How will we tell if the mythical soft landing is happening?

Our work is guided by the questions we receive from our clients and colleagues. Last year at this time, we were bombarded with inquiries about whether we were in a recession. Of late, though, a more encouraging curiosity has emerged: Are we in the soft landing? While we prefer the latter tone, it is premature to respond affirmatively.

For over a year, we have resisted forecasting a recession. Our base case remains for inflation to decline without a loss to gross domestic product (GDP) or a major gain in unemployment. All along, we have received feedback about our conclusion sounding too rosy. The assumption that nothing else would go wrong seemed unreasonably optimistic after enduring so many setbacks during the pandemic. Even Fed Chair Jerome Powell altered the scenario description to a “soft-ish” landing. Common sense dictated that some pain was inevitable.

The journey has been anything but smooth. Equity markets offered little reason for cheer throughout 2022. A rolling recession has imperiled several sectors that have since returned to growth. Crises surrounding gilt markets, cryptocurrency and the banking industry all had the potential to spark a broad downturn, but one has not emerged.

The absence of widespread malaise does not mean the hard times are over. Core inflation continues to run high, and central banks are still tightening in an effort to contain prices. Healthy labor conditions and favorable equity markets have helped to lift sentiment so far this year, but risks of a downturn are still elevated.

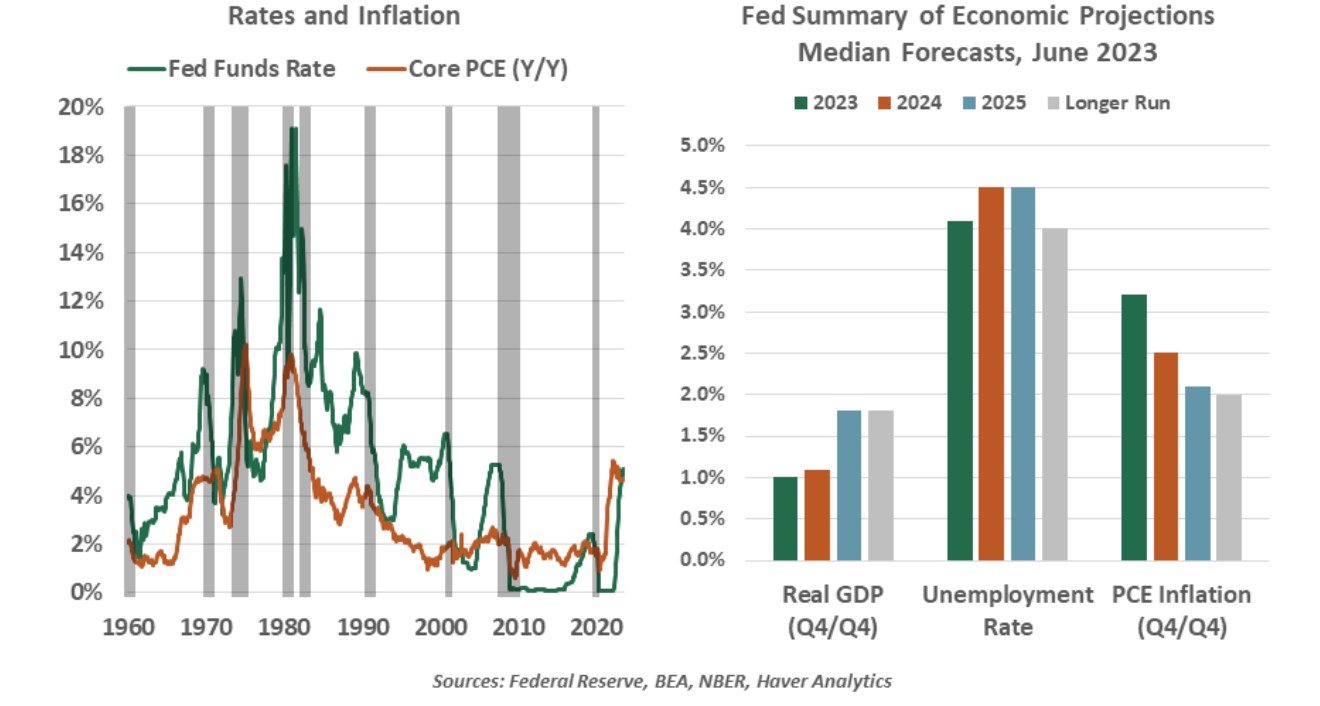

To call the soft landing, then, we will need to see core inflation move steadily closer to 2%. The cooling needs to happen in the context of steady employment. Lower demand may lead to some loss of jobs; a small increase in the unemployment rate is still very likely. The most important “all clear” signal will be central bank rate cuts if they are undertaken due to sustainably lower inflation. These outcomes are consistent with the forecast in the Federal Reserve’s latest Summary of Economic Projections.

History is not on our side. Actual examples of soft landings are rare. The Fed arguably engineered soft landings in 1966 and 1994. Circumstances are always different, but one key point stands out: those scarce examples happened with immediate, proactive rate hikes at the first hint of rising prices. Part of today’s problem is that the Fed waited to tighten until the worst of the COVID disruptions were in the past, causing a full-year delay between inflation rising and rate hikes. Rate cuts have usually been a sign of an unfolding economic emergency; cuts due to lower inflation in the 1970s and 80s were executed too soon.

While we await the signs of a soft landing taking shape, we remain vigilant for the signals of its failure. Among them could be:

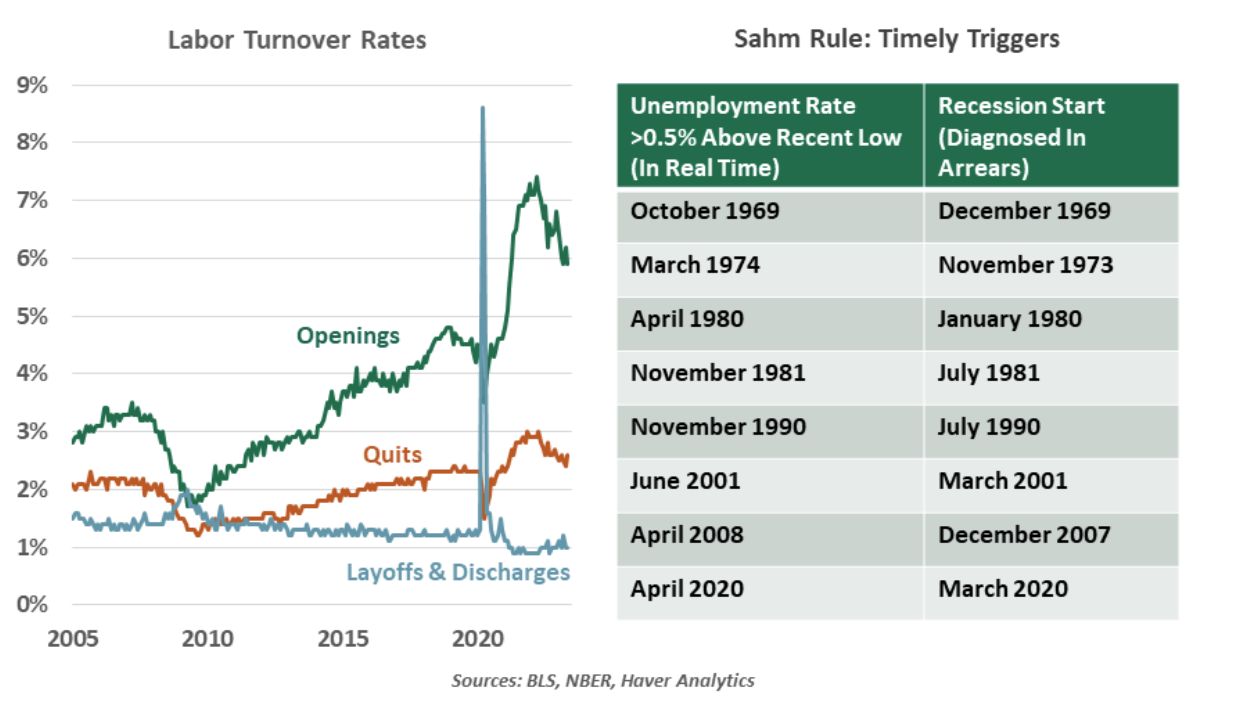

- Job losses are the primary indicator of the onset of a recession. Thus far, employment has been buoyant, which has fueled the strength in consumption that has been the core of economic strength. Openings are still elevated, and layoffs have been limited.

The “Sahm Rule” states a recession is underway when the three-month average unemployment rate rises half a percentage point above its minimum in the prior year. The relationship has held for over fifty years, with no false positives. The low point of unemployment was 3.4% in January and April 2023; sustained unemployment of 3.9% or above in the year ahead would trigger the rule.

- Credit stress can be a sign of widescale financial problems. In the recent era of low-interest rates, both households and corporate borrowers locked in low borrowing costs, helping to keep debt service payments manageable. However, bonds will mature, and new debts will be incurred at a higher cost. The maturity wall of corporate bonds coming due in years ahead could be a challenge for debt markets. For now, credit spreads have been tame, and loan defaults have been manageable.

- A housing downturn can also foretell a crisis. The rebound in housing activity this year has been a pleasant surprise: borrowers have adjusted to higher interest rates, and national home price indexes have returned to moderate growth after a flat year. Memories of the housing-led Global Financial Crisis have left us all nervous about stress in residential markets, but thus far, they have proven resilient.

The threats of a soft landing come from both directions. Recession risks are on one side, but we cannot rule out the “no landing” scenario: a reacceleration of economic activity. This carries the risk of reigniting the inflationary surge of 2021. Supply chains remain vulnerable to disruption, while labor demand exceeds the supply of workers.

This set of conditions would likely lead to a recurrence of the 1970s when a wage-price spiral developed. Workers would negotiate for higher pay, enabling more spending, pushing up prices, and thus requiring higher wages. Most nations have avoided this dangerous outcome thus far, but another inflationary push could prove to be beyond containment.

In this sense, “no landing” may mean no recession initially, but it would create more kindling for a worse downturn in the future. This may also set the economy on track for stagflation, an interval of high inflation and stagnant demand, a state that can be hard to break.

Everything about the pandemic and its economic outcomes has given us reason to be humble about our forecasts. Tail risks can derail the global economy, but so can layoffs, leverage, liquidity and long lags. Some leading indicators point to recession, but their predictive power is not perfect. The soft landing is not yet upon us, but we certainly hope that we can answer questions about it affirmatively at some point.

Information is not intended to be and should not be construed as an offer, solicitation, or recommendation with respect to any transaction and should not be treated as legal advice, investment advice, or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulations. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: VettaFi’s Fixed Income Symposium was the biggest virtual event of the summer. Register here for the replay link to learn from the experts and thought leaders who participated in the event.

© Northern Trust

Read more commentaries by Northern Trust