Global Economic Outlook: Slow Motion

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe Northern Trust Economics team shares its outlook for major markets in the months ahead.

Despite strong headwinds, the global economy has continued to expand. But an economic divergence has developed. The U.S. and Japan have exhibited unexpected strength; China, which was anticipated to drive global growth this year, is struggling. And Europe is somewhere between these extremes.

With inflation trending down, real incomes are set to turn positive in most economies, which will boost purchasing power. However, loosening labor market conditions could constrain the capacity to splurge. In some countries, the bite of higher interest rates is taking a noticeable toll. The “higher for longer” interest rate environment will result in a sustained period of below-trend growth.

Here are our up-to-date perspectives on how major economies are poised to perform during this year and next.

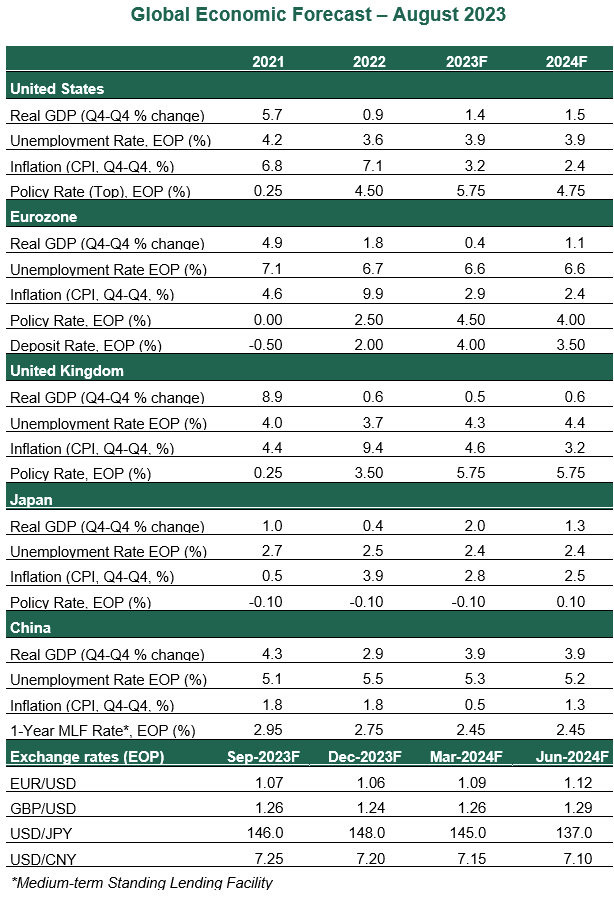

United States

- Inflation and labor market dynamics are in focus, with the Fed nearing the peak of the current tightening cycle. Headline inflation rose 3.2% year over year in July, with the core measure (excluding food and energy) recording its slowest gain in 20 months. While recent inflation readings are much better than the frightening highs seen a year ago, they are still well above the 2% target. The tight labor market and strong economic activity underpin our soft landing narrative, but they also add to inflation risk.

- After taking a breather in June, the Federal Open Market Committee raised the Fed Funds target rate to a range of 5.25-5.50% last month. The hike was well-signaled, but neither the accompanying statement nor the press release offered any hints as to the next steps. Still-elevated core inflation calls for one more hike next month, followed by a prolonged hold through the first half of 2024.

Eurozone

- The eurozone exited its winter recession, with the economy expanding 0.3% in the second quarter, but the figure was distorted by a rebound in Ireland. Excluding Ireland, real gross domestic product (GDP) grew 0.1% in the first and second quarters of 2023 as the German economy stagnated. Grim readings from August’s Purchasing Managers’ Indexes have raised the odds of a contraction in the third quarter. However, real incomes are set to turn positive, which should underpin consumption.

- Headline disinflation is underway, thanks to stable energy prices. But inflation’s core is proving to be more persistent than expected, rising 5.5% year over year in July. Employment data shows the labor market is loosening, with 350,000 jobs added in the second quarter, down from the 900,000 added in the first three months of 2023. This will exert downward pressure on wages. The European Central Bank raised policy rates by 25 basis points in July, but forward guidance was vague, similar to that of the Fed. We see one more hike in the deposit rate to 4%, after which it will remain there for at least the following three quarters.

United Kingdom

- The British economy has shown remarkable resilience in the face of persistent hardships. GDP growth surprised to the upside in the second quarter. Given the drags from sticky inflation and the lagged passthrough of tighter monetary policy, the recovery is unlikely to sustain momentum. A prolonged period of sluggish growth is expected.

- The Bank of England (BoE) raised its interest rate again in August, to a new 15-year high of 5.25%. Yet core inflation hasn’t improved at all and is the highest among major advanced economies. The labor market is loosening, but the growing slack hasn’t dented wages, which are growing at a record pace. Given the focus on wages, we see little reason for the BoE to conclude its tightening cycle. Two more hikes of 25 basis points each are likely at upcoming meetings.

Japan

- The Japanese economy grew at an annualized rate of 6% in the second quarter, marking the strongest growth since the last quarter of 2020. A surge in net exports was the main driver, as imports fell due to fading pent-up domestic demand. But recent gains in exports are unlikely to be sustained, given the slowing global economy.

- The Bank of Japan (BoJ), at its July meeting, surprised markets by raising the 0.5% cap on its yield curve control (YCC) policy to 1.0%. The move was aimed at enhancing the sustainability of the policy, rather than tightening it. Given recent developments in wage and consumer price inflation, we believe further policy revisions are in store. The termination of YCC later this year and a pivot to monetary tightening in the second half of 2024 is our base case.

China

- As we wrote here, bad news is piling up for China’s economy. The economic decoupling of China from the West is starting to gather pace. Foreign investments are drying up. Consumption is not taking off amid lingering property sector woes, tipping consumer prices into deflationary territory last month. And a major Chinese trust firm missed payments on investment products, adding to concerns that the economic slowdown may trigger a liquidity crisis beyond the real estate sector.

- These developments have prompted Beijing to deploy more policy support. However, the measures will neither solve all of their problems nor revive the property sector. Nevertheless, more policy support will be delivered, but the scope for a massive stimulus or devaluation of the currency to boost exports is narrow.

Information is not intended to be and should not be construed as an offer, solicitation, or recommendation with respect to any transaction and should not be treated as legal advice, investment advice, or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulations. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All