China's economy may have spillover effects on global economic and earnings growth, but it's unlikely to lead to global financial contagion and send stock markets materially lower.

China is having a tough year. In contrast to post-lockdown pent-up demand driving solid and steady economic growth this year, a surge in the first quarter was followed by a stall in the second. Our analysis of China's national data shows a country mired in deflation, plunging exports, youth unemployment climbing above 20%, a consumer pullback and an unstable property sector leaving developers to miss bond payments and a trust company to fail to repay investors.

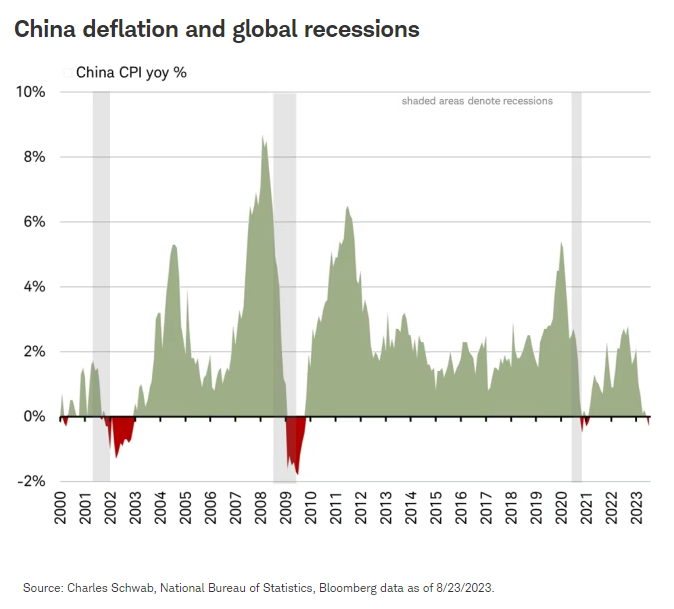

A stalled economy and concerns about a property market crash have reinvigorated questions about the impact of China's slowdown on the rest of the world. The world's second-largest economy has typically been closely tied to global demand. Historically, China's inflation has dipped into negative territory only around global recessions (2001, 2008-09 and 2020), as you can see in the chart below. Although China's consumer price index (CPI) has once more moved negative, we don't believe a "Lehman moment" involving a housing crash and global financial contagion is a likely outcome. We do expect lingering slow growth in China and potential spillover effects on global economic and earnings growth.

What happened?

Although official statistics from the People's Republic of China report the real estate sector directly accounted for 7% of GDP in 2020, the growth in activity across the many industries driven by property activities is estimated to contribute as much as 29% of GDP, according to a research paper published in August 2020 by Harvard Professor of Public Policy and Economics Kenneth Rogoff and International Monetary Fund economist Yancheng Yang. To curb speculation and the buildup of leverage, the government's "three red lines" were created in 2020. The criteria of property developers specified a 70% limit on the ratio of liabilities to assets, a 100% limit on the net leverage ratio, and a minimum coefficient of 1 in the liquidity ratio for property developers. By 2021, most developers were able to comply with these restrictions. But some, like Evergrande and Country Garden, have struggled.

Although the Chinese government sought to curb what it saw as overinvestment, the pendulum has swung to the other extreme. Developers seem to be starved of capital both in terms of debt issuance and cashflows from new property sales. Chinese homebuyers make down payments years before delivery of completed units, and concerns about losing down payments and making mortgage payments on properties not yet built have increased.

Because property comprises about 70% of wealth for Chinese households (according to analysis of data from China's National Bureau of Statistics), worries about the housing market have seemed to erode consumer confidence and the pace of spending on goods. This weakening has also reduced land sales revenues for local governments and may have contributed to a trust company missing payments to investors on some investment products.

Contagion?

Echoes of the U.S. subprime housing-led global financial crisis of 2008-09 have spooked investors. But, despite real estate loans accounting for over 25% of total loans issued in 2020, there are some mitigating factors that make a financial crisis and contagion within and beyond China unlikely. China's smaller banks may number about 4,000, but the overall financial sector is dominated by fewer than 20 big, government-owned banks, which are solidly capitalized and tightly regulated. Encouraged to increase spending to stimulate the slowing economy, local government officials are quietly bailing out many smaller local banks with real estate exposure (according to various media sources), issuing bonds and investing the proceeds into the banks. This effectively transfers bank problems onto the government's much healthier balance sheet.

Financial crises often result from the use of excessive leverage. But, unlike in the U.S. where NINJA (no income, no job, no assets) no-money-down loans become commonplace, leading up to the 2008-09 housing crash, the use of leverage by homebuyers in China has been low. In fact, until recently, 30-50% down payments were required and buyers often paid all in cash. The lack of excessive leverage could be a major mitigating factor when it comes to financial contagion from China's real estate downturn.

Markets have already priced in enormous losses stemming from the funding problems afflicting China's property developers; indexes for the developer stocks and high-yield bonds traded in Hong Kong are down over 90% from their highs in early 2021. Although the price of Country Garden's bonds that mature in 2026 is trading at just 8 cents on the dollar, other high-yield bonds from Bank of Communications (BOCOM) and Industrial and Commercial Bank of China (ICBCAS), the two largest issues in the China High Yield Bond Index, are trading near par. This suggests that markets do not expect Country Garden to get bailed out nor its probable failure to cause contagion even among other junk bond issuers or banks.

Offsets

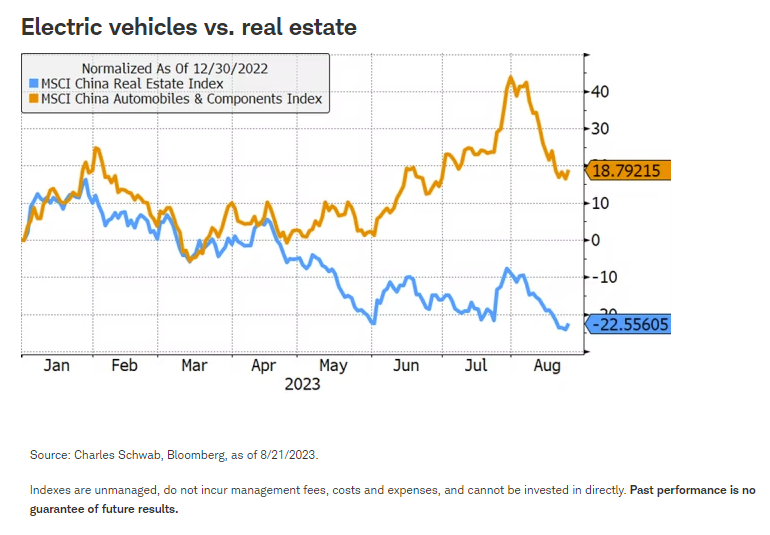

While we do not believe that it's likely to cause a contagion that spreads across China and ripples across the rest of the world, the property market downturn is a drag on China's economic growth. There are also increasing offsets to this drag. Parts of China's economy are doing well with investment and exports in electric vehicles, solar and wind power and batteries growing at double-digit rates. Rather than encourage investment back into property, the government is devoting resources to foster high-tech growth, issuing bonds to fund renewable energy infrastructure on a scale unmatched anywhere in the world. Beijing estimates those green manufacturing sectors or "the new economy"—plus other high-tech areas like semiconductors—grew 6.5% from a year ago in the first half of 2023 and accounted for approximately 17% of GDP. By contrast, real estate construction spending slumped almost 8% in the first half and the property sector provides about 20% of GDP. It isn't a complete offset, but it could make a difference in the diversity and quality of China's growth. This divergence can be seen in the stock performance of electric vehicle makers (+19%) and real estate developers this year (-23%).

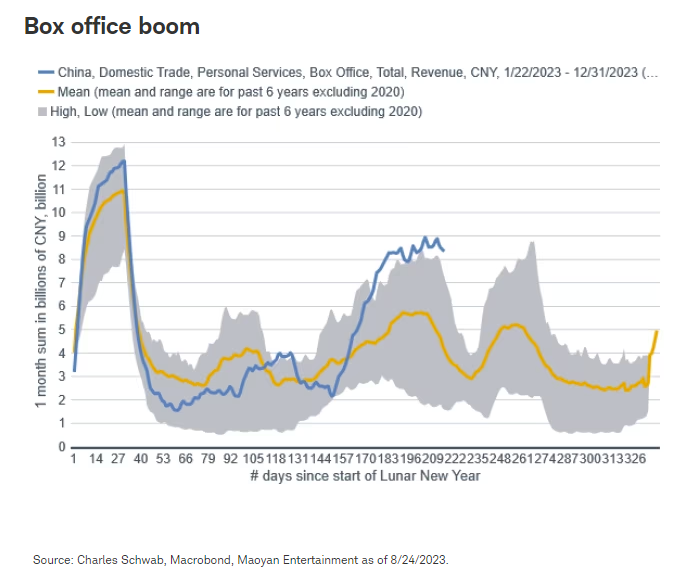

Additionally, with the emergence of zero-COVID lockdowns, consumer spending on domestic travel is now exceeding pre-pandemic levels by 15% and the summer movie box office revenues have set multi-year highs. This service sector improvement can also help offset slower spending on manufactured goods.

Stimulus

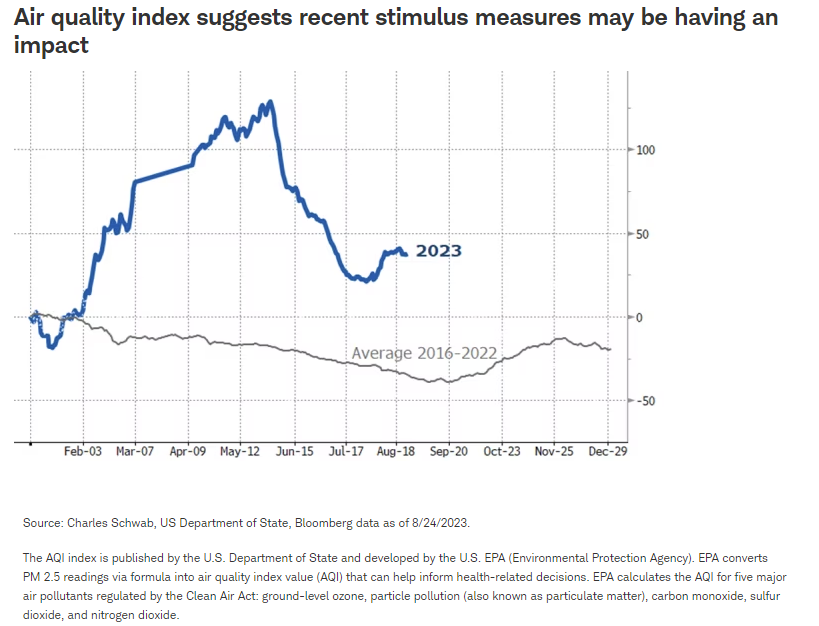

China's government has been slow to invoke aggressive stimulus to boost growth, fearing the costly and inflationary response that occurred across Western economies when record stimulus followed pandemic lockdowns. China's incremental and ongoing announcements of more modest measures have disappointed investors and pundits calling for larger and broader stimulus. Yet, there are signs that China's approach seems to be having some success. Air pollution, measured by U.S. consulates in China, offers a real-time measure of manufacturing and travel in the country—pollution rises along with economic activity. In recent weeks, air quality in China's capital worsened as new stimulus measures were enacted after the July politburo meeting, reversing some of the decline in emissions during the second quarter as the economy stalled.

Global Impact

China's slowdown spilling over to the U.S. and other countries may be a risk but is unlikely to be a major driver of weakness in economic or earnings growth.

- Many companies rely on sales to Chinese consumers. According to recent company filings, Qualcomm gets two-thirds of its revenue from China, General Motors gets nearly half, while Tesla gets about a quarter, as does Sketchers. Yet, sales to China account for only 4-8% of business for all listed companies in America, Europe, and Japan, which could limit any fallout.

- Overall exports to China from the U.S., United Kingdom, France, and Spain contribute to approximately 1-2% of their respective economies. Even for export-driven Germany, with exposure of nearly 4%, China imports would have to collapse to generate a sizeable hit to the German economy.

- Commodity exporters are uniquely exposed to China's slowdown, especially in building materials. The country is the world's biggest user of cement and consumes about half of the world's iron ore, refined copper, nickel, zinc, and almost a fifth of the world's oil. On August 22, BHP, the world's biggest miner, reported the lowest annual profit for the Australian firm since the pandemic shutdowns of three years ago, attributed to China's slowdown.

Investing implications

China's stock market makes up 30% of the MSCI Emerging Market (EM) Index, so its swings tend to drive overall EM stocks. While the risk of a crisis can't entirely be ruled out, our base case is that China's policymakers will continue with their modest and incremental approach to stimulus, and aid to banks and the property market, avoiding a crisis but resulting in relatively sluggish overall economic growth and consumer spending on goods. Chinese stocks seem to be pricing in lingering weakness with stocks trading below their 20-year average price-to-earnings ratio. If China responds with more aggressive stimulus, it could spark a rally, especially if the efforts begin to reflect improvement in more traditional economic data.

Recent rallies in China's stock market have been short and sharp. China's stocks rallied 60% from their low in October 2022 on signals the economy may reopen, and peaked on January 27 of this year; the rally ended as a Chinese balloon entered North American airspace, reigniting geopolitical tensions. Tensions have subsequently cooled after more high-level meetings between U.S. and Chinese officials took place over the summer, including U.S. Commerce Secretary Raimondo's visit this week. The often sudden price movements in emerging market (EM) stocks contribute to traditionally small weightings in most portfolios. But China's impact as the world's second-largest economy means the impact of China's slowdown may be felt beyond the EM share of portfolios. Fortunately, we believe China's troubles are unlikely to lead to a global financial contagion that would materially send stock markets lower and deepen economic downturns in other major countries.

Michelle Gibley, CFA®, Director of International Research, and Heather O'Leary, Senior Global Investment Research Analyst, contributed to this report.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Please note that this content was created as of the specific date indicated and reflects the author's views as of that date. It will be kept solely for historical purposes, and the author's opinions may change, without notice, in reaction to shifting economic, business, and other conditions.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results.

Investing involves risk including loss of principal.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets.

Investing in emerging markets may accentuate this risk.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income, small capitalization securities and commodities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors.

Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

Commodity-related products carry a high level of risk and are not suitable for all investors. Commodity-related products may be extremely volatile, and illiquid and can be significantly affected by underlying commodity prices, world events, import controls, worldwide competition, government regulations, and economic conditions.

The policy analysis provided by Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes please see schwab.com/indexdefinitions.

The MSCI China Index captures large and mid-cap representation across China A shares, H shares, B shares, Red chips, P chips and foreign listings (e.g. ADRs) covering about 85% of the China equity universe.

The MSCI China Real Estate Index is designed to capture the large- and mid-capitalization segments of securities included in the MSCI China Index that are classified in the Real Estate Sector as per the Global Industry Classification Standard (GICS®).

The MSCI China Automobiles and Components Index is designed to capture the large- and mid-capitalization segments of securities included in the MSCI China Index that are classified in the Automobiles and Components industry group (within the Consumer Discretionary sector) according to the Global Industry Classification Standard (GICS®).

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Charles Schwab

Read more commentaries by Charles Schwab