An upturn in residential activity may be the next inflation challenge.

Last year, tremors in the residential real estate sector added to fears of an imminent recession. During the pandemic, working and schooling from home accelerated decisions to purchase property. Demand for houses surged faster than supply could respond. But spiking prices and rising interest rates caused the market to cool rapidly.

Housing’s decline was one of the few examples of monetary policy working as intended: the higher cost of financing impaired affordability and slowed purchase activity. Though the market was due to cool down, a rapid reversion carried the risk of pain and spillover across the broader economy.

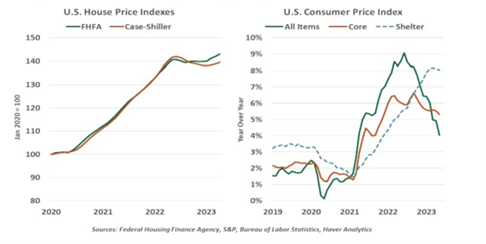

Recent measures out of the housing market show an adaptation to higher borrowing costs. Housing starts bounced by a startling 21.7% from April to May, while new home sales grew 12.2% in the same month. House price indexes (HPIs) through April are showing the beginnings of growth after a year of no appreciation. Mortgage interest rates are rangebound at around 7%, and buyers are not deterred.

Inventories of homes remain constrained. The Census Bureau’s estimated homeowner vacancy rate is holding at a record low of 0.8%. The supply of vacant homes for sale has fallen to levels last seen in 1979 when the nation was 100 million people smaller. A sluggish building cycle over the past decade kept supplies low. Today’s homeowners holding low mortgage rates are unable or unwilling to incur the higher financing cost of upgrading their homes.

The housing market may not be at equilibrium, but it has entered a stasis of tight supply and steady demand. As long as buyers are seeking a constrained number of homes, prices will hold up. By and large, this is good news for the wealth of current homeowners and should assuage those who feared a recurrence of the housing-led stress of the Global Financial Crisis.

However, housing has been the leading contributor to inflation over the past year. The falloff in rents and house prices has been slow to materialize in consumer price indices. And if home values now rebound, it will further complicate the effort to tame prices. While it is nice to see the foundation of a housing recovery, we have to keep inflation in the proper neighborhood.

Information is not intended to be and should not be construed as an offer, solicitation, or recommendation with respect to any transaction and should not be treated as legal advice, investment advice, or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulations. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our podcasts.

© Northern Trust

Read more commentaries by Northern Trust