With government stimulus over, accumulated savings starting to become depleted, rents soaring, and student loans about to switch back on, it appears a credit cycle has begun where borrowers struggle to fulfill their financial commitments.

In the charts below, we identify the overall delinquency rate and then break it out by age cohort. We are focusing on the data series provided by the New York Federal Reserve about loans that are 90+ days late.

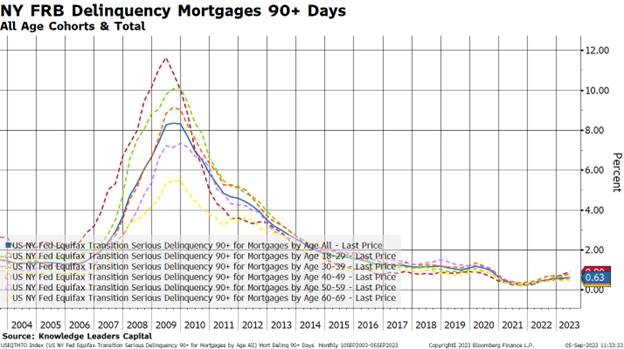

Starting with mortgage loans, the overall delinquency rate is 63bps, near record lows, likely due to the huge home appreciation of the last few years which padded the equity cushion for most homeowners. Even the youngest cohort (18-29 years old) has a delinquency rate only 30bps higher than the aggregate. Unlike the 2007-2011 period, the credit cycle is not playing out in the real estate market.

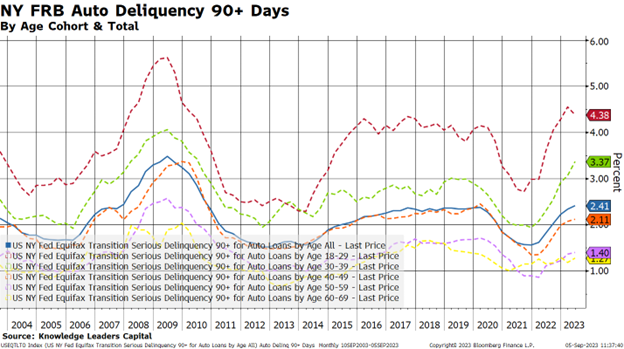

Let’s move on to some forms of consumer loans, where the story is a little more dauting. Auto loans are definitely the epicenter of the credit cycle. While the overall average is a still somewhat tame 2.41%, younger borrowers are not keeping up. Younger borrowers have delinquency rates that are 1-2% higher than the average while the inverse is true for older borrowers. Eighteen-to-thirty-nine year-old borrowers have the highest delinquency rate in 13 years.

Somehow, I sense that used car lots are going to start filling up again as these vehicles get repossessed. This should put downward pressure on used car prices, bringing that element of inflation down. This is one of the channels through which monetary policy works.

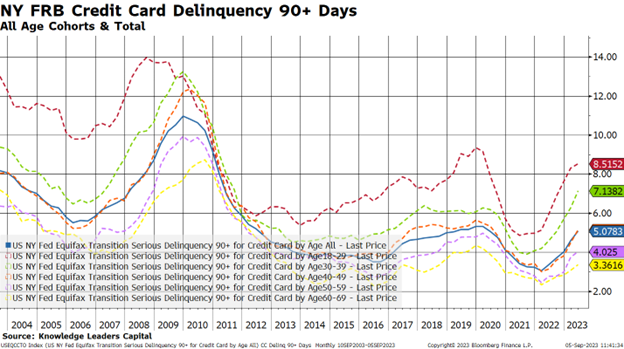

Lastly, I’ll take a look at credit card delinquencies. Here is where we can really see the stresses building. First, the overall delinquency rate has about doubled from 2.5% to 5% over the last couple years. Second, older borrowers have seen a tick up in delinquency rates, a feature we don’t really see in other credit products. Third, one in 12 younger 18-29 year-old borrowers are 90+ days late making their credit card payments.

In conclusion, we are in the early days of a consumer credit cycle. Younger borrowers are the weakest link in this analysis, and this makes me wonder where rates go when student debt payments turn back on at the end of the month.

Disclosures

The information presented here is for informational purposes only and is not to be construed as an offer to sell, or the solicitation of an offer to buy, securities. Some investments are not suitable for all investors, and there can be no assurance that any investment strategy will be successful. Hyperlinks may be included in this message that provide direct access to other internet resources, including web sites. While we believe these links are to reliable sources, Knowledge Leaders Capital (“KLC”) has no control over the accuracy or content of information contained on these sites. Although we make every effort to ensure such links are accurate, up to date and relevant, we have no control over pages maintained by external providers. The views expressed by these external providers on their own web pages or on external sites they link to are not necessarily those of Knowledge Leaders Capital.

The information provided on this blog is for illustrative or example purposes only and should not be construed as KLC’s opinion or investment outlook. As of the most recent quarter end, the named companies may have been held by KLC. For full information including additional policies and full disclosures, please visit our website: KnowledgeLeadersCapital.com.

Any reference to Index performance does not represent the performance of any investment product offered by Knowledge Leaders Capital, LLC. An investor cannot invest directly in an index. The performance of client account may vary from the Index performance. Index returns shown are not reflective of actual investor performance nor do they reflect fees and expenses applicable to investing.

Companies are selected for “Spotlights” based on high levels of innovation activities in their respective industries and illustrate innovation being employed across all sectors and geographies. Spotlight selection is separate from stock selection by the investment team. Spotlights are not necessarily representative of investment opportunities and can be selected regardless of investment performance or inclusion as a KLC holding.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Knowledge Leaders Capital

Read more commentaries by Knowledge Leaders Capital