Checking The Health Of Consumers

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsCredit balances are not the only consumer indicator running high.

My family has just concluded a fantastic summer that included air travel, roller coasters, road trips, new restaurants and no small amount of ice cream. As the school year resumed, I was looking forward to a steadier daily routine as well as a more predictable pattern of our spending. Alas, we’re now shelling out for new backpacks, shoes, sports leagues and school lunches. We are doing our part to prevent a recession.

Consumption has been the core of the post-COVID economic cycle. First, we accrued cash as our usual spending patterns were closed off in 2020. Pandemic stimulus and deferred purchases pushed up excess savings, equipping most households for a stretch of free spending. Our hesitancy to call for a recession hinged on expectations that households would sustain their activity.

A range of reports now show a trend of household assets falling and liabilities rising, leading some to wonder whether consumers are overextended. Overall, we believe households are managing their finances appropriately. In many respects, household balance sheets are getting back to normal. For better or worse, “normal” includes some additional stress for some households.

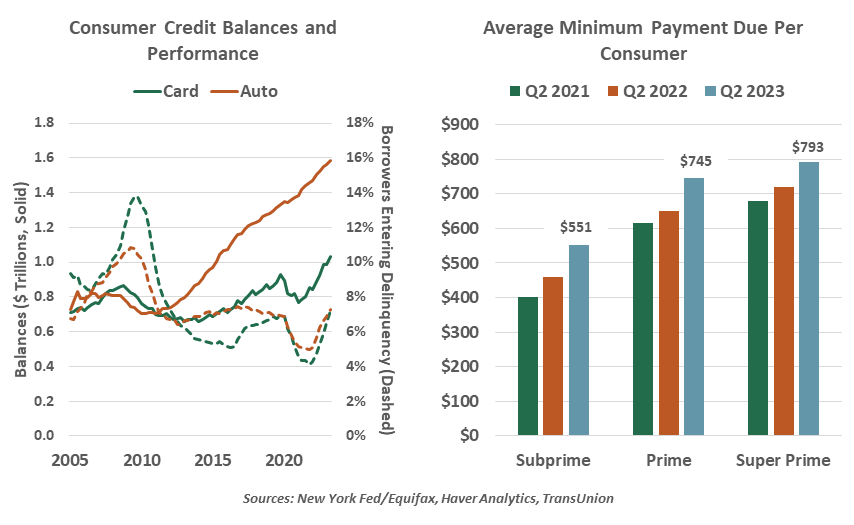

Consumers are indeed making more use of credit across most asset classes. Overall credit growth in the second quarter was muted, but this was driven by a slight decline in mortgage balances, which represent over 70% of consumer debt. Auto, credit card and home equity balances all grew. The average minimum payment due for most borrowers now exceeds $700 per month, a figure that has risen sharply in the past year.

Readers should beware of the fallacy of large numbers. We heard worries when second-quarter credit bureau data showed that U.S. credit card balances exceeded $1 trillion for the first time. Isn’t that too much debt? But the same was said when student and auto loan balances crossed that threshold in the past decade. The level is not meaningful: these figures are reported in nominal dollars, and inflation has done its part to push up balances. On a per-borrower basis, balances are up by about 14% from the second quarter (the same season) of 2019; nominal disposable personal income is up by 22% over the same period. And for credit cards, totals reflect balances of both those who pay off their balances in full each month and those who pay interest on a rolling balance.

Rather than judge debt excesses by levels, we track loan performance to see whether consumers are using credit appropriately. Higher delinquencies reflect distressed borrowers. In this vector, the pandemic had a positive effect. Many people used their stimulus payments responsibly to catch up on debt; delinquencies reached all-time lows in 2021. Now, they are trending up, but so far, only to their pre-pandemic norms. Delinquencies are still well below the strains seen in the 2008 financial crisis.

A few areas do merit some attention. The automotive sector is still dealing with disruptions to inventories and component supplies. Prices of used cars surged as new vehicles were unavailable, while new cars and trucks are only getting more expensive. Car and truck buyers were not deterred by higher prices, and demand stayed strong. The credit bureau TransUnion reported that as of the first quarter, higher prices and interest rates have pushed the average monthly payment to $532 for a used vehicle and $739 for new vehicles, an increase of about 30% from 2020 levels for both loan types.

As we have previously discussed, student loans will be a burden, but we expect they will be manageable. In fact, many borrowers are resuming payments even before they are required in October. Daily reporting by the U.S. Treasury shows that payments to the Department of Education are already approaching their pre-pandemic levels.

Of course, favorable aggregate figures will obscure individual strains. The lowest earners were the first to see their savings depleted and their delinquency rates rise. Subprime (or highest-risk) borrowers are leading the rise in delinquencies, which is an unfortunate symptom of normalcy.

Higher incomes will go a long way toward keeping debts manageable. Since February 2020, average hourly earnings and nominal disposable income have grown by 18%. Over the same interval, core inflation rose a cumulative 13.3%. Employment prospects remain strong, with the unemployment rate holding low and job openings still elevated. Workers are achieving real wage gains, and they are still purchasing, keeping the economy moving. As we enter a steadier state, both inflation and earnings will level off.

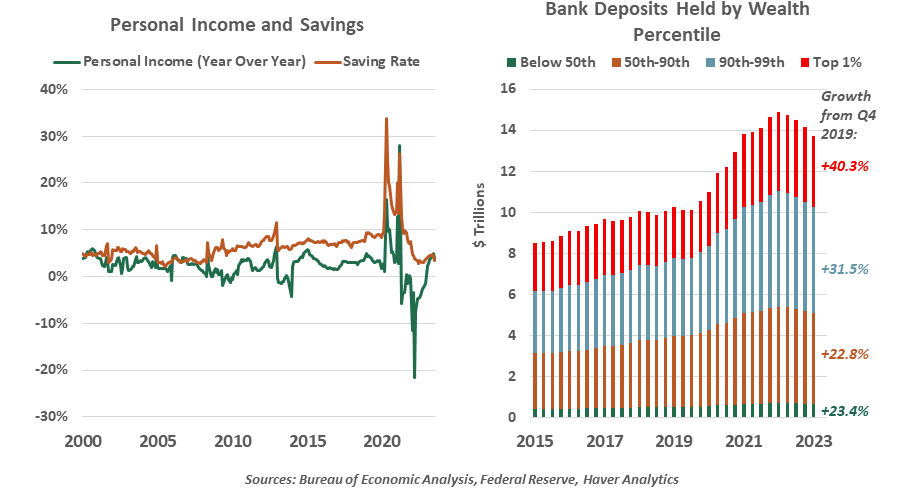

Though the worst of the pandemic is behind us, excess savings are not yet depleted. Saving is simply the remainder of personal income less taxes, consumption and interest payments. When shutdowns were widespread and stimulus was generous, the rate of saving reached a record high of 33.8% in April 2020. Then, at the height of spending and inflation growth last year, the rate fell to 2.7%, approaching the record low set in the housing bubble economy of 2005. Savings have settled into a steady share of income, albeit lower than their pre-pandemic norm.

Consumers are still carrying more cash than before. Bank deposits across all tiers of consumer wealth remain elevated. The cash buffer may help to keep consumers afloat and out of credit distress. Over time, lower inflation should help to make household budgets more predictable and support continued saving.

Just as I paid the last of the summer credit card bills, our household conversations turned to next year’s potential vacations and home renovations. As a result, I have raised my forecast for economic growth in 2024.

Information is not intended to be and should not be construed as an offer, solicitation, or recommendation with respect to any transaction and should not be treated as legal advice, investment advice, or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulations. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All