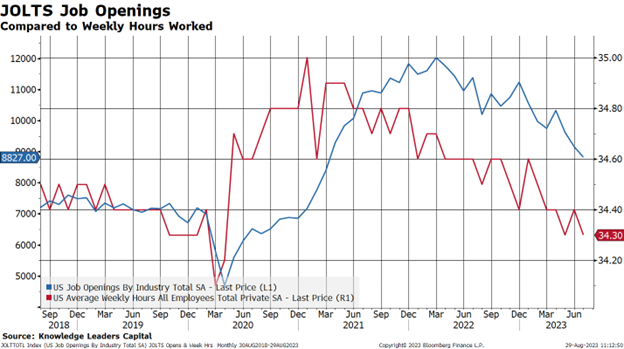

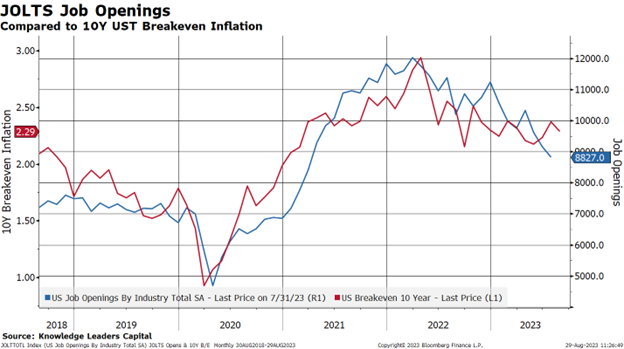

Today the monthly Job Openings and Labor Turnover survey came out for the month of July. Expectations were for 9.5 million job openings, but the actual figure came in at 8.87 million, representing the biggest miss in recent history.

This miss is further evidence that the job market is loosening up a little, taking some pressure off inflation. In the chart below, we can see that weekly hours worked have been falling since January 2021. Roughly a year later, we saw a peak in job openings. Current weekly hours suggest a glide-path down in job openings to the 6 million neighborhood.

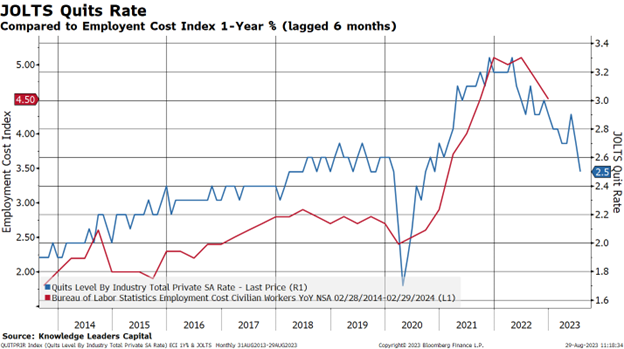

Another way we can illustrate the alleviation of labor pressure that JOLTS job openings suggest is by comparing it to the Employment Cost Index, the best statistic of labor costs because it adjusts for the shift in the mix of jobs (high-paying, low-paying, etc.). We lag the ECI by 6 months as the JOLTS data leads. The current level of job openings are consistent with an ECI 1-year percent change of 3.5% in the quarters to come.

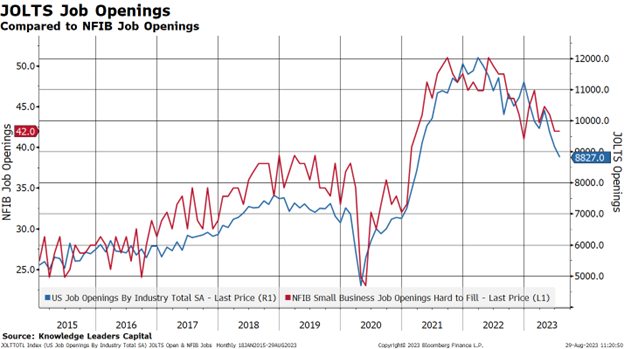

Another perspective is to compare the job openings with the National Federation of Independent Business Jobs Hard to Fill. As one would expect, this is a lagging indicator and it is following the JOLTS job openings down. It is simply becoming easier to fill jobs that are determined to be “hard to fill.”

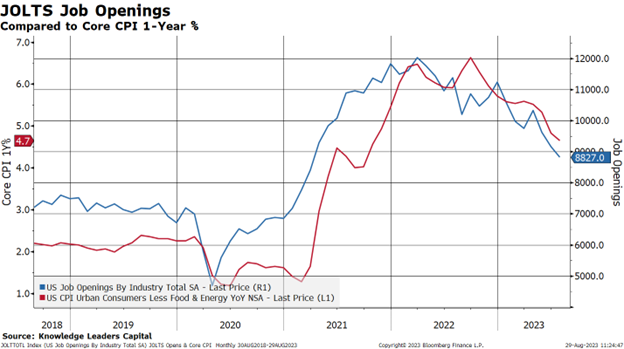

With labor being the component of inflation that has proven to be the most concerning, we can see that as the job market opens up some, it is related to inflation coming down. The core CPI is following the job openings down. If, as mentioned above, the trajectory of job openings is heading to 6 million, this would be consistent with 2% core inflation.

The bond market has a sense of the loosening job market. 10-Year UST Breakeven Inflation is falling in lock-step with job openings.

While the Fed seems to dart around from data point to data point to validate its policy, it is becoming clear that one of the last lagging data points is falling in line. The labor market is easing full stop.

Disclosures

The information presented here is for informational purposes only and is not to be construed as an offer to sell, or the solicitation of an offer to buy securities. Some investments are not suitable for all investors, and there can be no assurance that any investment strategy will be successful. Hyperlinks may be included in this message that provides direct access to other internet resources, including websites. While we believe these links are to reliable sources, Knowledge Leaders Capital (“KLC”) has no control over the accuracy or content of information contained on these sites. Although we make every effort to ensure such links are accurate, up-to-date and relevant, we have no control over pages maintained by external providers. The views expressed by these external providers on their own web pages or on external sites they link to are not necessarily those of Knowledge Leaders Capital.

The information provided on this blog is for illustrative or example purposes only and should not be construed as KLC’s opinion or investment outlook. As of the most recent quarter-end, the named companies may have been held by KLC. For full information including additional policies and full disclosures, please visit our website: KnowledgeLeadersCapital.com.

Any reference to Index performance does not represent the performance of any investment product offered by Knowledge Leaders Capital, LLC. An investor cannot invest directly in an index. The performance of the client account may vary from the Index performance. Index returns shown are not reflective of actual investor performance nor do they reflect fees and expenses applicable to investing.

Companies are selected for “Spotlights” based on high levels of innovation activities in their respective industries and illustrate innovation being employed across all sectors and geographies. Spotlight selection is separate from stock selection by the investment team. Spotlights are not necessarily representative of investment opportunities and can be selected regardless of investment performance or inclusion as a KLC holding.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Knowledge Leaders Capital

Read more commentaries by Knowledge Leaders Capital