The outlook for the British economy is sub-par.

Each summer, I enjoy watching a bit of the British Open golf championship. The links-style courses are set naturally into the landscape, with many close to the seashore. The scenery is beautiful.

To be honest, I also like watching professionals try to overcome rain squalls that soak to the skin, grass that is thicker than hay and bunkers whose faces are taller than the players are. One year while he was in his prime, Tiger Woods counted himself lucky to break 90 in particularly abysmal Open weather. At the time, a friend noted that he could finally claim that his scores were comparable to Tiger’s.

Watching the play at Royal Liverpool this year, I saw a parallel between the plight of the golfers and the challenges facing the British economy. Both have to deal with an inhospitable environment and a series of steep obstacles.

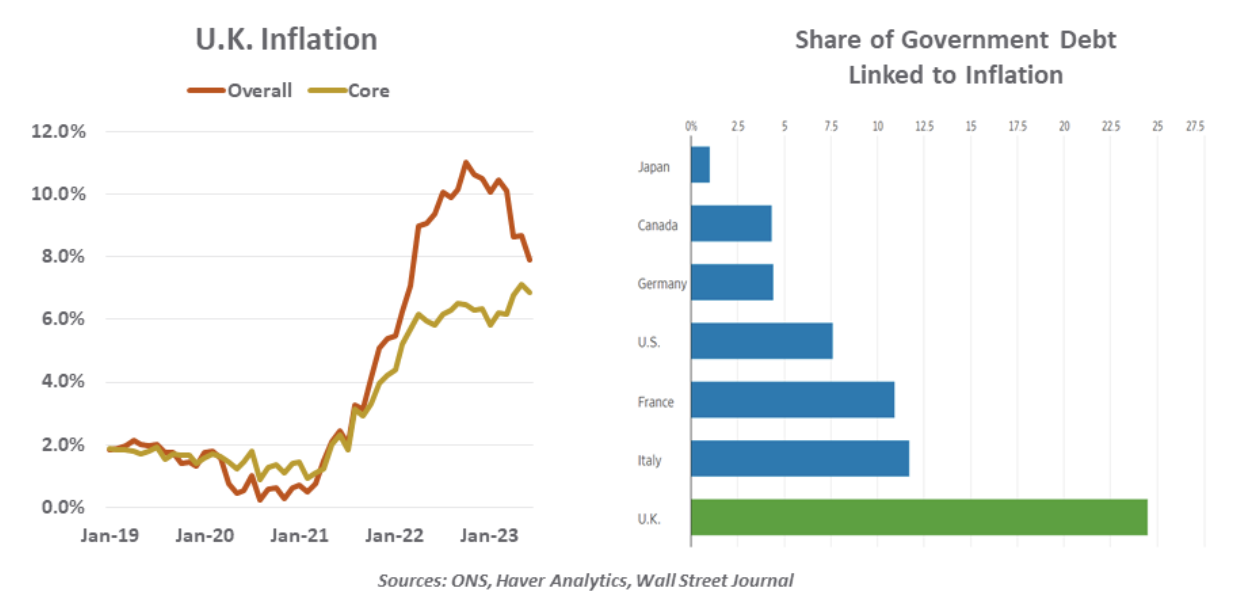

Britain is enduring the same post-pandemic economic afflictions that other countries are, but their manifestation in the U.K. has been more severe. Real gross domestic product is still below its 2019 level, long after other developed countries pushed through that threshold. U.K. inflation reached a much higher peak than it did elsewhere and remains elevated in spite of aggressive interest rate increases from the Bank of England. British equity indices have far underperformed those from other developed markets over the past year, and the pound hit a new all-time low against the U.S. dollar last fall.

Rising interest rates have pressured national budgets around the world, but Great Britain has been challenged most of all. Almost one-quarter of its national debt is indexed to inflation; as a result, interest costs now compose more than 10% of government revenues, by far the highest fraction in Europe. Britain’s annual budget deficit has risen to more than 5% of gross domestic product (GDP), larger than those seen in Greece and Spain.

Britain’s bond markets have become especially sensitive to fiscal developments. The penalty for reckless budgeting last fall was severe: the gilt crisis that took hold last September will make it very difficult for the government to support the economy by going further into debt.

Taming inflation is proving to be a much taller order for the U.K. than it is for other countries. The challenge is a combination of bad luck and bad policy.

Food prices are escalating much more rapidly in Britain than they are in other developed countries. Reliance on imports is a key reason for this: transportation costs have risen and supplies from Ukraine have been disrupted. Grocery costs have also been elevated by Brexit: frictions like increased paperwork and product checks have accounted for one-third of food price inflation since 2019, according to the London School of Economics.

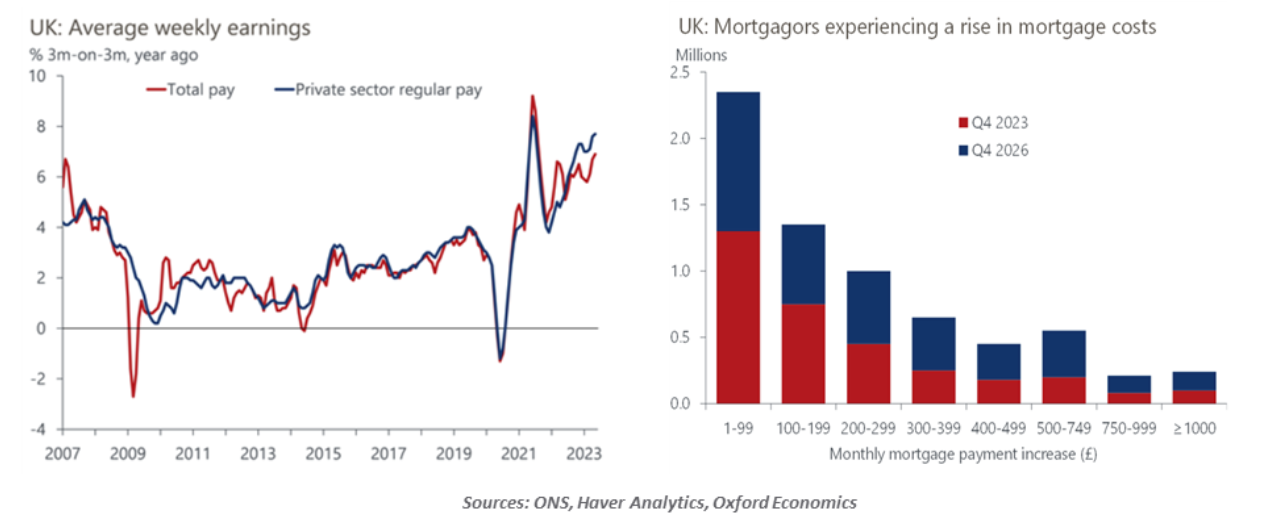

The high cost of essentials has led workers to seek larger pay increases. The British labor force is very tight: demand for employees remains strong, while COVID-19 increased the number of people who count themselves as unavailable for work because of illness. A series of public sector strikes set broad terms that have carried over to the private sector; wage increases in the United Kingdom are in excess of 7% over the past year. This has pushed service prices higher by more than 6% over the same period.

It is hard to overstate the impact of Brexit on Britain’s employment market. The exodus of EU workers in the wake of the 2016 referendum has been estimated at 1% of the U.K. labor force, and the pandemic prompted additional departures. The losses have primarily affected basic service industries, which are presently experiencing the biggest labor shortages.

While there has been some relaxation of standards to allow more skilled workers into the country, an extension to lower-skilled sectors appears unlikely. The current Tory government faces elections next year amid a big deficit in the polls; opening the borders to more newcomers would risk alienating a sector of the electorate that may be critical to the outcome.

Productivity in the U.K. has grown at half the rate of other developed countries over the past 15 years. Brexit plays a role here, too: uncertainty over the trade environment has hindered business investment. Frequent turnover in British governments has also been a headwind for planning in the private sector and industrial policy within the public sector.

Britain is closer to experiencing a wage-price spiral than any other country. Inflation is psychological and inertial, meaning that it is built from expectations and can take a long time to uproot once embedded. At the same time, economic activity is clearly decelerating, and the odds of recession are rising. This is the unpleasant combination of circumstances facing the Bank of England as it meets to set policy next week.

It is nearly certain that overnight rates will be increased by another half-point on Thursday, and we think that there will be more to come after that. This is a vastly different path from the one that markets anticipated three months ago when the Bank of England was expected to be on a prolonged hold.

The impact of interest rate increases on the British economy is significantly different from the influence seen in other countries. The main reason for this is the structure of U.K. mortgages, most of which are repriced at regular intervals. The maximum term for a mortgage in Britain is five years, compared to 30 years in the United States.

Quoted rates on British 2- and 5-year home loans have jumped from just over 1% two years ago to well over 5% today. As borrowers reset, they will see significant increases in monthly payments, which will limit consumption. Risks to the economy seem skewed to the downside.

If the policy were played out on a golf course, Parliament and the Bank of England would presently find themselves in deep rough, two hundred yards from a small green that is guarded by an array of pot bunkers. Getting the U.K. economy back to par with the rest of Europe is going to take some bold strokes.

Information is not intended to be and should not be construed as an offer, solicitation, or recommendation with respect to any transaction and should not be treated as legal advice, investment advice, or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulations. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Northern Trust

Read more commentaries by Northern Trust