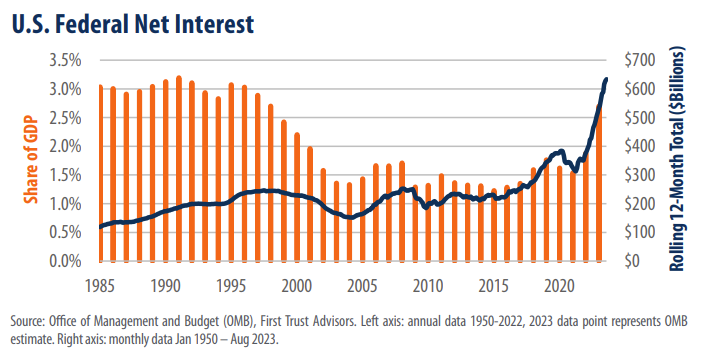

In this week’s installment of “Three on Thursday,” we take a long-term historical look at U.S. federal government finances. With annual deficits now in the trillions and interest payments on government debt at all-time highs, something needs to change. This sparks a longstanding debate: Are the wealthy truly not contributing their fair share, as the President asserts, or is it potentially a matter of excessive government spending? Our stance leans toward the latter. For some perspective, if the government were to seize the combined net worth of the Forbes 400 wealthiest individuals (totaling $4.5 trillion in 2023), it would merely sustain the government’s operations for a little over eight months. To illustrate further, supposing the Democrats successfully increased the top marginal tax rate from the current 37% to an extraordinary 100%, this policy change would impact 922,362 taxpayers based on the most recent data available, extending through the 2020 tax year. Such a change would generate approximately $580.7 billion in additional revenue, assuming no behavioral changes, retirements, or career shifts among affected individuals. This extra revenue injection would only run the government for an extra 33 days. To provide further insight, we’ve included three informative charts below.

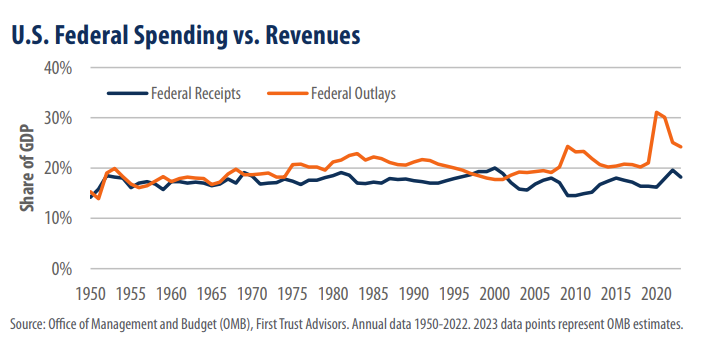

Looking back to 1950, government revenues have averaged 17.3% of GDP. During this time frame, the top marginal tax rate has exhibited significant fluctuations, ranging from a peak of 92% to a low of 28%. Interestingly, the best year for revenue as a share of GDP was 2000 when the highest marginal tax rate stood at 39.6%. Yet over this same period government spending has averaged 20.0% of GDP, hitting a record high of 31.1% of GDP in 2020. In the fiscal year 2023, revenues as a percentage of GDP were estimated to be at 18.2%, surpassing the historical average. Conversely, spending was estimated to reach 24.2% of GDP, easily exceeding the historical average.

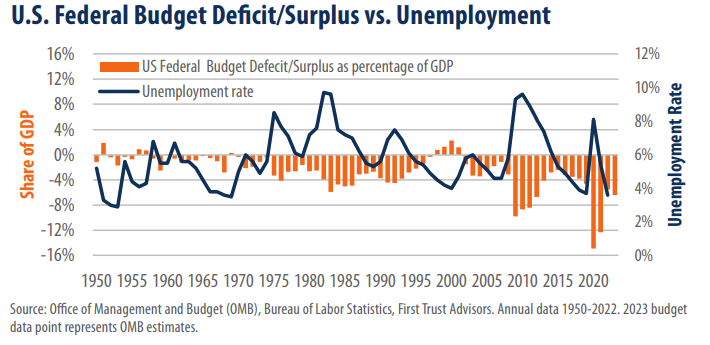

The projected U.S. deficit for fiscal year 2023 is 6.4% of GDP. It’s noteworthy that from 1950 through 2008, there was not a single year where the budget deficit equaled or exceeded 6.4% of GDP. Not one. There is room for reasonable debate regarding the appropriate size and scale of budget deficits during the aftermath of the Great Recession and the COVID lockdowns. However, running a deficit of this magnitude at present, particularly in a time of peace and historically low unemployment rates, is a cause for concern.