Continuing last week’s discussion on the role of the minority interest in Japanese equity returns, below we perform the same correlation test on universes of DM Americas and EMEA companies. To recap, we tested the following metrics, drawn from each company’s fiscal year-end reports and stated in USD, and correlated them with the percent price return in local currency over the past five years.

- Accumulated minority interest as a percentage of total capital and of total assets.

- The percentage of shares outstanding is closely held (by insiders, institutions, etc.).

- Minority interest expense is a percentage of the cost of goods sold.

- Equity in affiliate income as a percentage of sales.

The hypotheses for our test were as follows:

H0 (null hypothesis): There is no statistically significant correlation between a given financial metric and a five-year % price return. This would be verified by a correlation’s P-value above 0.05.

H1 (alternate hypothesis): A given financial metric has a statistically significant correlation with price returns. A correlation P-value below 0.05 would identify a given correlation as likely statistically significant and would be the cause for rejecting the null hypothesis for a given metric.

As a little stats refresher, the p-value of a statistical hypothesis test is the likelihood that the null hypothesis is correct. Standard practice is to reject the null hypothesis if the p-value for any metric is below 0.05.

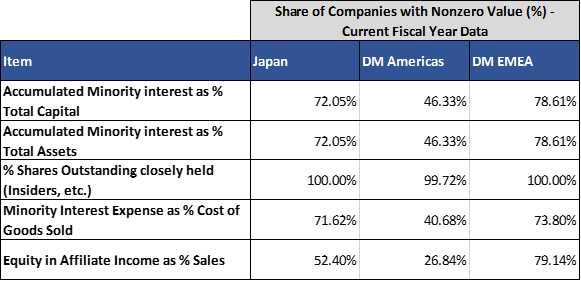

Looking at the results of these tests, we drew the conclusion that Yen-denominated price returns on mid and large-cap Japanese companies over the past five years were statistically unrelated to the metrics we tested. It is important to note that not all the companies tested had non-zero values for the metrics we tested. The following table breaks down the percentage of companies that had values greater than zero for each item, by area.

As you can see, the minority interest phenomenon is relatively prevalent in Japan, significantly more so than in the DM Americas universe we tested. Interestingly, it appears to be even more prominent among the DM EMEA companies tested.

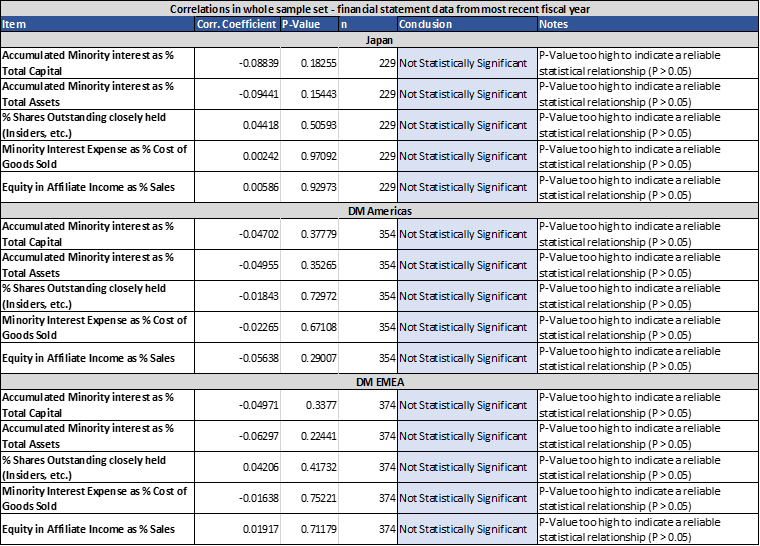

With that said, here are the results from the correlations tested, using financial statement data from the most recent fiscal year-end report for each company. The data used for testing was updated as of 6/16/23.

Once again, there is no statistically significant correlation to be found here. Of all the metrics tested, none appear to provide significant insight into price performance, no matter the region.

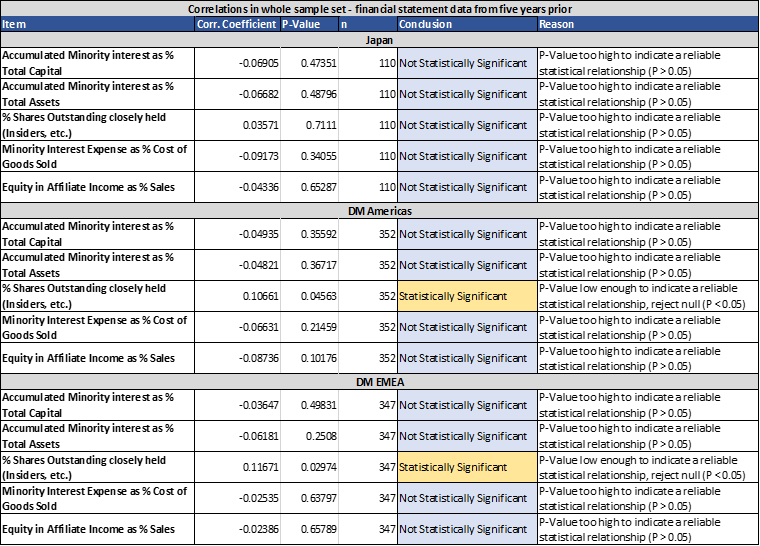

Where this gets especially interesting, however, is when we run the same test on financial statement data from five fiscal years ago.

Our analysis suggests that while insider shareholding has no significant impact on the price performance of Japanese equities, the same does not hold for American and EMEA companies. While the correlation is a relatively weak one, the five-year percent price return of mid- and large-cap DM Americas and DM EMEA stocks does in fact have a statistically significant correlation with insider ownership. So, while all the theorizing about this issue has been focused on Japan lately, what we see here suggests that it is actually DM EMEA and America's companies that are more impacted by this phenomenon.

Disclosures

The information presented here is for informational purposes only and is not to be construed as an offer to sell, or the solicitation of an offer to buy securities. Some investments are not suitable for all investors, and there can be no assurance that any investment strategy will be successful. Hyperlinks may be included in this message that provides direct access to other internet resources, including websites. While we believe these links are to reliable sources, Knowledge Leaders Capital (“KLC”) has no control over the accuracy or content of information contained on these sites. Although we make every effort to ensure such links are accurate, up-to-date, and relevant, we have no control over pages maintained by external providers. The views expressed by these external providers on their own web pages or on external sites they link to are not necessarily those of Knowledge Leaders Capital.

The information provided on this blog is for illustrative or example purposes only and should not be construed as KLC’s opinion or investment outlook. As of the most recent quarter-end, the named companies may have been held by KLC. For full information including additional policies and full disclosures, please visit our website: KnowledgeLeadersCapital.com.

Any reference to Index performance does not represent the performance of any investment product offered by Knowledge Leaders Capital, LLC. An investor cannot invest directly in an index. The performance of the client account may vary from the Index performance. Index returns shown are not reflective of actual investor performance nor do they reflect fees and expenses applicable to investing.

Companies are selected for “Spotlights” based on high levels of innovation activities in their respective industries and illustrate innovation being employed across all sectors and geographies. Spotlight selection is separate from stock selection by the investment team. Spotlights are not necessarily representative of investment opportunities and can be selected regardless of investment performance or inclusion as a KLC holding.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Knowledge Leaders Capital

Read more commentaries by Knowledge Leaders Capital