Economic indicators are released every week to help provide insight into the overall health of the U.S. economy. In this article, we examine indicators from the past week, such as inflation, that shed light on both inflationary trends and sentiment within the market. Policymakers and advisors closely monitor economic indicators to understand recession risk and the direction of interest rates, as the data can ultimately impact business decisions and financial markets. In the week ending on July 13th, the SPDR S&P 500 ETF Trust (SPY) rose 2.25% while the Invesco S&P 500® Equal Weight ETF (RSP) was up 3.25%.

During their last meeting, the Fed voted to leave interest rates unchanged, however, indicated they were planning on two more rate hikes for 2023. With the next meeting slated for the end of July, uncertainty remains high for what’s ahead for the second half of 2023. This is why the timing of the VettaFi Fixed Income Symposium, on July 24, is ideal. For three hours, VettaFi will be moderating a discussion of ETF industry experts on a range of topics. In addition to CE credit, advisors will hopefully be better equipped to navigate the challenging bond market and understand their income alternatives.

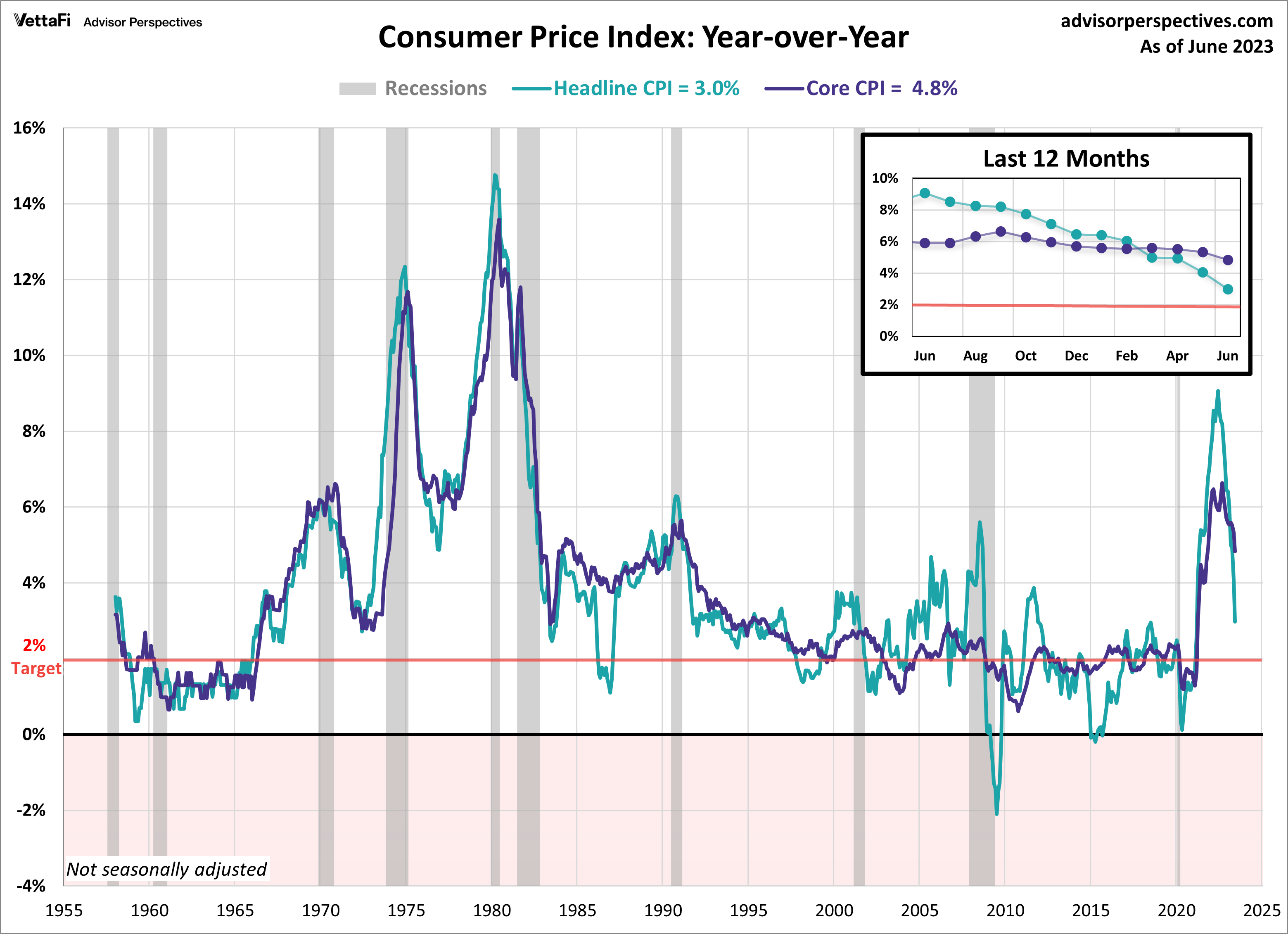

Consumer Price Index (CPI)

The tight grip of inflation is gradually weakening, as the latest CPI data reveals a significant drop to one-third of its peak reached in June 2022. The consumer price index (CPI) rose 3.0% year-over-year and 0.2% month-over-month. The latest reading came in slightly lower than the anticipated 3.1% forecast and is down from May’s 4.0% increase. It marks the twelfth consecutive month of inflation easing and the lowest level observed in almost two and half years. While core inflation also shows signs of easing, its pace is considerably slower compared to the headline number. Core CPI (excluding food and energy) rose 0.2% from May and increased 4.8% year-over-year, down from last month’s 5.3% increase. The latest reading is the lowest level for core CPI since October 2021. Although June’s data is cooler than expected and inflation continues to trend downward, both headline and core CPI levels remain above the Fed’s 2% target rate. Consequently, it is highly likely that the Fed’s next meeting will conclude with another rate hike.

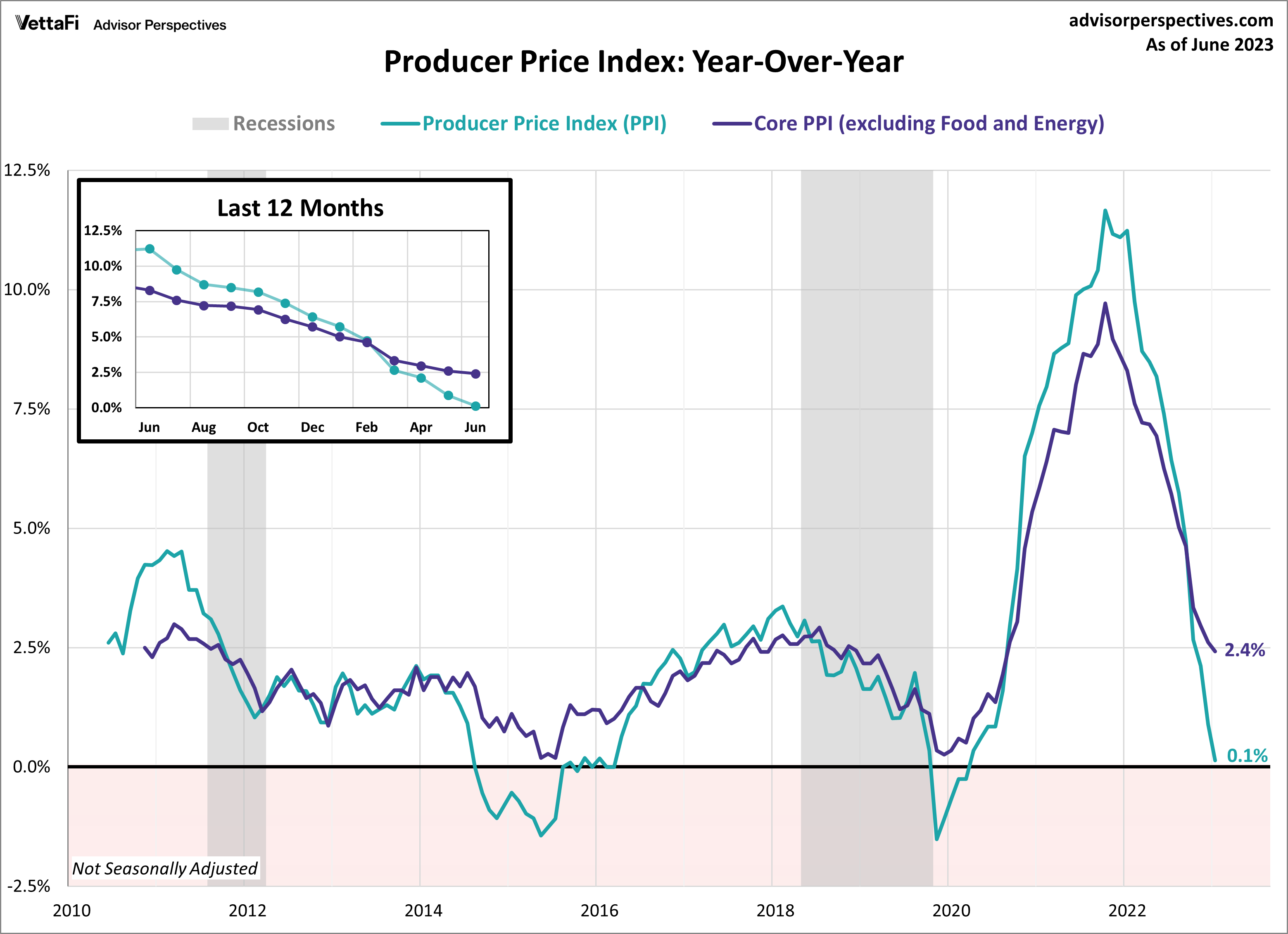

Producer Price Index (PPI)

The producer price index (PPI) for June provided additional evidence of easing inflationary pressures. Wholesale prices rose 0.1% compared to the previous year, down from last month’s 0.9% increase and below the projected 0.4% rise. This marked the 12th consecutive month of slowing for headline PPI and represents the lowest level since August 2020. On a monthly basis, the headline PPI showed a 0.1% increase in wholesale prices, falling short of the expected 0.2% monthly rise. Core PPI (excluding food and energy) also came in lower than expected, showing a 2.4% annual increase, down from last month’s 2.6% increase. This marked the 15th consecutive month of slowing for core PPI, reaching its lowest level since January 2021. Additionally, core wholesale prices saw a 0.1% increase from May.

The producer price index is thought to be a leading indicator of consumer inflation since producers pass along their price shifts to the consumer level. The PPI reached its peak in March 2022 and a few months later in June, the CPI reached its peak. Since then, both indexes have been cooling. The latest PPI numbers show that wholesale inflation continues to cool, offering further hope that consumer inflation will continue to follow suit.