BlackRock and Human Interest have found that a primary reason lower income workers are not saving for the future1 is because they do not have access to intuitive and automated savings tools, not because they do not want to or cannot afford to.

In 2017, a Federal Reserve report found that 40% of Americans couldn’t cover an unexpected $400 expense.2 Several years later, that figure remains relatively unchanged at 37% - and for people living on low-to-moderate incomes, it’s 58%.3 Certainly, it’s hard to save for tomorrow if you’re worried about making ends meet today. But, when workers are provided access to the right savings tools and opportunities, the outlook can change.

Over the past four years, BlackRock’s philanthropic Emergency Savings Initiative ran 43 financial security studies and pilot programs, created specifically with the goal of reaching low-to-moderate income households across the United States. Looking across these projects, it’s clear that, when people have access to savings programs, they are empowered to set aside money for the future.

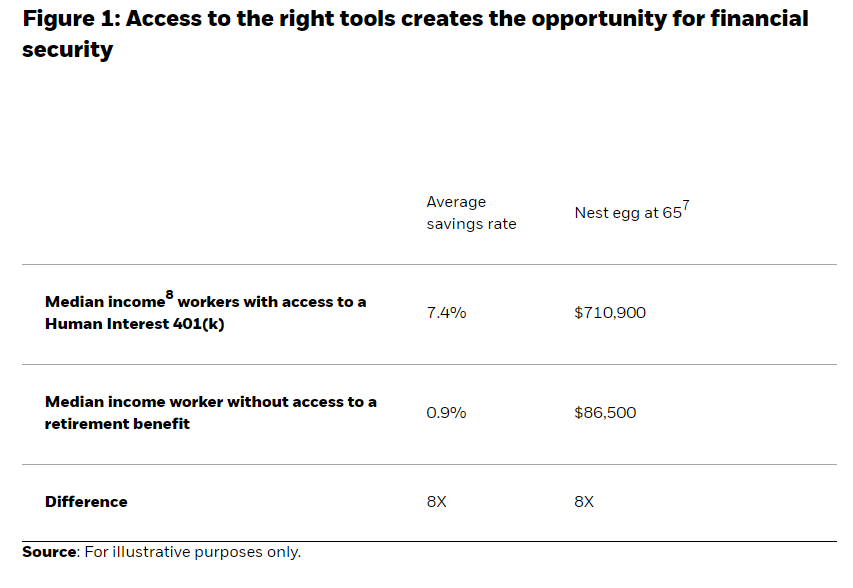

Human Interest data supports this. When workers are provided access to retirement tools, Human Interest has found the rates at which people are saving are higher than may have been previously thought possible - especially among lower income levels. Workers on Human Interest’s platform who are earning less than $60,000 annually save 7.4%4 of their income, compared to 0.9% savings rate5 for those without access to a retirement benefit.

The difference in financial security between workers with and without access to a retirement benefit is stark (Figure 1). With an average savings rate of 7.4% at Human Interest, a median income worker on Human Interest’s platform6 may be able to save $710,900 by the time they reach 65. By contrast, a median income worker without access to a retirement benefit and saving only 0.9% may have a $86,500 nest egg, which is $624,400 (or about eight times) less than their Human Interest counterpart in retirement.

BlackRock’s Emergency Savings Initiative research further finds that bolstering a retirement plan solution with an emergency savings program can amplify results. Across various pilot programs, those with emergency savings were found to be over 70% more likely to contribute to their defined contribution retirement plan.9 Moreover, those with emergency funds were found to be 13 times less likely to take a hardship withdrawal than those with inadequate savings.10 The research on this point is clear: when combined with a retirement solution, emergency savings programs can help people get started and save consistently for retirement.

Beyond providing access to savers, it is also important to make it as easy as possible for an employer to offer a 401(k) plan. Human Interest studied the behaviors of their customers, which are small and medium sized businesses, and built a solution called the Fast Track 401(k)11 that empowers business owners to purchase and launch a plan in 10 minutes or less.

The importance of access to retirement savings vehicles for employers and employees alike cannot be overstated. It is why BlackRock invested in Human Interest earlier this year, and it is why both organizations remain jointly committed to accelerating progress on helping underserved populations save for retirement.

1 BLS data; https://www.bls.gov/news.release/pdf/wkyeng.pdf

2 Federal Reserve, Report on the Economic Well-Being of U.S. Households in 2017, 2018

3 Federal Reserve, Report on the Economic Well-Being of U.S. Households in 2022, 2023

4 As of Q2 2023 on Human Interest platform

5 0.9% Savings Rate calculated by Human Interest based on publicly available data from Fed Survey of Consumer Finances and BEA Personal Savings rate.

6 BLS, 2023

7 Assumes workers begin saving at age 21 with a starting balance of $0 and a constant salary of $60,000 and a 5% assumed growth rate.

8 Median income is defined here as $60,0000 for illustrative purposes. This figure is based on the Bureau of Labor Statistics’ Usual Weekly Earnings of Wage and Salary Workers, Second Quarter 2023 report, which reports that the median weekly earnings of the nation's 121.5 million full-time wage and salary workers were $1,100 in the second quarter of 2023 (not seasonally adjusted). Weekly earnings of $1,100 equate to $57,200 annually.

9 BlackRock, Emergency Savings Initiative Impact and Learnings Report, 2023

10 BlackRock, Emergency Savings Initiative Impact and Learnings Report, 2023

11 See Human Interest website for more information.

This material is provided for educational purposes only and should not be construed as research. The information presented is not a complete analysis of the global retirement landscape. The opinions expressed herein are subject to change at any time due to changes in the market, the economic or regulatory environment or for other reasons.

The material does not constitute investment, legal, tax or other advice and is not to be relied on in making an investment or other decision.

Investing involves risk, including possible loss of principal.

Asset allocation models and diversification do not promise any level of performance or guarantee against loss of principal.

The opinions expressed may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources deemed by BlackRock, Inc. and/or its subsidiaries (together, “BlackRock”) to be reliable. No representation is made that this information is accurate or complete. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

© 2023 BlackRock, Inc. or its affiliates. All Rights Reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© BlackRock

Read more commentaries by BlackRock