The Bank of Japan met last night to cap off a week of central bank activity. From their policy statement:

“The Bank decided, by a unanimous vote, to set the following guideline for market operations for the intermeeting period.

The short-term policy interest rate: The Bank will apply a negative interest rate of minus 0.1 percent to the Policy-Rate Balances in current accounts held by financial institutions at the Bank.

The long-term interest rate: The Bank will purchase a necessary amount of Japanese government bonds (JGBs) without setting an upper limit so that 10-year JGB yields will remain at around zero percent.”

When discussing inflation they opined: “On the price front, the year-on-year rate of increase in the consumer price index (CPI, all items less fresh food) is slower than a while ago, mainly due to the effects of pushing down energy prices from the government’s economic measures, but it has been at around 3 percent recently owing to the effects of a pass-through to consumer prices of cost increases led by the past rise in import prices. Inflation expectations have shown some upward movements again.”

With respect to growth, the BoJ expressed a rather optimistic assessment: “Japan’s economy is likely to continue recovering moderately for the time being, supported by factors such as the materialization of pent-up demand, although it is expected to be under downward pressure stemming from a slowdown in the pace of recovery in overseas economies. Thereafter, as a virtuous cycle from income to spending gradually intensifies, Japan’s economy is projected to continue growing at a pace above its potential growth rate.”

So, inflation pressures are resilient and growth is expected to continue above potential. Isn’t that all the ingredients needed for a central banker to talk hawkish?

Not in Japan, where the BoJ statement goes on to emphasize the uncertainty of global conditions as the reason for its inaction: “Concerning risks to the outlook, there are extremely high uncertainties surrounding Japan’s economic activity and prices, including developments in overseas economic activity and prices, developments in commodity prices, and domestic firms’ wage- and price-setting behavior… With extremely high uncertainties surrounding economies and financial markets at home and abroad, the Bank will patiently continue with monetary easing while nimbly responding to developments in economic activity and prices as well as financial conditions.”

So, there you have it. Inflation is higher than expected, with another uptick expected, while growth is above potential and the BoJ decides to sit on its hands. Of course!

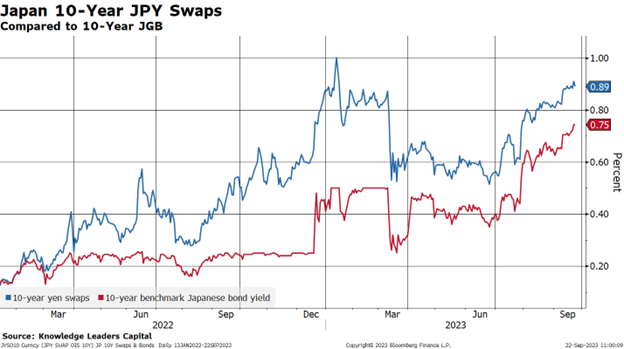

The markets, on the other hand, seem to be looking through these contradictory statements. This we can observe in two ways. First, 10-Year JGBs keep pushing higher toward the new 1% cap on yields, with the inflation swap suggesting yet higher yields to come.

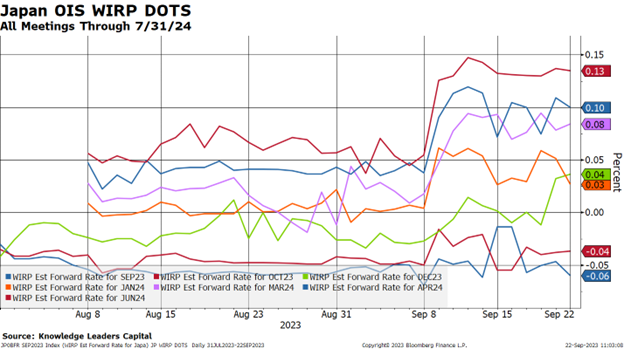

Second, looking at the OIS model, the market seems to be pricing in the BoJ moving the overnight rate—currently at -0.1%–to something higher, into positive territory. Futures are pricing overnight rates to rise to 13bps by next June, which translates into one 25bps increase in the overnight rate. More imminently, the market is pricing the overnight rate to flip into positive territory by December 2023 and continue rising from there.

So, while the BoJ continues with its message of patience, the market is beginning to test that patience. It seems the BoJ is in play, and they don’t even seem to realize this, not acknowledging reality in their statement or even addressing market expectations.

Disclosures

The information presented here is for informational purposes only and is not to be construed as an offer to sell, or the solicitation of an offer to buy, securities. Some investments are not suitable for all investors, and there can be no assurance that any investment strategy will be successful. Hyperlinks may be included in this message that provide direct access to other internet resources, including web sites. While we believe these links are to reliable sources, Knowledge Leaders Capital (“KLC”) has no control over the accuracy or content of information contained on these sites. Although we make every effort to ensure such links are accurate, up to date and relevant, we have no control over pages maintained by external providers. The views expressed by these external providers on their own web pages or on external sites they link to are not necessarily those of Knowledge Leaders Capital.

The information provided on this blog is for illustrative or example purposes only and should not be construed as KLC’s opinion or investment outlook. As of the most recent quarter end, the named companies may have been held by KLC. For full information including additional policies and full disclosures, please visit our website: KnowledgeLeadersCapital.com.

Any reference to Index performance does not represent the performance of any investment product offered by Knowledge Leaders Capital, LLC. An investor cannot invest directly in an index. The performance of client account may vary from the Index performance. Index returns shown are not reflective of actual investor performance nor do they reflect fees and expenses applicable to investing.

Companies are selected for “Spotlights” based on high levels of innovation activities in their respective industries and illustrate innovation being employed across all sectors and geographies. Spotlight selection is separate from stock selection by the investment team. Spotlights are not necessarily representative of investment opportunities and can be selected regardless of investment performance or inclusion as a KLC holding.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Knowledge Leaders Capital

Read more commentaries by Knowledge Leaders Capital