Key takeaways

- The potential for a Fed pause presents an opportunity for investors to consider adding duration back into their portfolios.

- In this market regime, we believe duration serves well as a hedge and equity diversifier.

- Advisors who were underweight bonds in their traditional 60/40 portfolios should consider bringing bonds back to the benchmark level or an overweight.

Navigating Today's Environment It's Just Math

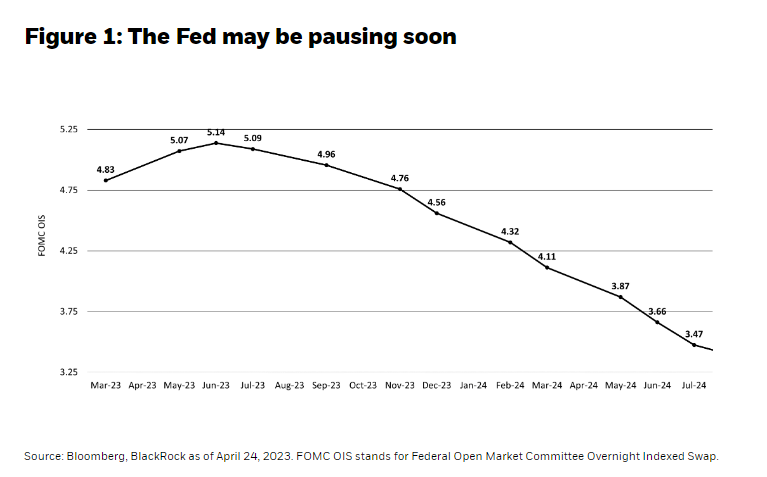

Beginning in March 2022, the Federal Reserve (Fed) raised interest rates at the fastest pace since 1980. Financial markets are now pricing in for the central bank to be near the end of its hiking cycle (Figure 1).

With yields at current levels, bond funds can lock in longer-term yields, offer price appreciation potential, and overall serve as a hedge against a possible hard landing. Though elevated cash balances worked during the Fed’s hiking cycle, we believe now is an opportunity for clients to consider adding duration given the potential for a Fed pause.

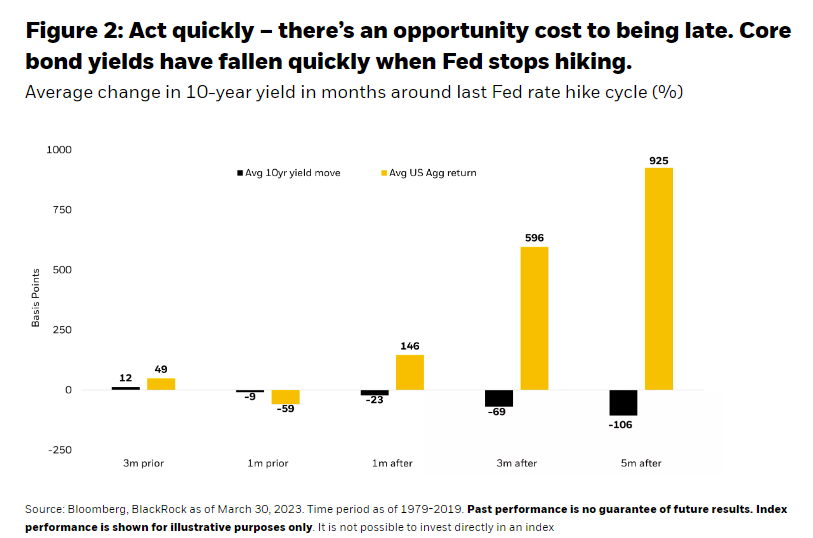

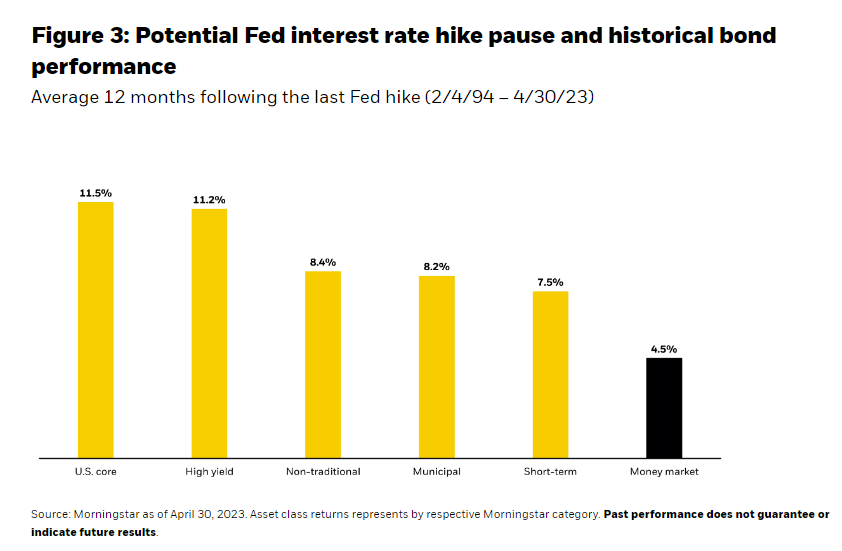

While investors are not penalized for being early to add duration, there is a potential cost to being late (Figure 2). Historically, cash underperforms when the Fed stops hiking (Figure 3).

Duration as a Hedge

In today’s environment of slowing growth and inflation volatility, duration may offer a hedge against potential market volatility and be used as a portfolio ballast. Amidst the Fed getting close to pausing, this bodes well for core bond funds, like the BlackRock Total Return Fund and the BlackRock Core Bond Fund, that may be able to offer defense in times of market stress in the form of income. For example, during periods where the Fed is hiking interest rates, the correlation of US Treasuries to equities is positive (+27%), however when the Fed is on hold or cutting rates the correlation drops (-16%)1.

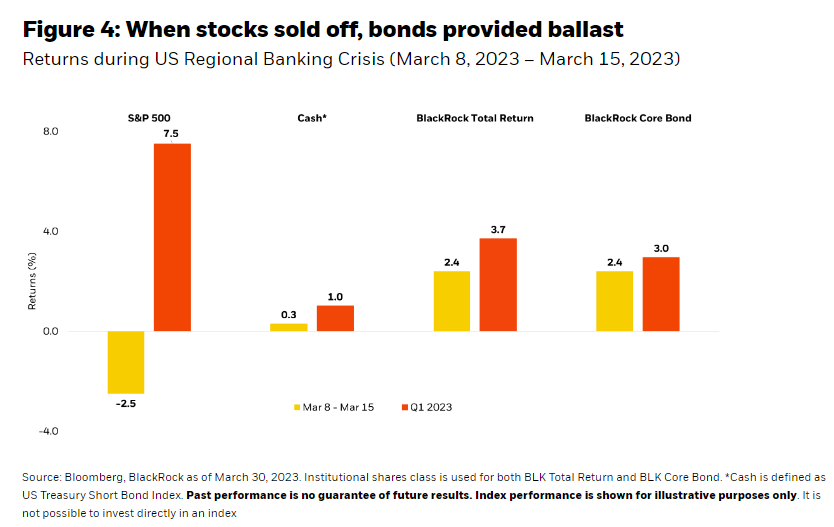

In addition, as markets were rattled by the US regional banking crisis in March of this year, Total Return and Core Bonds saw positive returns as equities sold off (Figure 4).

Case Study: Positioning the 60/40 Portfolio

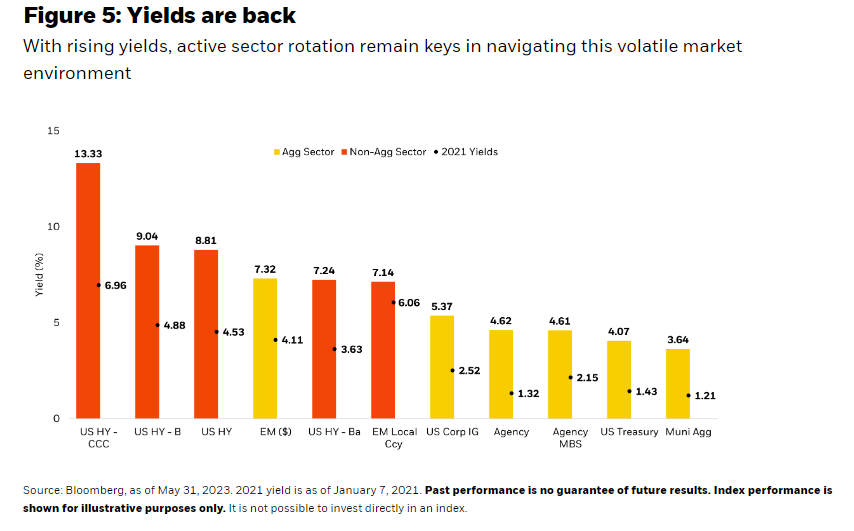

As of September 30, 2022, the average advisor’s portfolio was underweight fixed income by 9%2. In a market regime with over half of fixed income yielding over 4%, advisors should consider bringing bonds back to benchmark level or to an overweight (Figure 5). In periods of slowing growth, stocks may experience higher volatility, while high-quality bonds may offer a stable source of returns.

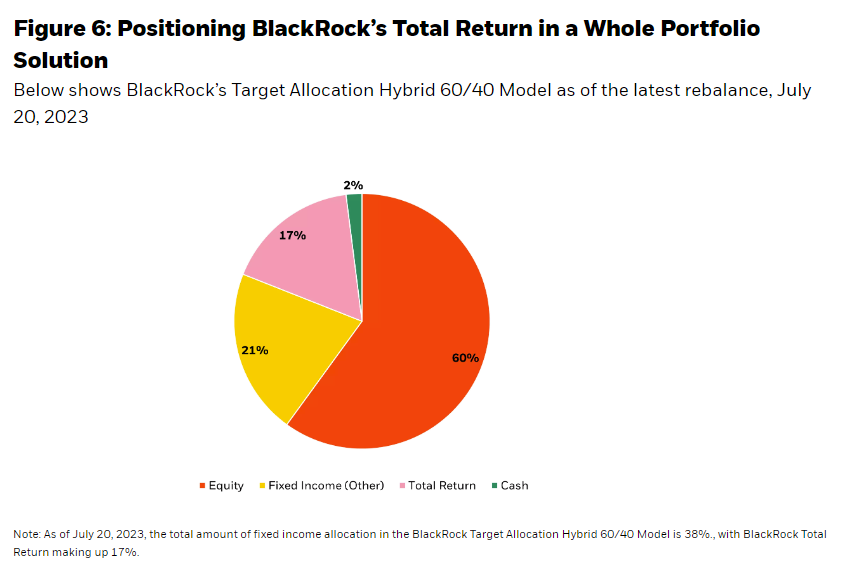

As of the latest rebalance in July 2023, BlackRock’s Target Allocation Hybrid 60/40 Model latest rebalance currently holds 60% and 38% of its portfolio in equities and fixed income, respectively – with the remainder being in cash. In this rebalance, the Model looked to enhance the overall quality of the portfolio and maintain its overweight to duration.

To increase equity diversification, dynamically navigate today’s bond market and source active returns, the Model continues to hold a 17% allocation to BlackRock’s Total Return Fund, making it the Model’s largest fixed income allocation (Figure 6).

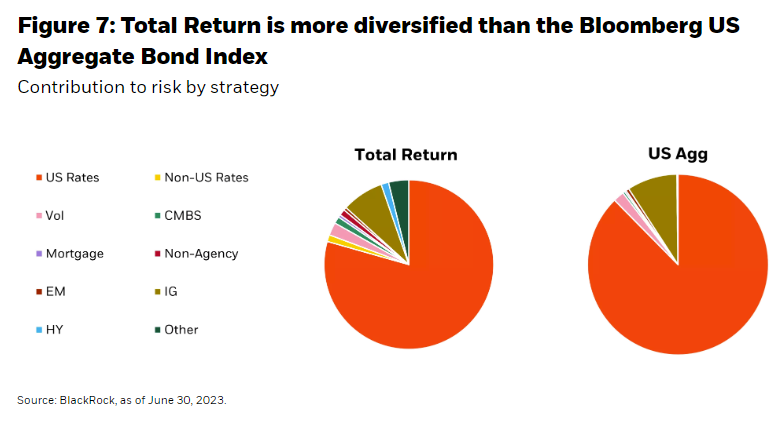

The Total Return Fund is an actively managed fixed income strategy that seeks to realize a total return exceeding that of the benchmark, Bloomberg US Aggregate Index. Given the fund's risk profile and long-term performance, Total Return Fund seeks to provide investors with core-bond defense by seeking to manage risk on the downside when markets come under pressure while striving to provide investors with core-plus-like returns by seeking to actively manage exposures for better returns over the long-term. The fund employs a diversified multi-sector approach built to navigate different market environments (Figure 7).

Summary

As the Federal Reserve nears the end of its hiking cycle, we believe now is an opportunity for investors to consider adding duration back to their portfolios. The duration may provide defense against potential market volatility and be used as a portfolio ballast during periods of slowing growth and inflation volatility. History shows that core bonds act as a diversifier when equity markets sold off.

The BlackRock Total Return Fund employs a diversified approach with sufficient flexibility in order to navigate periods of market volatility while providing a cushion in the form of income, and broad portfolio diversification. This has resulted in generating Core Plus-like returns with Core-like risk. As of June 30, 2023, the fund has a Yield to Worst (YTW) of 5.78% and 30 Day SEC Yield of 4.24% / 4.23% (subsidized/unsubsidized). The Bloomberg US Aggregate Index has a YTW of 4.79%, as of June 30, 2023.

In addition, BlackRock Core Bond provides investors with a diversified, core-bond exposure that seeks to generate attractive risk-adjusted returns that exceed the fund's benchmark, Bloomberg US Aggregate Index. The fund has a YTW of 5.38% and 30 Day SEC Yield of 4.37% / 4.26% (subsidized / unsubsidized) as of June 30, 2023.

The performance quoted represents past performance and does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when sold or redeemed, may be worth more or less than the original cost. Current performance may be lower or higher than the performance quoted. For current month-end returns visit www.blackrock.com.

1 Source: Bloomberg as of March 31, 2023.

2 Source: BlackRock, Aladdin. Data as of September 30, 2022, based on 5,417 portfolios.

3 The BlackRock Target Allocation Hybrid 60/40 Model invests in both BlackRock Exchange Traded-Funds and Mutual Funds.

Investing involves risks, including possible loss of principal.

Important Risks of the Funds: The mutual funds are actively managed and characteristics will vary.

International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation, and the possibility of substantial volatility due to adverse political, economic, or other developments. These risks often are heightened for investments in emerging/ developing markets or in concentrations of single countries.

Short-selling entails special risks. If the fund makes short sales in securities that increase in value, the fund will lose value. Any loss on short positions may or may not be offset by investing short-sale proceeds in other investments.

Fixed income risks include interest rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values.

Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments.

Non-investment-grade debt securities (high-yield/junk bonds) may be subject to greater market fluctuations, risk of default, or loss of income and principal than higher-rated securities.

Asset allocation strategies do not assure a profit and do not protect against loss.

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer, or solicitation to buy or sell any securities or to adopt any investment strategy.

The information and opinions contained in this material are derived from proprietary and non-proprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive, and are not guaranteed accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees, or agents. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

The Funds are distributed by BlackRock Investments, LLC (together with its affiliates, “BlackRock”).

© 2023 BlackRock, Inc. or its affiliates. All Rights Reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© BlackRock

Read more commentaries by BlackRock