Drew O’Neil discusses fixed income market conditions and offers insight for bond investors.

Anyone who even casually pays attention to the financial media has likely become familiar with the current state of inflation as well as how high interest rates have risen over the past ~2 years. Inflation has come down from its recent highs but remains well above the FOMC’s target and is currently 1% higher than its average over the past decade*. Similarly, fixed income yields across the curve are at or near their highest levels over the same timeframe. At the intersection of yield and inflation is what we call real yield. Real yield is essentially an inflation adjusted measure of yield. This tells you how the spending power of an invested dollar increases versus traditional yield which measures growth on a nominal basis. A positive real yield means that the yield is higher than inflation while a negative real yield means that inflation is higher than the yield.

Depending on the purpose of an investment, real yields may or may not be a high priority data point in your analysis. For most fixed income allocations where safety and return of principal are priority #1, the known aspects of owning individual bonds (known cash flow, known redemption value, and a known redemption date) are likely the most important considerations when choosing an investment. Expected return and yield (whether real or nominal) are likely a secondary consideration when allocating to fixed income (i.e. owning little or no fixed income because yields are low is likely not in alignment with most investor’s long-term financial plans).

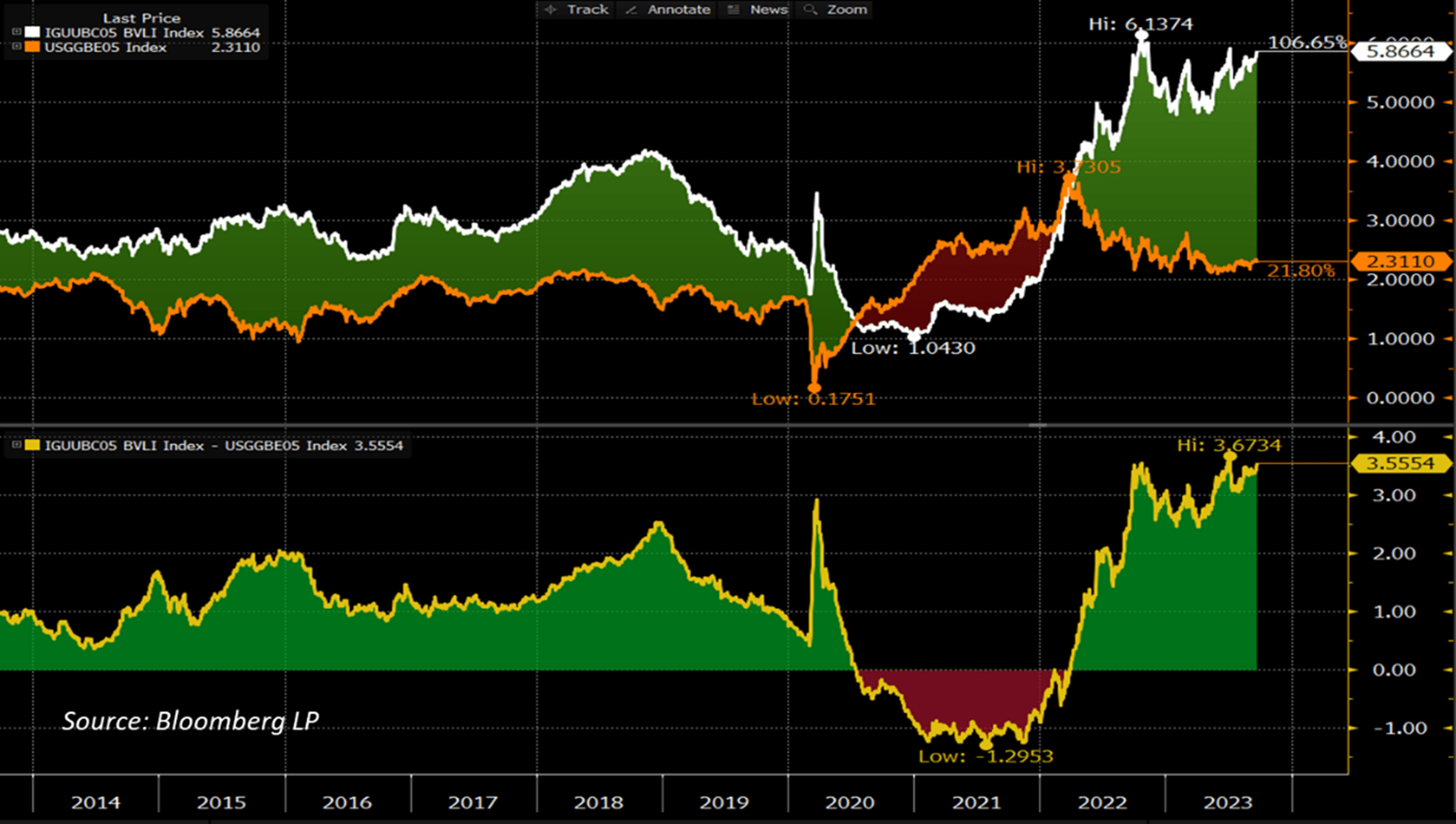

That being said, when the fixed income landscape presents attractive yield opportunities, it gives investors the ability to receive the known aspects that individual bonds provide while also earning attractive returns. Now is one of those times. The yields that are available in high-quality fixed income are at or near their most attractive levels in over a decade from both a nominal yield perspective as well as a real yield perspective. Nominal yields are regularly talked about, so today I wanted to shine some light on how attractive real yields are right now. To highlight the real yield opportunity, the graph below compares the 5-year BBB corporate bond yield* with the market expected average inflation* over the next 5 years. The difference between these two numbers provides the expected 5-year real yield for BBB rated corporate bonds.

The top portion of the graph shows the BBB corporate yields (white line) and the expected inflation rate (orange line). The bottom portion shows the real yield, which is the difference between the two. Two things likely jump out at you: 1) post-COVID created a unique scenario where yields were below expected inflation (red shaded regions), and 2) we are currently at some of the most attractive levels on BOTH a nominal yield basis and a real yield basis over the past decade. Based on these metrics, an investor would expect to earn ~3.55% ABOVE expected inflation by purchasing a 5-year BBB rated bond today. This is an opportunity that has not been available in a long time and may not last very long. The post-COVID negative real yield environment is a good reminder to not take positive real yields for granted, as they are not a given and can disappear quickly.