- We see emerging markets better withstanding volatility and benefiting as supply chains rewire. We switch our EM debt preference to the hard currency from local.

- Developed market stocks slid last week and long-term bond yields jumped as markets focused on U.S. fiscal challenges. We see long-term yields rising more.

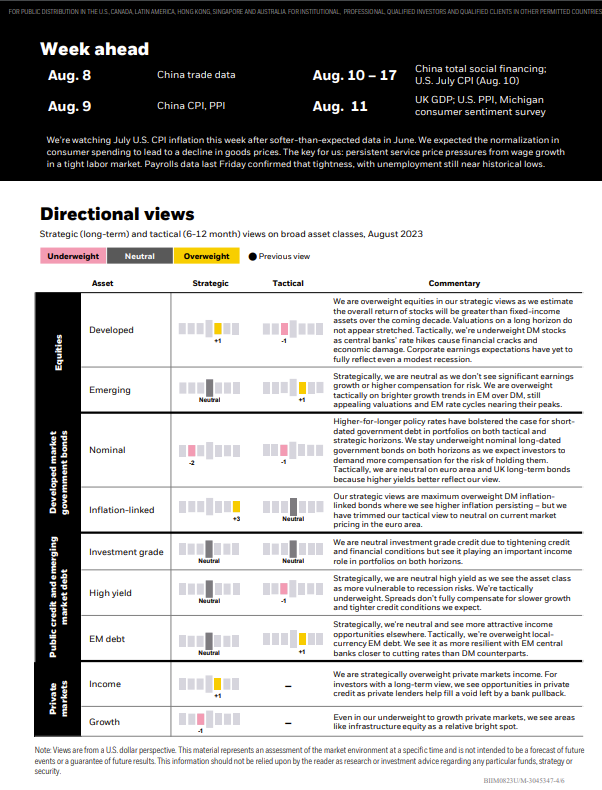

- All eyes are on U.S. inflation this week after softer-than-expected data in the last CPI print. We see persistent wage pressure keeping core inflation sticky.

Last week’s bond yield jump and stock tumble underscore we’re in a new regime of greater volatility. A renewed focus on U.S. fiscal challenges and surprise policy tightening in Japan have stirred up volatility in developed markets (DM). We think emerging market (EM) assets have an edge as their central banks cut rates and benefit from rewiring supply chains. What’s in the price is key. We rotate our EM bond preference to favor hard currency and stay granular in EM stocks.

Trade activity between nations dipped between World War One and World War Two (yellow shaded area in chart) before surging in the decades after World War Two as globalization took shape. Yet trade as a share of global GDP has plateaued (orange line) since the 2008 global financial crisis – one sign that globalization is under pressure. We see a world of fragmentation ahead: Competing defense and economic blocs are emerging. Multi-aligned nations are set to grow in power and influence, and we expect many major EMs to fall into this camp. As global fragmentation plays out, countries and companies are increasingly prioritizing security and resiliency – through industrial subsidies, export controls, and other tools – over maximum efficiency. We see this shift in priorities accelerating the rewiring of supply chains as nations aim to bring production closer to home. All this favors selected EMs, in our view.

Against that structural backdrop, we also favor broad EM exposures over DMs in the short term. DMs are experiencing bouts of volatility and we see the risk of more. The Fitch Ratings downgrade of the U.S. credit rating last week and the U.S. Treasury’s sizable borrowing needs put a spotlight on the challenging U.S. fiscal outlook. We think EMs are relatively better positioned to withstand some of this volatility. That’s partly due to EM central banks nearing the end of their rate hiking cycles. Some have started to cut policy rates, like in Chile and Brazil. Yet they’re not immune from a sharp hit to risk assets, in our view.

We put our new playbook in action again by gauging what’s in the price. We flip our overweight EM local currency debt to neutral and turn overweight EM hard currency debt on a six- to 12-month tactical horizon. We had been overweight EM local currency debt since March on attractive yields from EM central banks nearing the end of their hiking cycles and a broadly weaker U.S. dollar. We began to reassess our view on local currency in July: Yields have fallen closer to U.S. Treasury yields. Rate cuts seem largely priced in and could put downward pressure on EM currencies, dragging on local currency returns.

EM hard currency debt – issued in U.S. dollars and thus cushioning returns from any local currency weakness – looks more attractive. Hard currency debt is more diversified than the local currency, based on J.P. Morgan indexes, and it could benefit from the rewiring of globalization. We also think lower credit ratings in EM hard currency debt are priced in given that yields are at a near 14-year high versus local currency bond yields, Refinitiv data show.

We prefer EM bonds and stocks as we see a rewiring of supply chains benefiting select countries that offer valuable commodities and supply chain inputs. That includes oil from the Gulf states; India’s chemicals and industrial manufacturing; South Korea’s battery and memory supply chain businesses; Indonesia’s nickel and cobalt; and Chile’s lithium. Some, like Mexico, could benefit from U.S. and other DM efforts to reshore production closer to home. That push includes the making of semiconductors – the technology powering artificial intelligence (AI) and a key part of major EM tech sectors. Yet as an investment opportunity, the AI mega force may be bigger within DM, supporting revenues and margins across sectors.

Bottom line: We are in a new regime of greater volatility – and we see EMs better positioned to withstand it, for now. We harness mega forces to find opportunities based on what’s in the price. We stay overweight EM debt overall but switch our preference to hard currency on its high yields. We like EMs that may benefit from rewiring globalization.

Market backdrop

Developed market stocks retreated and long-term government bond yields rose, with the U.S. 10-year Treasury yield jumping above 4% to near 15-year highs reached last year. We think the U.S. rating downgrade helped put a spotlight on the fiscal challenges it faces. Along with greater U.S. Treasury bond issuance, that could prompt investors to demand more term premium, or compensation for the risk of holding long-term government bonds – and push long-term yields even higher.

Macro take

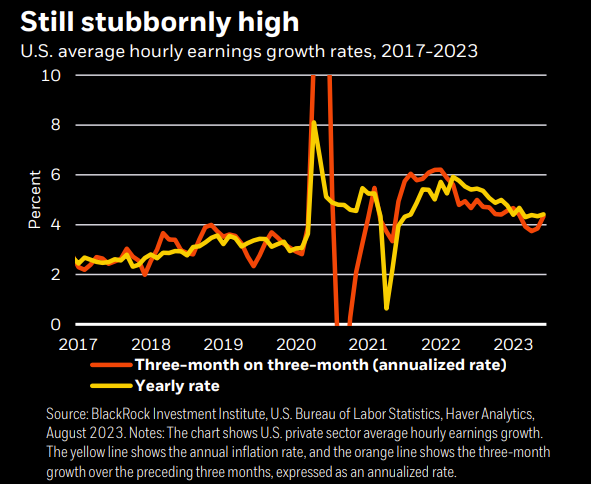

Last week’s U.S. jobs report for July clearly shows wage pressures aren’t abating just yet despite recent data raising hopes of U.S. inflation falling durably back to the Federal Reserve’s 2% target.

Growth in average hourly earnings – a key gauge of wage trends – is still elevated at a 4.7% annualized pace over the three months through July. See the chart. Even though employment growth is slowing, the labor market is set to tighten at this level of job growth. The labor force participation rate remains stuck for the fifth month in a row and the unemployment rate ticked down near five-decade lows to 3.5%. That’s the labor supply shock at work.

As the U.S. population ages, workers retire and labor supply gets squeezed, we don’t think this level of employment growth is slow enough to help ease pressures on wage growth to a level consistent with 2% inflation. That’s even with the seemingly positive news from the second quarter labor cost data. We see the Fed keeping rates high as a result.

Investment themes

1 Holding tight

- Markets have come around to the view that central banks will not quickly ease policy in a world shaped by supply constraints – notably worker shortages in the U.S.

- We see central banks being forced to keep policy tight to lean against inflationary pressures. This is not a friendly backdrop for broad asset class returns, marking a break from the four decades of steady growth and inflation known as the Great Moderation.

- Economic relationships investors have relied upon could break down in the new regime. The shrinking supply of workers in several major economies due to aging means a low unemployment rate is no longer a sign of the cyclical health of the economy. Broad worker shortages could create incentives for companies to hold onto workers, even if sales decline, for fear of not being able to hire them back. This poses the unusual possibility of “full employment recessions” in the U.S. and Europe. That could take a bigger toll on corporate profit margins than in the past as companies maintain employment, creating a tough outlook for DM equities.

- Investment implication: Income is back. That motivates our overweight to short-dated U.S. Treasuries.

2 Pivoting to new opportunities

- Greater volatility has brought more divergent security performance relative to the broader market. Benefiting from this requires getting more granular and eyeing opportunities on horizons shorter than our tactical ones. We go granular by tilting portfolios to areas where we think our macro view is priced in.

- We think dispersion within and across asset classes – or the extent to which prices deviate from an index – will be higher in the new regime amid the various crosscurrents at play, allowing for granularity. That offers more ways to build portfolio “breadth” via uncorrelated exposures, in our view.

- We think it also means security selection, expertise, and skill are even more important to achieving above-benchmark returns. Relative value opportunities from potential market mispricings are also likely to be more abundant.

- Investment implication: We like quality in both equities and fixed income.

BlackRock Investment Institute

The BlackRock Investment Institute (BII) leverages the firm’s expertise and generates proprietary research to provide insights on macroeconomics, sustainable investing, geopolitics, and portfolio construction to help Blackrock’s portfolio managers and clients navigate financial markets. BII offers strategic and tactical market views, publications, and digital tools that are underpinned by proprietary research.

General disclosure: This material is intended for information purposes only, and does not constitute investment advice, a recommendation, or an offer or solicitation to purchase or sell any securities to any person in any jurisdiction in which an offer, solicitation, purchase, or sale would be unlawful under the securities laws of such jurisdiction. This material may contain estimates and forward-looking statements, which may include forecasts and do not represent a guarantee of future performance. This information is not intended to be complete or exhaustive and no representations or warranties, either express or implied, are made regarding the accuracy or completeness of the information contained herein. The opinions expressed are as of Aug. 7, 2023, and are subject to change without notice. Reliance upon information in this material is at the sole discretion of the reader. Investing involves risks.

In the U.S. and Canada, this material is intended for public distribution. In the European Economic Area (EEA): this is issued by BlackRock (Netherlands) B.V. and is authorized and regulated by the Netherlands Authority for the Financial Markets. Registered office Amstelplein 1, 1096 HA, Amsterdam, Tel: 020 – 549 5200, Tel: 31-20-549-5200. Trade Register No. 17068311 For your protection telephone calls are usually recorded. In the UK and Non-European Economic Area (EEA) countries: this is Issued by BlackRock Advisors (UK) Limited, which is authorized and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL, Tel: +44 (0)20 7743 3000. Registered in England and Wales No. 00796793. For your protection, calls are usually recorded. Please refer to the Financial Conduct Authority website for a list of authorized activities conducted by BlackRock. In Italy, for information on investor rights and how to raise complaints please go to https://www.blackrock.com/corporate/compliance/investor-right available in Italian. For qualified investors in Switzerland: This document is marketing material. This document shall be exclusively made available to, and directed at, qualified investors as defined in Article 10 (3) of the CISA of 23 June 2006, as amended, at the exclusion of qualified investors with an opting-out pursuant to Art. 5 (1) of the Swiss Federal Act on Financial Services ("FinSA"). For information on Art. 8 / 9 Financial Services Act (FinSA) and on your client segmentation under Art. 4 FinSA, please see the following website: www.blackrock.com/finsa. For investors in Israel: BlackRock Investment Management (UK) Limited is not licensed under Israel’s Regulation of Investment Advice, Investment Marketing and Portfolio Management Law, 5755-1995 (the “Advice Law”), nor does it carry insurance thereunder. In South Africa, please be advised that BlackRock Investment Management (UK) Limited is an authorized financial services provider with the South African Financial Services Board, FSP No. 43288. In the DIFC this material can be distributed in and from the Dubai International Financial Centre (DIFC) by BlackRock Advisors (UK) Limited — Dubai Branch which is regulated by the Dubai Financial Services Authority (DFSA). This material is only directed at 'Professional Clients’ and no other person should rely upon the information contained within it. Blackrock Advisors (UK) Limited - Dubai Branch is a DIFC Foreign Recognised Company registered with the DIFC Registrar of Companies (DIFC Registered Number 546), with its office at Unit 06/07, Level 1, Al Fattan Currency House, DIFC, PO Box 506661, Dubai, UAE, and is regulated by the DFSA to engage in the regulated activities of ‘Advising on Financial Products’ and ‘Arranging Deals in Investments’ in or from the DIFC, both of which are limited to units in a collective investment fund (DFSA Reference Number F000738)In the Kingdom of Saudi Arabia, issued in the Kingdom of Saudi Arabia (KSA) by BlackRock Saudi Arabia (BSA), authorized and regulated by the Capital Market Authority (CMA), License No. 18-192-30. Registered under the laws of KSA. Registered office: 29th floor, Olaya Towers – Tower B, 3074 Prince Mohammed bin Abdulaziz St., Olaya District, Riyadh 12213 – 8022, KSA, Tel: +966 11 838 3600. The information contained within is intended strictly for Sophisticated Investors as defined in the CMA Implementing Regulations. Neither the CMA nor any other authority or regulator located in KSA has approved this information. The information contained within does not constitute and should not be construed as an offer of, invitation, or proposal to make an offer for, the recommendation to apply for, or an opinion or guidance on a financial product, service, and/or strategy. Any distribution, by whatever means, of the information within and related material to persons other than those referred to above is strictly prohibited. In the United Arab Emiratesis only intended for - natural Qualified Investors as defined by the Securities and Commodities Authority (SCA) Chairman Decision No. 3/R.M. of 2017 concerning Promoting and Introducing Regulations. Neither the DFSA nor any other authority or regulator located in the GCC or MENA region has approved this information. In the State of Kuwait, those who meet the description of a Professional Client as defined under the Kuwait Capital Markets Law and its Executive Bylaws. In the Sultanate of Oman, sophisticated institutions that have experience in investing in local and international securities, are financially solvent and have knowledge of the risks associated with investing in securities. In Qatar, for distribution with pre-selected institutional investors or high net worth investors. In the Kingdom of Bahrain, to Central Bank of Bahrain (CBB) Category 1 or Category 2 licensed investment firms, CBB licensed banks, or those who would meet the description of an Expert Investor or Accredited Investors as defined in the CBB Rulebook. The information contained in this document does not constitute, and should not be construed as an offer of, invitation, inducement, or proposal to make an offer for, recommendation to apply for, or an opinion or guidance on a financial product, service, and/or strategy. In Singapore, this is issued by BlackRock (Singapore) Limited (Co. registration no. 200010143N). This advertisement or publication has not been reviewed by the Monetary Authority of Singapore. In Hong Kong, this material is issued by BlackRock Asset Management North Asia Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong. In South Korea, this material is for distribution to Qualified Professional Investors (as defined in the Financial Investment Services and Capital Market Act and its sub-regulations). In Taiwan, independently operated by BlackRock Investment Management (Taiwan) Limited. Address: 28F., No. 100, Songren Rd., Xinyi Dist., Taipei City 110, Taiwan. Tel: (02)23261600. In Japan, this is issued by BlackRock Japan. Co., Ltd. (Financial Instruments Business Operator: The Kanto Regional Financial Bureau. License No375, Association Memberships: Japan Investment Advisers Association, the Investment Trusts Association, Japan, Japan Securities Dealers Association, Type II Financial Instruments Firms Association.) For Professional Investors only (Professional Investor is defined in Financial Instruments and Exchange Act). In Australia, issued by BlackRock Investment Management (Australia) Limited ABN 13 006 165 975 AFSL 230 523 (BIMAL). The material provides general information only and does not take into account your individual objectives, financial situation needs, or circumstances. In China, this material may not be distributed to individual residents in the People’s Republic of China (“PRC”, for such purposes, excluding Hong Kong, Macau, and Taiwan) or entities registered in the PRC unless such parties have received all the required PRC government approvals to participate in any investment or receive any investment advisory or investment management services. For Other APAC Countries, this material is issued for Institutional Investors only (or professional/sophisticated /qualified investors, as such a term may apply in local jurisdictions). In Latin America, no securities regulator within Latin America has confirmed the accuracy of any information contained herein. The provision of investment management and investment advisory services is a regulated activity in Mexico and thus is subject to strict rules. For more information on the Investment Advisory Services offered by BlackRock Mexico please refer to the Investment Services Guide available at www.blackrock.com/mx

©2023 BlackRock, Inc. All Rights Reserved. BLACKROCK is a trademark of BlackRock, Inc., or its subsidiaries in the United States and elsewhere. All other trademarks are those of their respective owners.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© BlackRock

Read more commentaries by BlackRock