Why Investors in Retirement May Want to Consider an Income Approach

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAs multi-asset income investors, we seek to help a wide range of clients meet their income needs. The benefits of an income-centric approach are especially relevant for investors as they enter retirement – and that’s especially true today. We bring that to life with two case studies.

Why an income-centric approach matters in retirement: The accumulation vs. decumulation distinction

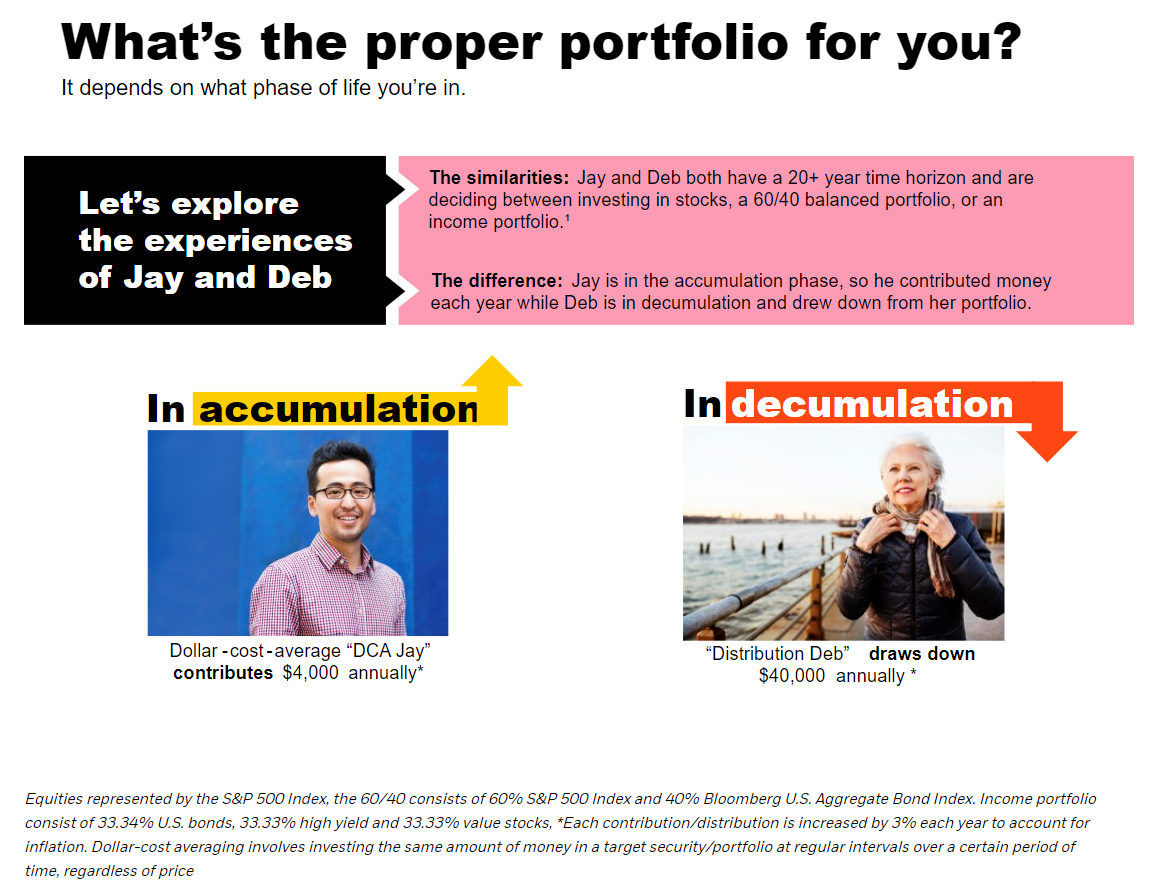

First, meet dollar-cost-average “DCA” Jay. He’s in his early 40s, in the middle innings of his career with another roughly 20 years before retirement. He’s squarely in the ‘accumulation’ phase of his investment journey, contributing regularly to his savings. On the other hand, we have “Distribution Deb,” a recent retiree. Since she is no longer earning a salary, she is relying on income from her investment portfolio to meet her cost-of-living expenses (in addition to income from other sources like social security and an annuity).

Now let’s see what types of portfolios may be appropriate for these two very different life phases:

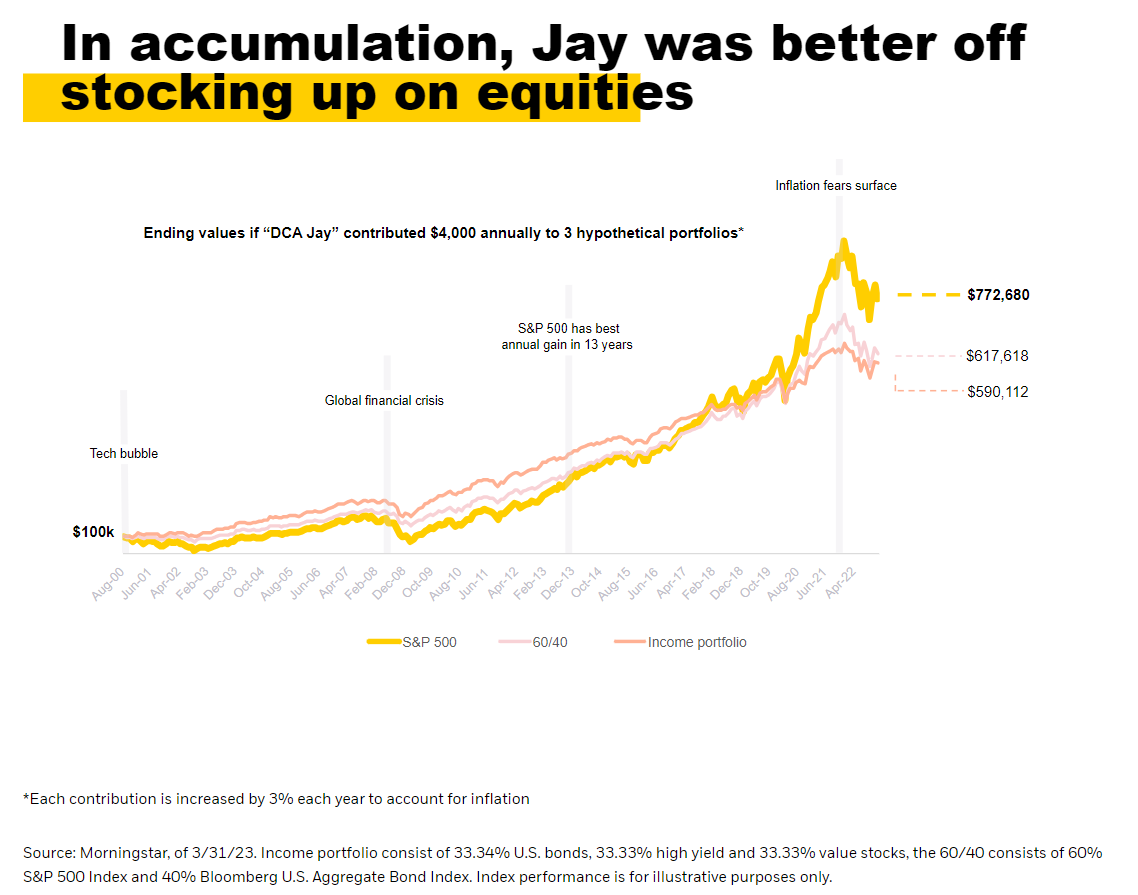

In accumulation, imagine that DCA Jay starts with $100,000 in the year 2000 and he manages to consistently contribute an inflation-adjusted $4,000 annually to his savings over the course of the next 20+ years. Despite weathering multiple storms over this accumulation period, be that the tech bubble, the Global Financial Crisis or Covid, he would have been better off investing in the broad S&P 500 Index compared to a 60/40 balanced portfolio or an income-tilted portfolio (assuming he stayed invested throughout).

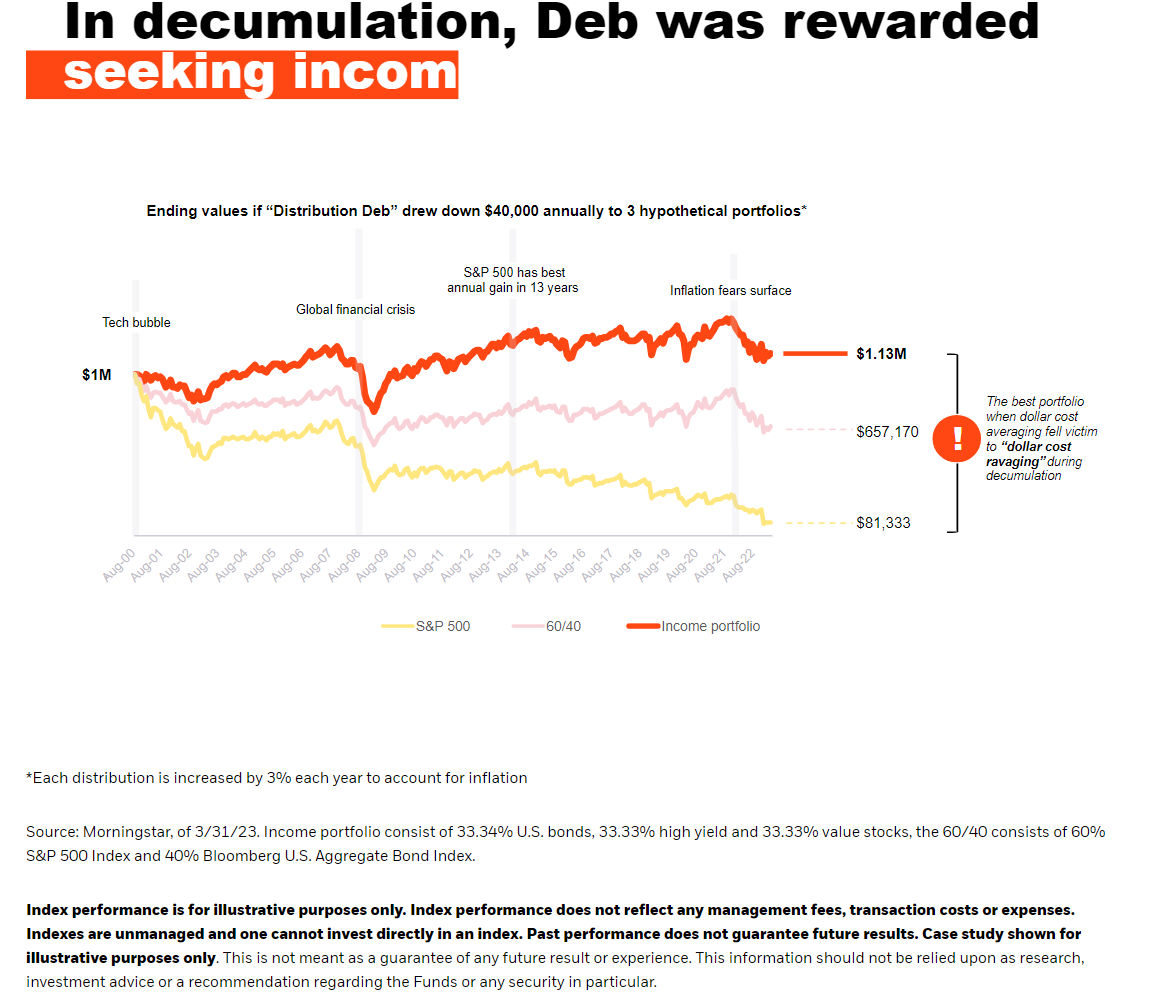

In the decumulation phase, it’s a very different story. Imagine that Distribution Deb has $1 million saved and a $40,000 annual portfolio income need. Starting at the same point in time as DCA Jay, weathering all the same market ups and down, her potential portfolio outcomes are vastly different. Had she invested fully in the S&P 500, her starting portfolio would have lost over 90% of its value. Why? The reason is something we refer to as “sequence of returns risk.” In the early days of Deb’s retirement, markets – and her portfolio – suffered a major downturn with the tech bubble. Nonetheless, Deb still would have needed to meet her distribution needs (which are not met through the relative low yield on the S&P 500 Index), meaning she had to sell a portion of her principal at exactly the time when her portfolio value was down, locking in these financial losses and making it difficult for her portfolio to fully recover as the market rebounded. Instead of dollar cost averaging, she experienced something we call “dollar cost ravaging”.

Fortunately, there is another story for Deb with a much happier outcome. If, instead of investing fully in the S&P 500, Deb had chosen to transition to a diversified income-oriented portfolio when she entered retirement, she would have been able to meet her annual income need primarily from the cash flow generated by the underlying investments, allowing her to leave her principal more intact and to ultimately participate in the market rebound over the coming years. In fact, her ending portfolio value would have actually grown from $1mn to $1.1mn over her decades long retirement, all the while taking $40,000 in distributions each year.

Why does this matter today?

The same sequence of returns risk that we saw impact Distribution Deb in the early 2000s is playing out as we speak. Following a challenging year like 2022 when both equities and fixed income delivered negative returns, Distribution Deb’s savings would have been particularly damaged had she remained invested in a non-income producing portfolio at the time of her retirement. Why? She would have started withdrawing principal when her portfolio value was down, which would have resulted in fewer future units and limited her participation in the market rally year to date 2023.

Bringing it all together: Consider taking a diversified, income-generating approach in the decumulation phase

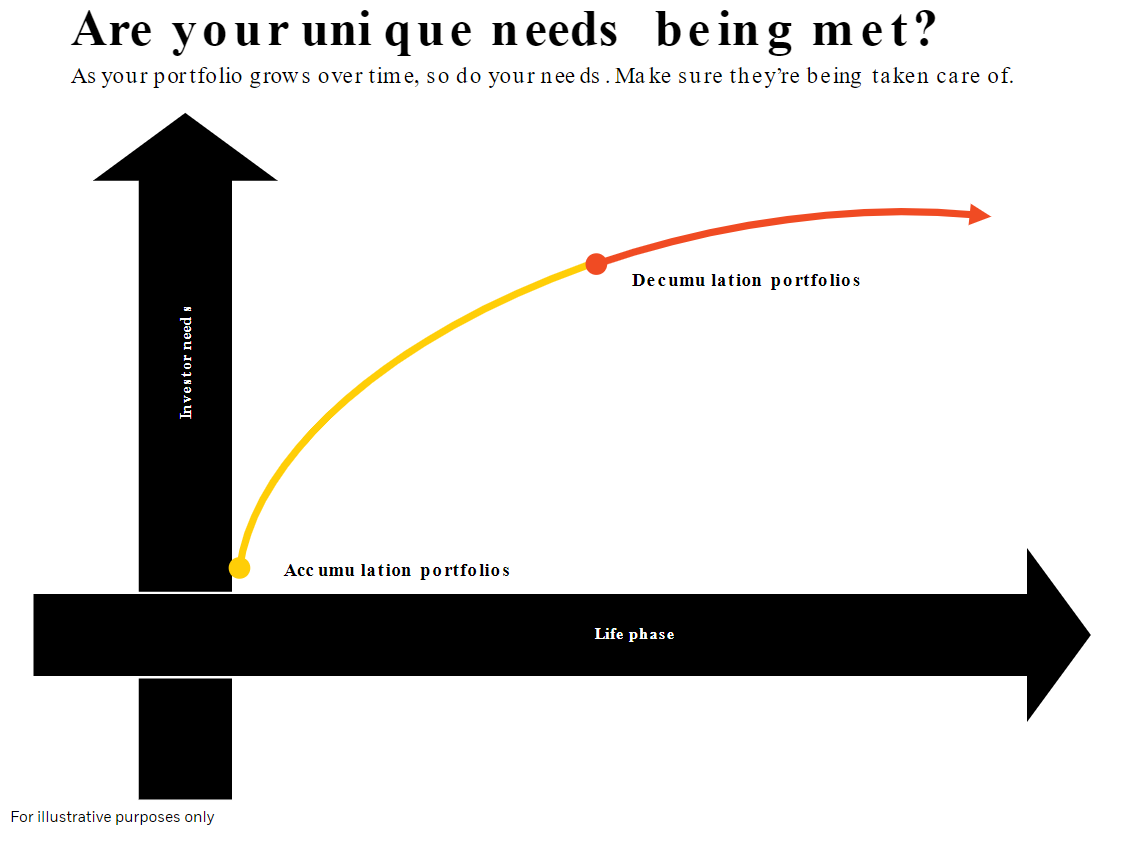

So what does this all mean? As an investor’s life phase progresses, so too should their investment portfolio design. While growth equities and traditional balanced portfolios may very well be a good choice in the accumulation phase, a portfolio rethink is warranted for investors once they reach retirement and start to decumulate.

One way of mitigating this dollar cost ravaging, or sequence of returns risk, is by taking an income-centric approach. The BlackRock Multi-Asset Income Models Portfolios provide a core, diversified option for investors in their decumulation phase, and can be paired with income sources like social security and annuities. These models offer a number of benefits:

- Tap into a broad, diversified universe of income-producing asset classes including dividend stocks, investment grade and high yield bonds, floating rate loans, covered calls and more.

- This diversified approach allows the team to nimbly take advantage of market opportunities, constantly evaluating the income landscape and rebalancing on a quarterly basis.

- A whole portfolio solution available across multiple risk profiles to address the needs of all retirees, ranging from those early in retirement looking for more equity exposure to those focused more on capital preservation.

Disclosure

disclosure: Carefully consider the Funds' investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Funds' prospectuses or, if available, the summary prospectuses which may be obtained by visiting www.iShares.com or www.blackrock.com. Read the prospectus carefully before investing.

Investing involves risks, including possible loss of principal.

This material is provided for educational purposes only and is not intended to constitute “investment advice” or an investment recommendation within the meaning of federal, state, or local law. You are solely responsible for evaluating and acting upon the education and information contained in this material. BlackRock will not be liable for any direct or incidental loss resulting from applying any of the information obtained from these materials or from any other source mentioned. BlackRock does not render any legal, tax or accounting advice and the education and information contained in this material should not be construed as such. Please consult with a qualified professional for these types of advice.

There is no guarantee that any investment will pay dividends.

Index performance is for illustrative purposes only. Index performance does not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results.

The BlackRock model portfolios are provided for illustrative and educational purposes only. The BlackRock model portfolios do not constitute research, are not personalized investment advice or an investment recommendation from BlackRock to any client of a third party financial professional, and are intended for use only by a third party financial professional, with other information, as a resource to help build a portfolio or as an input in the development of investment advice for its own clients. The BlackRock model portfolios themselves are not funds.

BlackRock intends to allocate all or a significant percentage of the BlackRock model portfolios to funds for which it and/or its affiliates serve as investment manager and/or are compensated for services provided to the funds ("BlackRock Affiliated Funds"). Clients will indirectly bear fund expenses relating to assets allocated to funds, including BlackRock Affiliated Funds. BlackRock has an incentive to (a) select BlackRock Affiliated Funds and (b) select BlackRock Affiliated Funds with higher fees over BlackRock Affiliated Funds with lower fees.

Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments. Non-investment-grade debt securities (high-yield/junk bonds) may be subject to greater market fluctuations, risk of default or loss of income and principal than higher-rated securities.

Mortgage-backed securities ("MBS") and commercial mortgage-backed securities ("CMBS") are subject to prepayment and extension risk and therefore react differently to changes in interest rates than other bonds. Small movements in interest rates may quickly and significantly reduce the value of certain mortgage-backed securities.

Prepared by BlackRock Investments, Inc. LLC. Member FINRA

©2023 BlackRock, Inc. or its affiliates. All rights reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All