Quick read

- Monetary and fiscal policy are typically thought of as independent tools that central banks and governments use to manage the economy. However, elevated levels of government indebtedness in the post-quantitative easing (QE) world mean there is a more challenging trade-off between price stability (i.e., managing inflation) and fiscal sustainability (i.e., managing government debt).

- Compared to other developed market central banks, the Federal Reserve is in a relatively privileged position as it can generate operating losses without needing a government recapitalization. An underappreciated cost of this legal set-up is that monetary policy in the US may remain looser compared with other countries (and likely looser than intended).

- In our tactical multi-asset portfolios like the BlackRock Tactical Opportunities Fund, the prospect of greater fiscal dominance over monetary policy leads us to be short long-dated government bonds and short the US dollar.

The economic importance of fiscal policy has grown since the start of the pandemic and at this juncture, there are no easy choices for central bankers. Elevated levels of government indebtedness and large central bank balance sheets create a direct trade-off between price stability (which requires interest rates above economic growth rates) and fiscal sustainability (which requires economic growth rates above interest rates). The pursuit of price stability through monetary tightening harms central bank profitability increases government interest expense, and may result in higher overall debt issuance. Alternatively, the prioritization of debt sustainability through a central bank-sponsored overshoot of nominal GDP growth may put price stability at risk. We view this as a situation where the relative independence of monetary and fiscal policies has diminished.

Fiscal dominance

Strategic government spending initiatives – most notably the US IRA and CHIPS Act that we discussed in Guns and Butter 2.0 – further complicate the policy tradeoffs. Since these fiscal programs directly target interest rate-sensitive sectors (like construction), they can directly offset monetary tightening. In the US, fiscal stimulus appears to be dominating the monetary tightening that was meant to slow growth in pursuit of price stability. As other countries have already begun to mimic the US industrial growth policies, we should expect fiscal policies to offset monetary tightening in other regions of the world in the coming years as well.

Feeling QuEasy

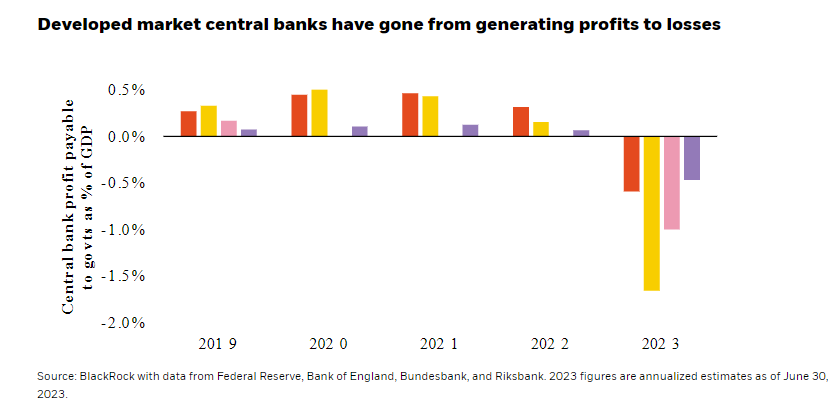

Central banks purchased large amounts of government bonds in response to the last two recessions and have been slow to unwind fixed coupon bond holdings. Though there have been academic discussions on how large balance sheets would intersect with normalization of policy rates, we have now reached that reality and central banks find themselves generating large operating losses. The transfer of these capital losses to governments leaves central banks politically exposed. The current deterioration of government finances during a robust economic expansion with above-target inflation likely means that both monetary and fiscal policy will face greater constraints during the next downturn.

Central bank profitability matters

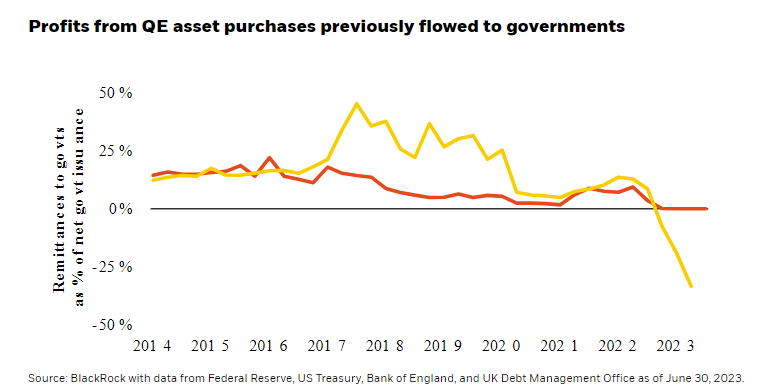

Before this year, central banks were incredibly profitable institutions that bolstered government finances. Profits from QE asset purchases flowed to treasuries and resulted in less issuance than would have otherwise been needed to finance government spending. The chart below shows the remittance of the Fed and Bank of England (BoE) to national treasuries as a fraction of government issuance. The numbers are not small: in 2021, for example, the Fed transferred $109bn to the US Treasury. There have been periods when BoE payments to the UK Treasury amounted to over 40% of net issuance and Fed transfers sometimes amounted to more than 20% of total US issuance. These transfers have lowered the overall supply of government bonds and eased the burden on taxpayers. The chart also illustrates, however, how this dynamic has changed as central banks have normalized policy rates.

Exorbitant privilege 2.0: the ability to defer central bank losses

As remittances have ended across developed market central banks, governments must issue more bonds to finance the same amount of spending. For countries that have an indemnity agreement in their central bank charter, the impact is even greater and more immediate. The governments in the UK, New Zealand, and soon Sweden must transfer meaningful sums to recapitalize the negative equity position of their central banks.1 In the UK, this has contributed to the turmoil in debt markets as BoE losses look set to add 30% to UK Gilt debt issuance this year.

Relative to other central banks, the Fed charter provides it with greater latitude. That is because it can manage operational losses by using a special balance sheet item known as a ‘Deferred Asset’.2 This means that additional US debt issuance from QE losses will likely be backloaded compared to other countries.3 However, the use of an accounting item to delay the recognition of losses does result in some policymaking challenges; it means that the Fed is effectively expanding the monetary base despite trying to slow the economy.4 We anticipate that institutional differences across developed market central banks are likely to lead to dispersion in policy and relative government bond supply across countries in the coming years.5

Fragility of monetary independence

Monetary and fiscal policy are typically thought of as independent tools that central banks and governments use to manage the economy. However, the current magnitude of losses associated with past central bank policy choices has substantial and direct fiscal implications. This raises the unwelcome prospect of increasing fiscal dominance over monetary policy through indirect channels (like political rhetoric) and more direct channels (like potential changes in legislation around central bank statutes). This potential political by-product of QE was a topic raised by Chris Sims in his 2016 Jackson Hole speech:

"The fiscal impact of central bank balance sheet gains and losses are, even with the current levels of expanded balance sheets, modest compared to the fiscal impact that will arise if interest rates rise to normal levels. But once they are large enough to generate public discussion, the balance sheet fluctuations are likely to be seen as more directly attributable to the central bank itself. Drastic drops in seigniorage flows, or even a requirement for substantial capital injections to the central bank from the treasury, could arise. They might mistakenly, or cynically, be portrayed as due to central bank mismanagement. And indeed they would represent the central bank’s taking on risk and thereby making important fiscal decisions. A legislature that realizes belatedly that this has happened may legitimately question whether the central bank has exceeded its mandate."

In our tactical multi-asset portfolios like the BlackRock Tactical Opportunities Fund, we seek to deliver diversifying returns that are lowly correlated with stock and bond markets. We do so primarily by seeking out relative value opportunities across different countries. Our insights on the fiscal-monetary trade-off have led us to be short government bonds across developed markets, notably in the UK and Sweden given the large recapitalization costs associated with QE losses. We are also short US dollar vs. currencies of countries like Australia, Canada, and the Eurozone that have been more fiscally prudent.

1 The UK Treasury has paid the BoE nearly £15bn since Q4 2022 (source: UK Office for National Statistics); the New Zealand government has paid the RBNZ over NZD$3 bn starting Q2 2022 (source: RBNZ). The Swedish Riksbank is subject to new legislation that requires it to request a recapitalization in early 2024, which could exceed SEK60bn (source: Riksbank). The Bank of Canada is indemnified against losses it may realize on selling its QE portfolio but so far no losses have been crystallized as bonds are being held to maturity.

2 Additionally, the Fed, unlike some peers, does not need to recognize mark-to-market losses on its bond portfolio as a write-down on its income statement. This lowers reported losses compared to other central banks.

3 In other countries that recognize the unrealized mark-to-market losses as a current fiscal cost, the central bank is likely to return to profitability relatively earlier as the value of bonds rises closer to maturity.

4 It is notable that the Fed is the only developed market central bank with a base money supply that is larger now compared with the start of 2023.

5 Unlike the Fed, the Bundesbank is opting to run down its substantial store of provisions and reserves (over EUR190bn as of June 2023, source: Bundesbank) before it decides to ‘carry forward’ losses as the Fed is doing. Recent decisions by the European Central Bank and the Bundesbank to reduce the interest paid on minimum reserves and on government deposits, respectively, will help reduce net interest expense and suggest European policymakers are acutely attuned to its operating losses.

Carefully consider the investment objectives, risks, charges and expenses of the fund carefully before investing. The prospectus and summary prospectus contain this and other information about the fund and are available, along with information on other BlackRock funds, by calling 800-882-0052 or at blackrock.com. The prospectus and, if available, the summary prospectus should be read carefully before investing.

Performance data quoted represents past performance and is no guarantee of future results. Investment returns and principal values may fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. All returns assume reinvestment of dividends and capital gains. Current performance may be lower or higher than that shown. Refer to blackrock.com for the most recent month-end performance.

To obtain more information on the fund, including the Morningstar time period ratings and standardized average annual total returns as of the most recent calendar quarter and current month-end, please visit Tactical Opportunities Fund.

The Morningstar RatingTM for funds, or "star rating," is calculated for managed products (including mutual funds, variable annuity and variable life subaccounts, exchange-traded funds, closed-end funds, and separate accounts) with at least a three-year history. Exchange-traded funds and open-ended mutual funds are considered a single population for comparative purposes. It is calculated based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a managed product's monthly excess performance, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of products in each product category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars, and the bottom 10% receive 1 star. The Overall Morningstar Rating for a managed product is derived from a weighted average of the performance figures associated with its three-, five-, and 10-year (if applicable) Morningstar Rating metrics. The weights are 100% three-year rating for 36-59 months of total returns, 60% five-year rating/40% three-year rating for 60-119 months of total returns, and 50% 10-year rating/30% five-year rating/20% three-year rating for 120 or more months of total returns. While the 10-year overall star rating formula seems to give the most weight to the 10-year period, the most recent three-year period actually has the greatest impact because it is included in all three rating periods.

Important risks: The fund is actively managed and its characteristics will vary. Stock and bond values fluctuate in price so the value of your investment can go down depending on market conditions. International investing involves special risks including, but not limited to political risks, currency fluctuations, illiquidity and volatility. These risks may be heightened for investments in emerging markets. Fixed income risks include interest rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Asset allocation strategies do not assure a profit and do not protect against loss. The fund may use derivatives to hedge its investments or to seek to enhance returns. Derivatives entail risks relating to liquidity, leverage, and credit that may reduce returns and increase volatility.

This information should not be relied upon as research, investment advice, or a recommendation regarding any products, strategies, or any security in particular. This material is strictly for illustrative, educational, or informational purposes and is subject to change.

Prepared by BlackRock Investments, Inc. LLC. Member FINRA

©2023 BlackRock, Inc. or its affiliates. All rights reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© BlackRock

Read more commentaries by BlackRock