June update

- Municipal bonds posted positive absolute and relative performance in June.

- Modest primary and secondary supply was outpaced by improved demand.

- While July has historically been a top-performing month, we maintain some near-term caution.

Market Overview

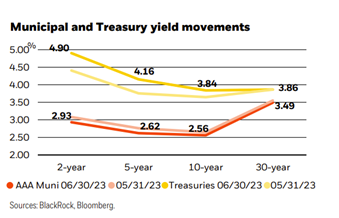

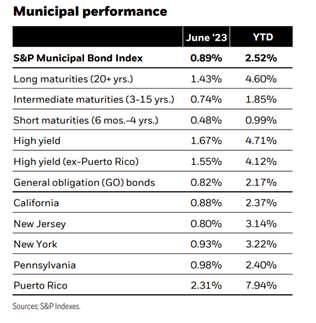

Municipal bonds delivered on expectations for the summer strength and posted positive absolute and relative performance in June. Despite a mid-month pause by the Federal Reserve at the June FOMC meeting, interest rates rose in the front and intermediate part of the yield curve as strong economic data, persistent inflation, and hawkish Fed guidance prompted the market to reprice for a longer tightening cycle. However, improved supply-and-demand technical helped municipals to significantly outperform comparable Treasuries. The S&P Municipal Bond Index returned 0.89%, bringing the year-to-date total return to 2.52%. Longer duration (i.e., more sensitive to interest rate changes) and lower-rated bonds performed best.

The issuance was muted at $36 billion, 8% below the five-year average, bringing the year-to-date total to $171 billion, down 14% year-over-year. As anticipated, the market seasonally transitioned back to net negative supply and benefited from reinvestment income from maturities, calls, and coupons, outpacing issuance by over $2 billion. Deals were oversubscribed by 4.0 times on average, slightly above the year-to-date average of 3.9 times. Similarly, secondary trading was manageable. The bid-wanted activity was slightly elevated at $1.3 billion per day on average but waned modestly as bank portfolio liquidations wrapped up late in the month. At the same time, demand firmed, and the market produced net positive fund flows for the first time since February.

Favorable seasonal technical should aid near-term performance. Historically, July has been a top-performing month, averaging total returns of 1.14% over the past five years. However, some caution is likely still warranted given rich valuations and continued interest rate volatility.

Strategy insights

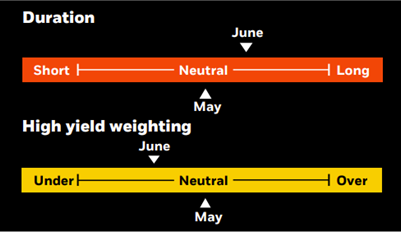

We maintain a neutral-duration posture overall. We prefer an up-in-quality bias with a neutral allocation to noninvestment grade bonds. We strongly advocate a barbell yield curve strategy, pairing front-end exposure with an increased allocation to the 20-year part of the curve.

Overweight

- Essential-service revenue bonds.

- Select the highest quality state and local issuers with the broadest tax support.

- Flagship universities.

- Select issuers in the high-yield space.

Underweight

- Speculative projects with weak sponsorship, unproven technology, or unsound feasibility studies.

- Senior living and long-term care facilities in saturated markets.

- Lower-rated private universities.

- Stand-alone and rural health providers.

Credit headlines

According to a Bloomberg report using data from the Urban Institute, 17 states have experienced revenue declines in their fiscal years through April. States relying heavily on capital gains and income taxes from relatively few, very high earners have been hit especially hard, with California and New York seeing the largest revenue drops. In addition, population shifts, particularly from California and New York, have benefited southern states, such as Florida and Texas, which rely more heavily on sales rather than income taxes and continue to see solid revenue gains. According to the report, roughly 12 states have seen revenue grow by at least 5% over this period. Tax cuts in many states have also contributed to slowing or declining revenue, but record-high reserves are available to offset revenue softness. The National Association of State Budget Officers pegs total state rainy day fund balances at over $160 billion in 2022. While California currently projects a $32 billion deficit this fiscal year, its legislative budget committee recently reported a $38 billion reserve.

In late June, Villanova University entered into an agreement to buy Cabrini University’s campus. After several years of declining enrollment and deficits, Cabrini located a couple of miles from Villanova, announced that it is planning to cease operations in June 2024. Cabrini is rated BBB- by S&P and has $49 million of outstanding municipal bonds. Small liberal arts institutions, especially schools in the saturated northeast and midwestern markets are struggling to attract the shrinking supply of college-quality students and have turned to tuition discounting as a core strategy to maintain enrollment. Large schools with healthy balance sheets that are known for their academic excellence benefit from national demand and are better situated to compete for students. We anticipate similar headlines to follow and risk premiums to drift higher for smaller schools, especially for campuses that are not located near a potential buyer.

Investment involves risk. The two main risks related to fixed-income investing are interest rate risk and credit risk. Typically, when interest rates rise, there is a corresponding decline in the market value of bonds. Credit risk refers to the possibility that the issuer of the bond will not be able to make principal and interest payments. There may be less information available on the financial condition of issuers of municipal securities than for public corporations. The market for municipal bonds may be less liquid than for taxable bonds. A portion of the income from tax-exempt bonds may be taxable. Some investors may be subject to Alternative Minimum Tax (AMT). Capital gains distributions, if any, are taxable. Index performance is shown for illustrative purposes only. You cannot invest directly in an index. Past performance is no guarantee of future results.

This material is not intended to be relied upon as a forecast, research, or investment advice, and is not a recommendation, offer, or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of July 10, 2023, and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive, and are not guaranteed accuracy. There is no guarantee that any forecasts made will come to pass. Any investments named within this material may not necessarily be held in any accounts managed by BlackRock. Reliance upon information in this material is at the sole discretion of the reader.

©2023 BlackRock, Inc or its affiliates. All Rights Reserved. BlackRock is a trademark of BlackRock, Inc or its affiliates. All other trademarks are those of their respective owners.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© BlackRock

Read more commentaries by BlackRock