Fed’s Quantitative Tightening (Qt) Will Face Constraints

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsABOUT THE AUTHOR

A member of Putnam's Fixed Income team since 2007, Onsel Gulbiten analyzes macroeconomic issues, including inflation, interest rates, and policy developments.

How long will the Federal Reserve continue quantitative tightening (QT)? How large will its balance sheet be when QT ends? These important questions impact financial market liquidity, the anchor of asset values. We assess the likely path of QT in the years ahead.

- The Fed is continuing QT to reduce its large balance sheet, which is currently about twice as large as it was before the Covid pandemic.

- The Fed will try to avoid a market disruption like the money market disfunction and rate spike that occurred in September 2019.

- The composition of the Fed's balance sheet is likely to be a constraint on QT.

Falling bank reserves could disrupt markets

As the Fed pursues QT, it will monitor bank reserve scarcity. When the Fed first started quantitative easing (QE) in 2008, it had initiated an ample reserve system and began paying banks interest on reserves sitting on the Fed's balance sheet. The interest rate on reserves (IOR or IOER) typically acts as the ceiling of the Fed's target policy rate range for federal funds. In order to make sure that short-term rates stay in the desired range, the Fed has another facility, its overnight reverse repo (ON RRP) window, through which the Fed pays interest on overnight deposits. ON RRP is lower than IOR and helps the policy rate stay in the target range.

When bank reserves are abundant, the policy rate stays comfortably in the range. When reserves become scarce, the federal funds rate rises beyond the target range, and disruptions can happen in other money markets.

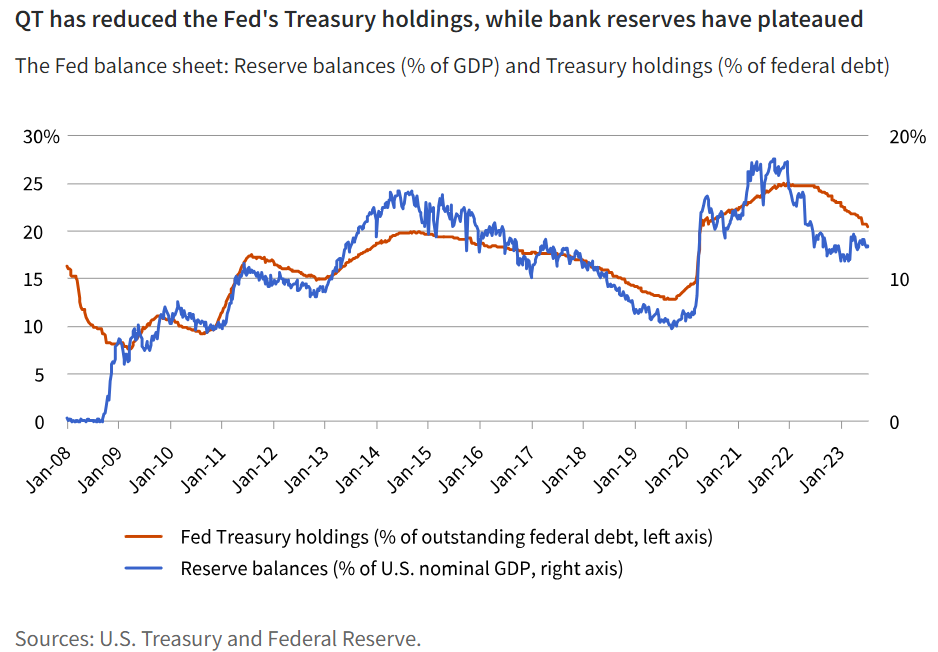

The Fed and market players learned the level of bank reserves that represents scarcity when money market stress arose in September 2019. After just having ended QT a few months earlier, the Fed was compelled by the market stress to start increasing its balance sheet by purchasing T-bills. Based on this experience, the Fed concluded that when reserves decline to 8% as a share of GDP, they become scarce.

Today, reserve balances are about 12% of GDP, which is well over the Fed's 8% threshold. As a result, the Fed and Wall Street analysts have been relying on the 8% number and are comfortable that QT can go on for a long time. Although questions surround it, such as whether comparing bank reserves to bank balance sheets might matter, we use the 8% threshold as a starting point to consider the outlook for QT. Then, we assess whether the Fed's Treasury holdings act as a constraint before reserves become scarce.

Banks' preference for reserves over debt securities may prolong QT

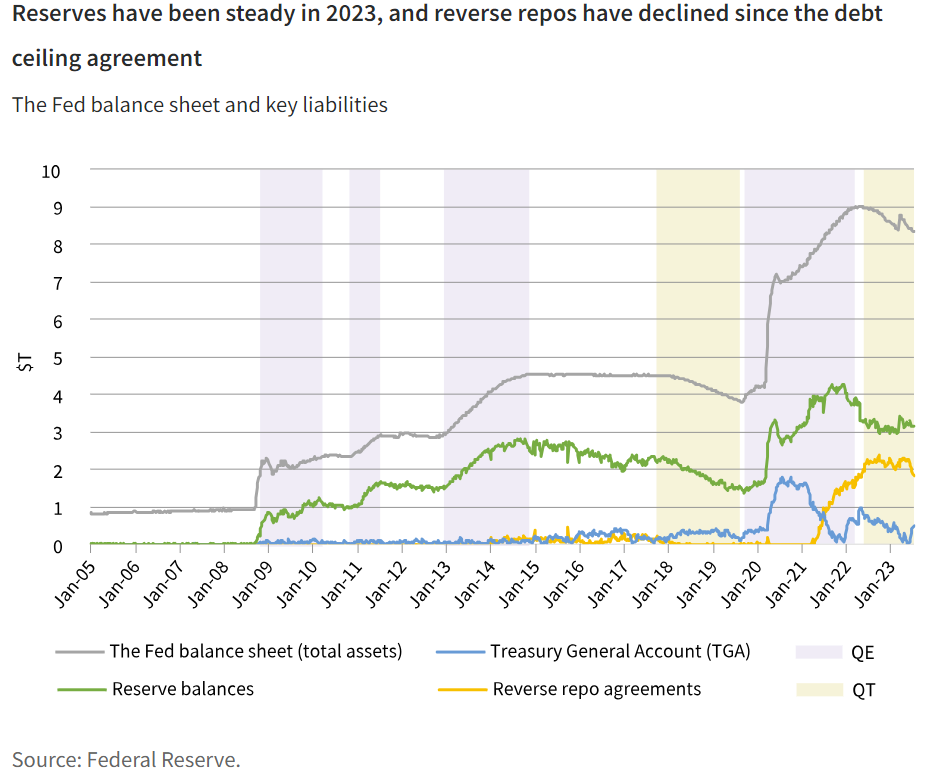

When the 8% threshold will be reached depends on the pace at which reserve balances decline. Bank reserves had been decreasing since the end of 2021 along with the decline in deposits. The historical pattern suggested this would continue after the debt ceiling resolution, with the Treasury increasing its balances at the Treasury General Account (TGA). Typically, the TGA rebuilding has come along with a large drop in reserves. However, the recent behavior of banks' cash assets surprised us. Reserves have risen as banks have been taking the cash from maturing Treasury and mortgage securities and depositing it as reserves to earn the interest the Fed pays, currently 5.40%. Reverse repos have fallen rather than bank reserves. Given the resilient economy and the Fed's fight against inflation, this new reserve-TGA dynamic is likely to continue for a while.

If reserves go down only gradually, reserve balances may not bind quickly. If the decline in the Fed's Treasury and agency MBS holdings continues at its average pace since September 2022, about $75B per month, and if this is mostly matched on the liability side by a decline in reserve repo agreements, the balance sheet can drop for almost two years without damaging bank reserves. Once the domestic reverse repo agreements are close to depletion, if bank reserves continue to decline, it would take another year for them to reach about 8% of GDP. Therefore, at the current pace of QT, the balance sheet reduction can go on for about three more years, and the balance sheet would drop to around $5.6T based on a liability-side-only approach. This would be higher than pre-Covid levels and about 20% of U.S. GDP. Note, the pre-Covid balance sheet was also around 20% of GDP.

The analysis focusing solely on the liability side of the balance sheet suggests QT may go on for another three years. However, back in September 2019, when the Fed had to restart QE, the culprit behind the market disfunction was likely the declining participation of the Fed in the Treasury market rather than reserve scarcity alone. When the Fed's participation in the Treasury market declines, someone else needs to absorb the supply. In September 2019, when the Fed's share in the Treasury market declined to 13%, the market could not absorb the total bond supply. Perhaps when the Fed's ownership declines to 13% of the Treasury market, which was the level in September 2019, stress will emerge. Considering that there is a large Treasury issuance ahead of us, the asset side of the balance sheet might bind before bank reserves become scarce.

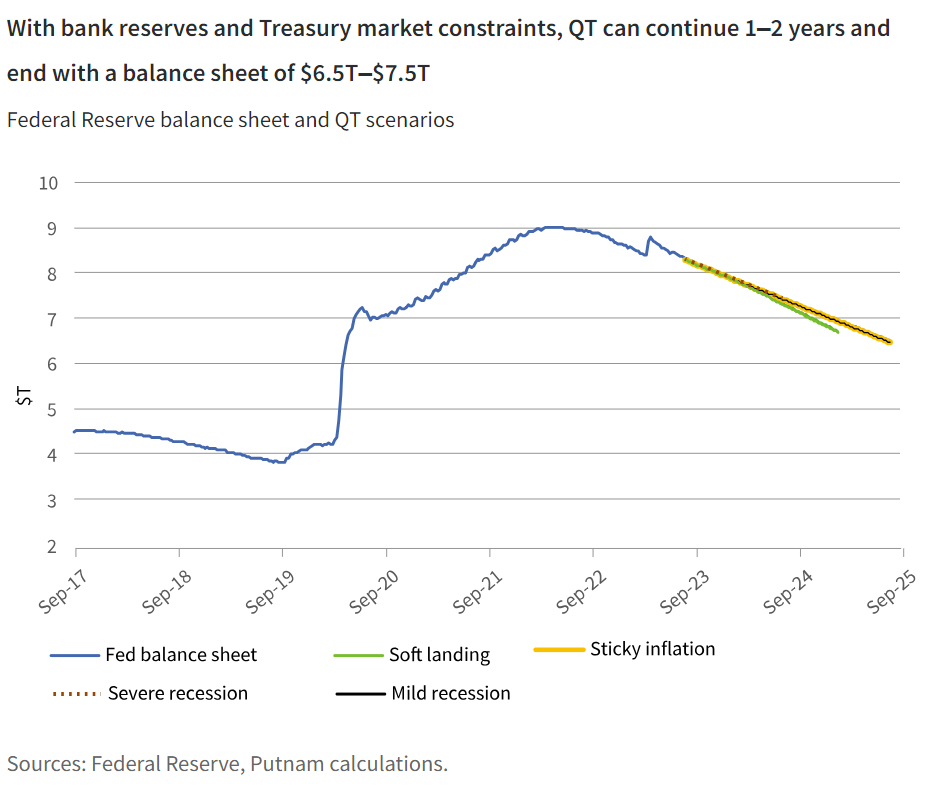

The Congressional Budget Office estimates a more than $1T annual budget deficit for each of the next three years. A $1T net Treasury issuance in public markets this year and next, when the Fed is reducing its Treasury holdings by $60B per month, suggests only two more years of QT. That is, the asset side of the Fed's balance sheet can bind in two years' time, before reserves do, with the final size of the balance sheet being around $6.5T. A disfunction in the Treasury market or another liquid market can cause an unexpected end to the balance sheet normalization.

In the base case scenario of sticky inflation, where inflation declines but stabilizes at around 3.0%–3.5% while the U.S. avoids a recession, QT could last until mid-2025. The Fed would keep the policy rate high for longer, and the yield curve would stay mostly flat or inverted, keeping reserves attractive for banks relative to holding Treasuries or mortgages. While banks would reluctantly reduce their cash balances, a major malfunction in the Treasury or another liquid market would cause QT to end earlier than expected.

Alternative economic scenarios change the timing and size of balance sheet reduction

If a recession arrives, the ultimate size of the balance sheet will likely depend on its severity. (Note, we see a 40% chance of recession in late 2024.)

- In a severe recession, QT would continue until around August 2024 and end with the balance sheet around $7.5T. A severe recession is unlikely, but QT would probably end around the time when the Fed starts cutting the policy rate and before reserve balances start to bind.

- In a mild recession, QT would continue until mid-2025 and end with the balance sheet around $6.5T. The Fed is likely to continue with QT, at least in the early stages of the downturn. If banks' willingness to own Treasuries, agencies, and even MBS rises, and bank reserves decline at the same pace as reverse repo agreements from 2024 on, bank reserves might bind only near the end of 2025. The asset side of the balance sheet, i.e., the Fed's declining Treasury holdings, would bind before that, by the summer of 2025.

If the economy has a soft landing, QT would continue until year-end 2024 and conclude with the balance sheet around $6.7T. If a soft landing allows inflation to come down naturally, the balance sheet reduction might gain some speed once the soft-landing prospects rise during the next 12 months. Commercial banks might begin buying Treasuries ahead of time, reducing cash balances at a faster pace. At the same time, a decline in mortgage rates, when there is no recession, can increase mortgage prepayments. This would accelerate the decline in mortgage securities on the Fed's balance sheet. If the balance sheet shrinkage speeds up to the monthly cap of $95B in 2024, cash balances can decline to 8% of GDP by the end of next year, assuming an equal drain from reserves and reverse repo agreements.

Due to market constraints, QT alone is unlikely to cure inflation

The Fed's ultimate balance sheet will naturally reflect developments in the economy and financial markets. For instance, in the case of a severe recession, the Fed will probably have to maintain a large balance sheet to prevent a deep correction in the money supply, especially if there is severe damage to the credit channel.

A mild recession would have a negative impact on credit creation and is likely to be disinflationary. Two non-recessionary scenarios — soft landing and sticky inflation — are not likely to come with noticeable further declines in broad money supply. However, the Fed would end up with a larger balance sheet than before the 2019–2022 QE period. A large balance sheet, then, begs the question whether inflation will come down sustainably without a recession.

This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This information should not be relied upon as research or investment advice regarding any strategy or security in particular.

This material is prepared for use by institutional investors and investment professionals and is provided for limited purposes. This material is a general communication being provided for informational and educational purposes only. It is not designed to be investment advice or a recommendation of any specific investment product, strategy, or decision, and is not intended to suggest taking or refraining from any course of action. The opinions expressed in this material represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor's particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the material. Predictions, opinions, and other information contained in this material are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

This material or any portion hereof may not be reprinted, sold, or redistributed in whole or in part without the express written consent of Putnam Investments. The information provided relates to Putnam Investments and its affiliates, which include The Putnam Advisory Company, LLC and Putnam Investments Limited®.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Putnam

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All