Key takeaways:

- Technology companies have gone from massive underperformers to once again dominating equity markets.

- Year-to-date technology and the tech-heavy consumer discretionary sector are up 32% and 39% respectively.

Russ Koesterich CFA, JD, Managing Director, and Portfolio Manager discusses how improving economic expectations may suggest adding to cyclical areas of the market.

Like many trends that abruptly reversed in early 2023, technology companies have gone from massive underperformers to once again dominating equity markets. Year-to-date, technology and the tech-heavy consumer discretionary sector are up 32% and 39% respectively (as measured by the respective S&P GICS sector index). This year’s performance is handily beating the market as well as trouncing last year’s winners, energy, and low-beta, defensive stocks.

That said, while tech companies continue to grind higher on a surge of enthusiasm for all things related to artificial intelligence (AI), relative performance has shifted. Recently many cyclical parts of the market, including the industrials sector, have outpaced the broader market as well as tech. This shift in leadership has coincided with a steady stream of better-than-expected economic data. As economic expectations improve, the equity rally has expanded to favor more cyclical companies. I would expect this trend to continue and would consider adding exposure to industrial stocks.

Recession fears subsiding

In contrast to earlier in the year, recession fears are abating and growth expectations rising. A Bloomberg consensus of 2023 U.S. gross domestic product (GDP) forecasts growth at 1.3%, a significant improvement from January’s consensus of 0.5%. And although inflation estimates have started to slip, the consensus is still around 4%. Taken together, this suggests nominal GDP (NGDP) of 5% or more.

Nominal GDP matters as it is closely related to corporate earnings. If nominal GDP is likely to come in better than expected, earnings probably will as well. This shift would disproportionately benefit cyclical companies whose revenue is more closely linked to the economic cycle.

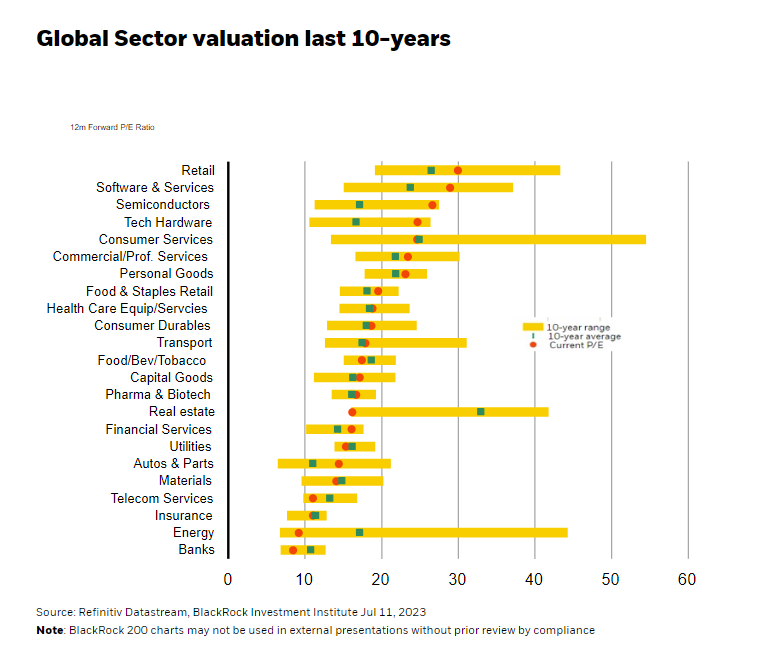

Not everything is expensive

Valuation is another factor favoring cyclicals. In aggregate, U.S. equities are trading at approximately 19x forward earnings, well above the historical average and a premium to most international markets. However, the premium is being driven by a relatively small number of stocks, mostly in technology and tech-related areas. Outside of these, most sectors, including industries, are trading at or below their long-term average (see Chart 1).

Apart from a stronger economy and cheaper valuations, many industrial companies, particularly in manufacturing and automation, stand to benefit from longer-term secular themes. Despite artificial intelligence has captured the public’s imagination, other innovations and trends may prove just as profound. A rapidly changing geopolitical landscape, pandemic-induced supply concerns, and a renewed focus on defense spending are driving generational shifts. For example, after decades of building increasingly complicated global supply chains, companies are now focusing on resilience rather than just cost. The net effect is a trend towards onshoring and ‘near-shoring’, i.e., locating manufacturing in adjacent and friendly countries.

What does this trend mean for broader portfolio positioning? While I still like tech and would maintain a long-term overweight, there are other opportunities that might justify a modest shift in positioning. A more resilient economy, reasonable valuations, and a compelling set of long-term tailwinds suggest that it may be an opportune time to take some profits in tech and redirect to select industrials.

Carefully consider the Funds' investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Funds' prospectuses or, if available, the summary prospectuses, which may be obtained by visiting the iShares Fund and BlackRock Fund prospectus pages. Read the prospectus carefully before investing.

Investing involves risk, including possible loss of principal.

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer, or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of June 2023 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive, and are not guaranteed accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees, or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader. Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. You cannot invest directly in an index.

The BlackRock Model Portfolios are provided for illustrative and educational purposes only, do not constitute research, investment advice or a fiduciary investment recommendation from BlackRock to any client of a third party financial advisor (each, a "Financial Advisor"), and are intended for use only by such Financial Advisor as a resource to help build a portfolio or as an input in the development of investment advice from such Financial Advisor to its own clients and shall not be the sole or primary basis for such Financial Advisor’s recommendation and/or decision. Such Financial Advisors are responsible for making their own independent fiduciary judgment as to how to use the BlackRock Model Portfolios and/or whether to implement any trades for their clients. BlackRock does not have investment discretion over, or place trade orders for, any portfolios or accounts derived from the BlackRock Model Portfolios. BlackRock is not responsible for determining the appropriateness or suitability of the BlackRock Model Portfolios or any of the securities included therein for any client of a Financial Advisor. Information and other marketing materials provided by BlackRock concerning the BlackRock Model Portfolios –including holdings, performance, and other characteristics –may vary materially from any portfolios or accounts derived from the BlackRock Model Portfolios. Any performance shown for the BlackRock Model Portfolios does not include brokerage fees, commissions, or any overlay fee for portfolio management, which would further reduce returns. There is no guarantee that any investment strategy will be successful or achieve any particular level of results. The BlackRock Model Portfolios themselves are not funded. The BlackRock Model Portfolios, allocations, and data are subject to change.

For financial professionals: BlackRock’s role is limited to providing you or your firm (collectively, the “Advisor”) with non-discretionary investment advice in the form of model portfolios in connection with its management of its client’s accounts. The implementation of, or reliance on, a Managed Portfolio Strategy is left to the discretion of the Advisor. BlackRock is not responsible for determining the securities to be purchased, held and sold for a client’s account(s), nor is BlackRock responsible for determining the suitability or appropriateness of a Managed Portfolio Strategy or any securities included therein for any of the Advisor’s clients. BlackRock does not place trade orders for any of the Advisor’s clients’ account(s). Information and other marketing materials provided to you by BlackRock concerning a Managed Portfolio Strategy—including holdings, performance and other characteristics–may not be indicative of a client’s actual experience from an account managed in accordance with the strategy.

For investors: BlackRock’s role is limited to providing your Advisor with non-discretionary investment advice in the form of model portfolios in connection with its management of its client’s accounts. The implementation of, or reliance on, a Managed Portfolio Strategy is left to the discretion of your Advisor. BlackRock is not responsible for determining the securities to be purchased, held and sold for your account(s), nor is BlackRock responsible for determining the suitability or appropriateness of a Managed Portfolio Strategy or any securities included therein. BlackRock does not place trade orders for any Managed Portfolio Strategy account. Information and other marketing materials provided to you by BlackRock concerning a Managed Portfolio Strategy—including holdings, performance and other characteristics—may not be indicative of a client’s actual experience from an account managed in accordance with the strategy. This material is subject to change.

Prepared by BlackRock Investments, Inc. LLC. Member FINRA

©2023 BlackRock, Inc or its affiliates. All rights reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

A message from Advisor Perspectives and VettaFi: Our latest white papers offer research and analysis covering the most important topics and trends in financial planning, investing, and practice management. Click here to read the top insights from our valued partners.

© BlackRock

Read more commentaries by BlackRock