducing the debt.

Defense spending in the United States takes up a higher fraction of GDP than it does for most other developed countries. For decades, America has organized and provided security far beyond its borders; there have been conversations over recent years about changing cost-sharing arrangements between countries. But in the current geopolitical environment, defense is not likely to be a primary candidate for cuts.

Meaningful progress on spending control can therefore not be achieved without considering mandatory categories. Following is analysis of the two largest pieces of that puzzle.

Preparing For Retirement

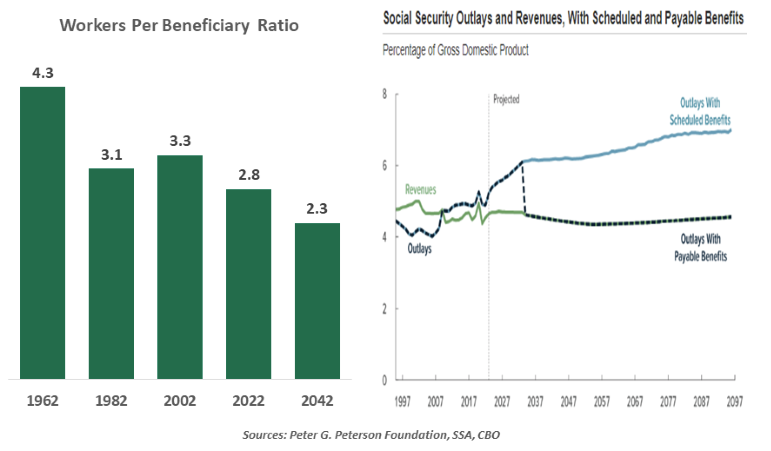

Social Security (SS) is the largest single federal program in the United States. It is a self-financing program in which today’s benefits are funded primarily by a 12.4% payroll tax collected from current workers and employers. Inflows not needed to pay benefits are deposited into the SS trust fund.

Since its inception in 1935, SS collected more in payroll taxes and other income than it paid in benefits and other expenses, leaving the trust fund with reserves of $2.8 trillion as of March 2023. As mandated by the law, these accumulated reserves are invested entirely in U.S. Treasuries.

Even though retirement benefits in the U.S. are modest compared to several other advanced economies, America’s Social Security system is coming under increasing pressure due to shifting demographics. Life expectancy has increased since the system was first constructed, which means the program pays beneficiaries over a longer period of time. America is also graying rapidly, with about 10,000 baby boomers retiring every day. About 67 million American residents are receiving retirement benefits each month, a number that is expected to swell to 77 million by 2031 as the last Baby Boom generation begin taking benefits.

With the number of retirees growing much faster than the ranks of new workers, the share of workers paying into the system (via payroll taxes) has been falling relative to the number of recipients. This imbalance has led SS to draw down trust fund reserves to help pay for benefits since 2021. Without legislative action from Congress, the trust fund reserve is projected to be depleted in the year 2034.

The Social Security system can only spend what it takes in. According to the most recent Social Security Trustees’ analysis, depletion of the trust fund will require benefit cuts of 23% across the board as the program transitions to funding only through current contributions.

SS is the biggest source of retirement income for most retirees. Without retirement benefits, 4 in 10 adults aged 65 and above would have incomes below the poverty line. Therefore, it is imperative to find a sustainable solution.

Historically, Congress has fixed shortfalls in the Social Security system by raising payroll taxes, increasing retirement ages, and adjusting benefits. Other potential fixes include modifying the benefit formula, changing the annual cost-of-living adjustment calculation, raising the cap on taxable earnings subject to the payroll tax, and increasing the financial penalties for claiming Social Security before full retirement age.

Means-testing of benefits has been proposed on a number of occasions. Many Americans have other sources of retirement income that are significant, and may not need to rely as heavily on Social Security. But this idea has struggled to advance, partly because of the mistaken belief among some that they have an account in the Social Security system and are entitled to the balances it contains. In truth, Social Security is a transfer payment system, not a bank; and it was intended as an insurance program, not an entitlement.

The decade-long window before trust fund depletion gives policymakers time to craft a plan that helps balance the program. However, neither Republicans nor Democrats want to be the first to advance curbs on a very popular public program. Social Security has been described as the third rail of American politics, and no one has an appetite for a shock.

Health Issues

Very little about the funding and delivery of American healthcare is simple. And for a program designed to meet the medical care needs of the entire U.S. population age 65 and over, the costs and complexities are immense.

Medicare is structured in four parts: Part A covers inpatient hospital and nursing care; Part B covers outpatient services and doctor-administered prescription drugs; Part D covers self-administered prescriptions; and Part C (or Medicare Advantage) fills in coverage gaps, limits annual costs, and reduces the co-pays and deductibles of Part A and B plans. While heavily subsidized, Medicare isn’t free: plans charge premiums, deductibles and coinsurance.

Like Social Security, Medicare is funded through dedicated payroll taxes. Programs are administered by each state, using block grants from the federal Department of Health and Human Services.

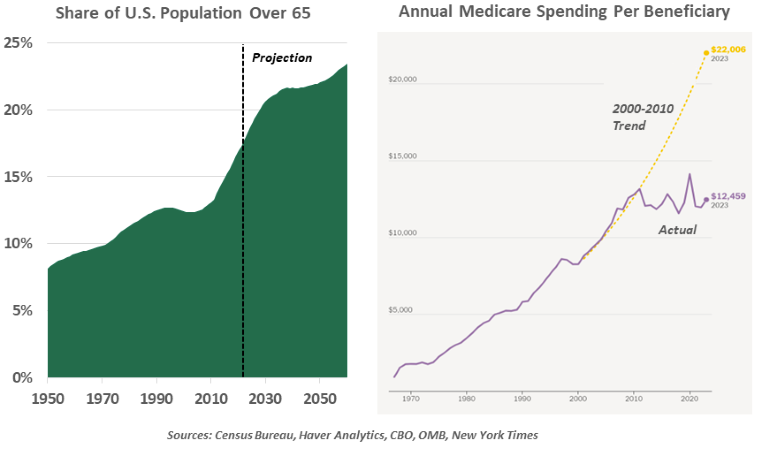

In 2022, Medicare expenditures exceeded $1 trillion, representing 16% of federal outlays or 3.1% of the nation’s GDP. This share is poised to increase along with the aging population. The Congressional Budget Office foresees Medicare expenditures rising to 5.5% of GDP in 2053.

Though the costs are growing, one silver lining has emerged. In the past decade, the cost of Medicare per enrollee has held mostly flat, after growing rapidly from the program’s outset. For decades, longer lifespans, better (but more expensive) health services, and the widening scope of Medicare pushed costs continually upward.

Since 2010, however, cost growth has been modest, contained by fewer new expensive care services and more availability of generic prescriptions. Most recently, the pandemic reduced healthcare costs as non-essential treatments were deferred; those who succumbed to COVID may have avoided other costly end-of-life care.

Even if cost containment can continue, the rising share of the elderly population will make the Medicare program increasingly burdensome. The Census Bureau forecasts the population over 65 will grow by more than 2% each year through the remainder of the decade. The Medicare costs for retirees will be borne by a working-age population that will not grow at nearly the same rate.

Medicare’s finances are on a challenging path. Much like Social Security, Medicare is supported through current contributions, buffered by a set of trust funds. The fund supporting Medicare Part A will remain solvent through 2028; at that point, contributions can support 90% of costs. The trust funds for other Medicare components are not forecast to be depleted.

Remediation through tax reforms and cost controls can go a long way to improve the program’s solvency. The president’s most recent budget proposal included a higher Medicare payroll tax rate on the highest earners, who already pay the highest marginal income tax rate. Owing to its size, the Medicare program has leverage to negotiate lower costs from healthcare providers, a tactic used in past funding shortfalls. Marginal reforms to both revenues and expenses can rebalance and sustain this popular and vital program.

Tipping Point Ahead?

We often get the question of how much debt is too much for the United States. As I expressed in my article from so many years ago, I thought we had reached our limit in the early 1990s. Yet here we are.

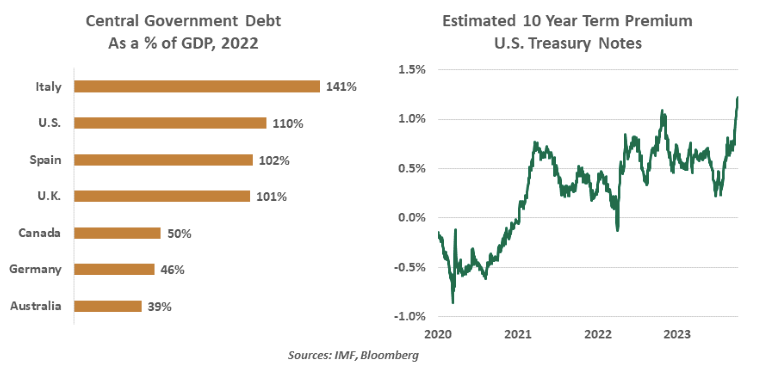

America is not the only indebted country in the world. Sovereign borrowing around the globe has risen substantially over the past 15 years, with particular speed during the past three. But the level of debt (relative to GDP) in the U.S. places it in the company of nations like Spain, which are not known as bastions of budget discipline. If America continues along the projected path, its debt could rival and surpass that of Italy or even Greece.

Almost all of the examples of countries losing control of their finances come from the emerging world. Smaller countries have less wealth, relatively little inbound investment, and an inability to stabilize their currencies. So there is little we can learn from past sovereign defaults about what might lie ahead for the United States.

One important yardstick to watch is the relationship between economic growth (g) and the rate of interest (r). If your income is rising more quickly than your interest payments, handling debt is easier. For most of the past 25 years, g has been greater than r for the United States. But the two quantities have converged over the last year and a half.

Looking ahead, the ability of the American economy to grow will depend on growth in the labor force and growth in productivity. Neither is on a comfortable track at the moment, and policy will need to focus on improving our potential. Maintaining g > r is critical to debt sustainability.

At the moment, there is little evidence that the United States is losing traction as a reserve currency. The representation of the U.S. dollar in official reserves and international transactions remains little diminished. Auctions of new Treasury bills, notes, and bonds still attract substantial interest from domestic and foreign buyers. This has helped to offset the recent decline in purchases by the Federal Reserve.

Nonetheless, rating agencies are concerned. In our essay Not Making the Grade, we highlighted the role that political dysfunction plays in the assessment of America’s creditworthiness. Polarization within and across parties is making consensus much more difficult to achieve. Government shutdowns have become more common, and the United States has flirted with temporary defaults on several occasions. This has raised the “term premium” that investors require to hold long-term Treasury notes. Those extra basis points act as a tax on Americans.

To change its financial trajectory in any meaningful way, difficult decisions will have to be made. Unfortunately, the political calculus is taking precedence over fiscal calculus in Washington. Representatives are loath to cast a vote that might help the nation’s finances in five years, but which might lose them their seat in the next election. But kicking the can further down the road is a losing strategy.

A new baby entered my life this summer. My grandson is perfect in every way, and I hope for only the best things for him. But I do worry that the fiscal situation he will inherit may narrow his path to prosperity. He, and others of his generation, deserve better.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulations. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All