The results from our latest quarterly survey of Loomis Sayles’ corporate credit analysts point to some good news. In aggregate, their responses indicated leverage had moved lower, input prices continued their steady march lower, and they felt the risk of a potential crisis had leveled off. While we welcome these developments, we don’t think we have hit bottom in this credit cycle. Our analysts expect further deterioration in three important measures of corporate strength: their credit outlook, profit margins and pricing power. The bottom line: we believe companies are likely to experience more pain in the months to come.

Easing inflation feeding through to lower costs

On the positive side, we want to highlight the continued decline in input costs. Costs have been trending lower for several quarters—the CANDIs’ most recent reading showed a particularly steep drop from six months ago— as global supply chains have returned to pre-pandemic norms. Our findings square with recent inflation data, which showed prices easing at both the consumer and producer level. Inflation readings remain well above the Federal Reserve’s two percent target.

Leverage, the ratio of debt to profits, has not reached concerning levels in this cycle in our view. In most industries, our analysts felt the risk of a potential crisis had largely stabilized at a benign level.

Key metrics hint at further erosion

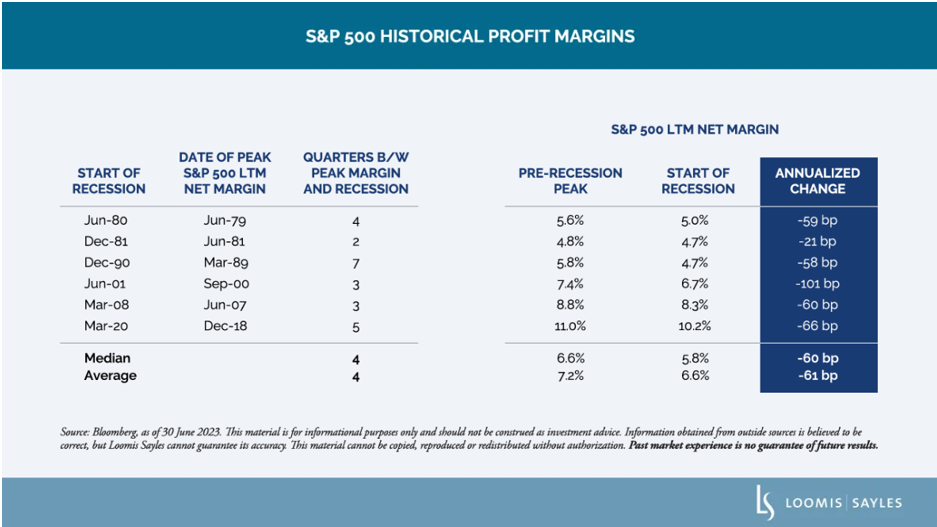

On the opposite side of the ledger, profit margins for the S&P 500 Index have fallen about 4.7% from their peak six quarters ago.i[i] The table below shows how profit margins tend to peak about one year before a recession hits.

Because profit margins entered this current slowdown at elevated levels, today’s margins don’t look bad by historical standards, in our view. Still, we see more room for them to come down. In our latest survey results, analysts anticipate shrinking margins in 13 industries, while they expect margins to improve in five. The CANDIs’ readings on analysts’ credit outlook and pricing power tell much the same story: the number of analysts expecting further deterioration in their industries is greater than those who see progress.

When it comes to interpreting the CANDIs’ output, direction is important. So are the levels. Levels for three key categories—margins, pricing power and credit outlook—are currently weak, in our view. We would want to see considerable gains in all three metrics before we’d consider calling for a genuine recovery.

The road ahead

In our view, what happens from here will likely be determined, in part, by the Federal Reserve. If inflation continues to ease, the central bank could ease up its restrictive policy sooner, which could help the economy avoid a potential recession. Persistent inflation and more rate hikes would likely increase the chances of a recession. Corporates appear prepared to weather a mild downturn. Barring some unforeseen shock, we would expect any further deterioration in corporate strength to be gradual, not precipitous. Consistent with that view, we also anticipate only modest increases in the default rate over the next six months. We will continue monitoring a broad range of industries to see what comes next.

MALR031449

Market conditions are extremely fluid and change frequently.

Market scenarios have inherent limitations and should not be viewed as predictions of future events. They rely on opinions, assumptions and mathematical models which can turn out to be incomplete or inaccurate. These opinions and assumptions are often based on past events and do not consider unforeseen events or developments. Past market experience is no guarantee of future results.

This blog post is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors only and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. This information is subject to change at any time without notice. Information obtained from outside sources is believed to be correct, but Loomis Sayles cannot guarantee its accuracy.

i Credit Analyst Diffusion Indices {CANDIs) were created and are managed by Loomis Sayles. They are proprietary survey-based diffusion indices that measure changes in indicators of corporate health.

ii Source: Bloomberg, as of 30 June 2023.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Loomis, Sayles & Co.

Read more commentaries by Loomis, Sayles & Co.