When markets are in a rising tide, all boats (aka stocks) can benefit. When the waters are choppier, active equity selection aims to identify the sounder vessels. Tony DeSpirito reviews five reasons why he believes the new environment is setting up to favor an active approach.

After years of low inflation and interest rates, the economic and market backdrop is decidedly different today. Higher rates have low-risk investments like Treasuries and money market funds offering yields in the area of 4%-5%. This challenges the investment thesis for higher-risk assets such as equities. Yet the long-term picture shows that stocks are still a portfolio’s primary growth engine and have outperformed bonds more often than not across time horizons, as illustrated below. This was the case even as the average 10-year Treasury yield over the 65-year period we analyzed was higher than today, at 5.75%.

But as we discuss in Equity investing for a new era: The return of alpha, the investing backdrop now forming calls for a fresh look at how to gain equity exposure. Higher stock valuations than at the start of the prior regime 15 years ago, plus higher interest rates, means less return from markets broadly (beta) and, we believe, greater opportunity for skilled active managers to generate alpha, or above-market return.

We identify various market dynamics taking shape that support the case for a stock-by-stock, alpha-centric approach to equity investing:

1. Volatility more likely to increase than decrease

Equity market volatility, as measured by the VIX, has been relatively muted in 2023 ― just as rates volatility has been high. This disconnect suggests ample uncertainty in the marketplace and greater potential for equity volatility to pick up. Geopolitical concerns, supply disruptions and a data-dependent Fed committed to fighting inflation are all likely to stoke bouts of volatility across time.

The market dips inherent in volatility can lead to mispricings, presenting opportunities for active stock pickers to purchase shares of companies with good prospects at a discount.

2. Stock dispersion more likely to broaden than narrow

Stock dispersion was muted after the 2008 global financial crisis (GFC) with little difference in return across top and bottom performers. It was a beta-driven environment in which a rising tide lifted all boats. This reduced the reward to stock pickers, as there was smaller advantage to identifying “winners” or avoiding “losers.”

Our analysis of stock return dispersion across time has found average dispersion since 2020 to be more akin to the pre-GFC period than the 10+ years after it. We believe this normalization sets up an environment in which skilled stock picking can once again provide more meaningful contribution to portfolio outcomes.

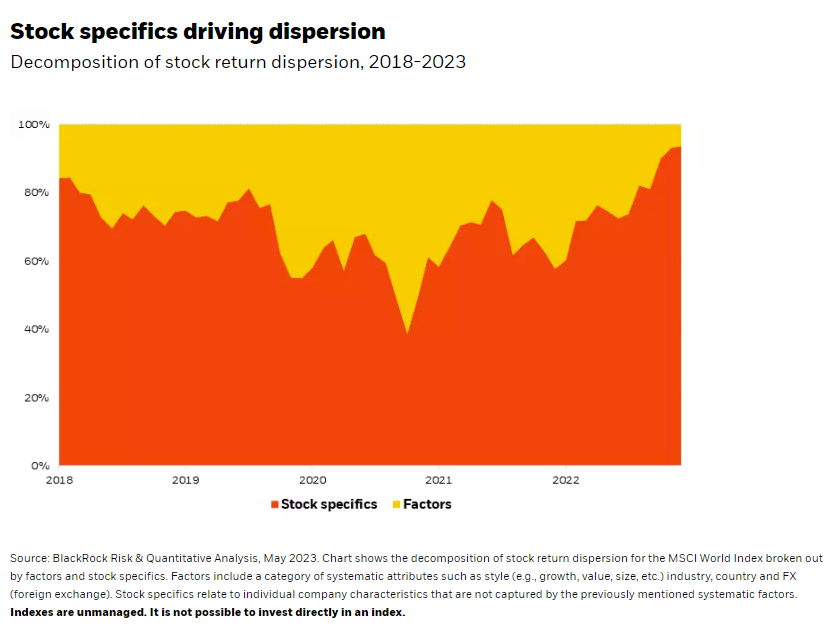

3. Stock specifics gaining influence

Our data further finds that the reason for this greater dispersion in returns is increasingly based on stock-specific variables and less on the factor characteristics of the stocks (e.g., growth vs. value, small vs. large), which were more dominant in 2020 and 2021. See chart below.

While the continuation of these trends cannot be assured, we believe active selection focused on fundamentals can have greater bearing on investor outcomes. We also expect to see an increasing shift in focus from macro concerns at large to how individual companies are able to navigate an environment of slower growth and higher inflation and rates, making company specifics more important to investment decision-making.

4. Market breadth poised to widen

Market breadth has been historically narrow, with 22% of the S&P 500 Index’s market cap attributed to the top five stocks as of June 30. This compares to just under 16% pre-COVID (year-end 2019) and 13% ahead of the GFC (year-end 2007), according to data from Refinitiv.

Comparing the index’s market cap-weighted (16%) and equal-weighted (6%) returns at mid-year illustrates just how much the mega-cap stocks ― primarily tech-related shares across IT, telecom services and consumer discretionary ― have driven year-to-date index performance. As the market increasingly acknowledges and values company fundamentals, we expect market breadth to widen beyond the current leaders and create greater opportunity for active stock pickers with the research capabilities to identify companies with strong fundamentals and attractive long-term growth prospects.

5. AI-driven opportunity and disruption

Given its wide reach and immense potential, we see artificial intelligence (AI) contributing to increased dispersion in the marketplace. Among software companies, for example, the winners will successfully incorporate AI into their products and be able to raise prices while those that fail will become obsolete. Elsewhere in technology, we could see some companies using AI to increase profitability while others merely experience it as a cost of doing business. The impact is not limited to the tech sector. Across industries, we expect new business models will arise, powered by AI innovation, and others will be disrupted (e.g., call centers where humans are displaced by chat bots). Understanding of AI use cases, implications and risks across sectors, industries and individual stocks will have growing influence on investment outcomes, in our view.

The bottom line

Markets are unpredictable, but we believe the dynamics coming into place set up a more favorable environment for active stock selection ― creating an opportunity for skilled stock picking to have a bigger impact on portfolio outcomes and arguing for a new approach to equity investing that puts alpha at the center.

Investing involves risk, including possible loss of principal. Stock values fluctuate in price so the value of your investment can go down depending on market conditions.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of September 2023 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader. Past performance is no guarantee of future results.

You should consider the investment objectives, risks, charges and expenses of any BlackRock mutual fund carefully before investing. The prospectus and, if available, the summary prospectus contain this and other information about the fund and are available, along with information on other BlackRock funds, by calling 800-882-0052 or from your financial professional. The prospectus should be read carefully before investing.

Prepared by BlackRock Investments, LLC, member FINRA

© 2023 BlackRock, Inc. or its affiliates. All Rights Reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© BlackRock

Read more commentaries by BlackRock